According to IHS Technology, "By 2017, enterprise spending on the cloud will amount to a projected $235.1 billion, triple the $78.2 billion in 2011."

As the world's largest data center real estate investment trust, REIT, Digital Realty Trust (DLR 0.75%) is in a unique position to cash in on the growth of cloud computing.

However, where there is excitement and growth there is big competition. One such company looking to crowd Digital Realty's turf is DuPont Fabros Technology (NYSE: DFT). Today I'll dig into the two competitors and determine which data center REIT is your better dividend stock.

Diversification

A strong dividend yield is one of the major draws to REITs and Digital Realty's 4.8% yield and DuPont Fabros' 4.4% yield are no exception. Because no dividend is guaranteed, companies that own a diverse portfolio of properties leased to reliable tenants help to ensure investors receive a consistent payout.

Digital Realty owns 131 data centers that make up a combined 25.5 million rentable square feet. For some perspective, that works out to an average size of 200,000 square feet per data center which is about three and a third football fields.

About 78% of rent comes from properties focused in major U.S. cities while remaining properties are primarily located in Europe, and to a lesser extent Asia.

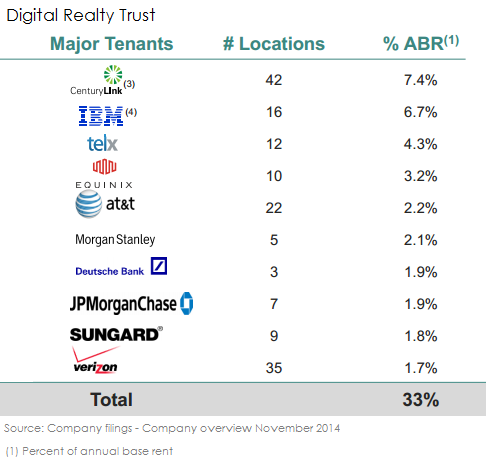

Most importantly, to limit Digital Realty's exposure to any one tenant or industry, the company has more than 600 customers -- none of which make up more 8% of annual rent -- that are diversified throughout several different industries.

DuPont Fabros Technology owns 11 data centers that make up a combined 2.8 million square feet. Despite the company's market cap being almost five times smaller than Digital Realty, DuPont Fabros is the second largest data center REIT.

Of the company's 11 properties eight are located in Northern Virginia. Although the company has 35 different tenants, their four largest customers -- Facebook, Microsoft, Yahoo!, and Rackspace -- account for more than half of their annual rent.

Compared to Digital Realty, nearly every aspect of DuPont Fabros' business is concentrated and this exposes the company to a number of risks, including: regional energy price increases, industry downturns, and the loss of one tenant having a tremendous impact on earnings.

Growth

The other side of diversity is growth, and while there is little doubt Digital Realty and DuPont Fabros will have the opportunity to grow, the question is how fast?

According to Digital Realty, their average data center takes about six months to build -- that's not including the time it takes to acquire the land -- and anywhere from $600 million to just over $1 billion to develop. This makes growing assets not only a fairly slow process but extremely capital intensive.

This is where Digital Realty has another huge advantage. Because of the company's size and stability it has access to $2 billion worth of low-cost funding at the drop of a hat. DuPont Fabros, on the other hand, has $250 million in credit available to them at a higher interest rate.

In fact, over the last five years the two companies' property growth has played out exactly as you might expect. Digital Realty has better access to funding and was able to grow properties by 50 since 2009. While DuPont Fabros has added just five in the same time.

| Company | 3-year annual compound FFO growth 2011-2013 | 3-year annual compound dividend growth 2011-2013 | FFO growth (9/30/13 YTD to 9/30/14 YTD) | Dividend Growth (9/30/13 YTD to 9/30/14 YTD) |

| Digital Realty | 11.8% | 15.6% | 4.6% | 6.4% |

| DuPont Fabros | 13.8% | 29.3% | 29.5% | 50% |

Source: Company filings

Here's the catch: Despite adding more total properties, Digital Realty's larger size makes growing funds from operations, or FFO -- cash generated from real estate operations -- a more difficult proposition. While DuPont Fabros may not have the same access to funding, because of their smaller size the addition of one to two properties per year can go a long way in moving the needle.

Ultimately, the ability to grow their earnings and dividend at a fast clip is the most compelling case to be made for DuPont Fabros.

Leadership

As the driving force behind any company, management is the most important piece to the puzzle. While judging management is often more art than science, there are two broad strokes I find essential.

First, are they good at what they do?

Data centers have the responsible of ensuring customer's information is secure, there is reliable cooling and power, and they are being cost-effective. For companies that are able to juggle these tasks we could assume attracting new tenants as well as re-leasing existing tenants would be much easier.

Currently, both DuPont Fabros and Digital Realty's occupancy is above 90%; this is not only strong for the industry but suggests their services are valuable to their customers.

Second, what are management's plans for the future?

On November 24, Digital Realty announced that Arthur Stein, the company's former chief financial offer, would take over as CEO. During the company's most recent conference call, Stein explained that Digital Realty will be focusing on selling non-core assets and recycling the capital into more attractive options. He suggested this will slow growth but will strengthen the company long-term.

As a long-term investor, I want a management team that is willing sacrifice quarterly results for long-term gains. While it's still very early in Stein's reign as CEO, that seems to be his focus.

As for DuPont Fabros, their current focus is on finding a new CEO. While having the company's co-founders still involved in operations is comforting, for a company whose major selling point is growth I would need to see a stable figure I believe in leading the company before I would consider buying.

Better dividend stock

Despite the fantastic growth potential for DuPont Fabros, I think the company is too vulnerable at this point to be worth a buy.

Ultimately, Digital Realty's size, diversity, strong operations, and long-term focused management give it an enormous competitive advantage to continue to grow with less risk. For those reasons, I believe Digital Realty is a no-brainer investment for investors interested in cashing in on the growth of data centers.