The barbarians were at the gate. Then they were in the boardroom. Now on the front porch about to leave, they have just two more quick questions for Timken (TKR -0.53%). How long after the spinoff before there is a takeover of the steel business and how much will investors make in the deal?

"Can't Fight This Feeling"

The California State Teachers' Retirement System (CalSTRS) and Relational Investors pushed Timken for more than a year to break up. On September 5, Timken announced the spinoff of its steel business with management saying it will occur within the next 12 months.

"I Can See Clearly Now"

The barbarians realize the big money in specialty steel is to be made in the oil and gas industry. Soon they will be cooing to "New" Timken Steel singing, "Come a little bit closer. You're my kind of company" just as they not so secretly shop the company, which will have a lot of interest.

"Hello, Goodbye"

The day after Timken announced plans for a steel business spinoff, Litchfield Hills Research (LHR) attacked the company in a research note.

LHR wrote that Timken would destroy shareholder value by divesting its steel company in the current economic climate. And, it said, Timken Steel would become the target of a leveraged buyout in no less than 36 months from the point of spinoff. Timken's experiment as a public company would also be bad for employees who will face layoffs and who should look for work elsewhere, the research firm warned.

The problem with Timken Steel, LHR claims, is the business lacks the scale necessary to compete in the capital-intensive steel industry. The result, LHR concluded, is the new steel company's share price will underperform industry peers and institutions will dump it. The cautious sentiment was echoed by Moody's Investment Service, which "revised its outlook for Timken to negative from stable."

If the barbarians believe the doom and gloom, they may well try and engineer a Timken Steel takeover.

"Born to Run"

Timken Steel has supplied the oil and gas industry for more than 60 years. The company makes alloys used in tool joints, drill collars, bits, mud motors and whipstocks. And, as producers have continued to drill deeper (see below chart), these Timken products have evolved to better withstand more extreme depths.

"Simply The Best"

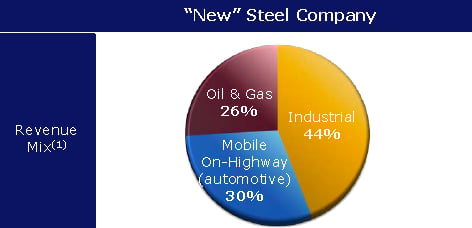

In 2012, Timken Steel generated 24%of its revenue from steel sales to the oil and gas industry. Post spin-off, Timken predicts the independent steel company will expand the proportion of its revenue derived from the oil and gas industry -- by about 2%. (See chart below.) This makes Timken Steel an even more attractive takeover target as drillers start to drill more aggressively and some predict a possible return to 2011 investment levels. (In 2011, producers spent $65.5 billion drilling 10,173 wells in the U.S. alone.)

Timken generates a larger share of its revenue from oil and gas as compared to Carpenter Technology (CRS +2.00%) or Allegheny Technologies' (ATI +2.17%). However, both specialty steel manufacturers are aggressively working to expand their steel sales to the sector. Therefore, it is possible the barbarians will look to these companies in their search for a Timken Steel suitor. Translation: Game on!

Carpenter end markets pre-Latrobe acquisition

"Believe It Or Not"

Hoping to keep the table set for profitable growth, Timken has invested $225 million to expand its Faircrest facility. These improvements will expand production capacity, product range and improve operating efficiency. The upgrades will give Faircrest the ability to produce more exotic steel grades for which there is a strong demand. And efficiency gains achieved through this investment will reduce the facility's workforce 10% while increasing its production capacity.

"Call Me Maybe"

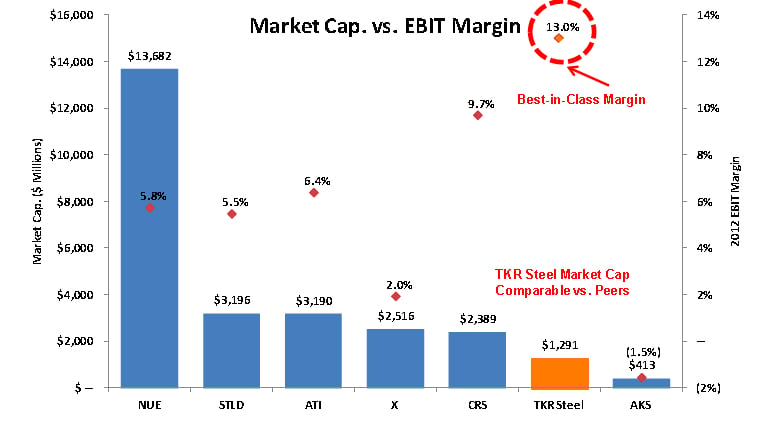

Timken Steel will have minimal debt, a fully funded pension program and the industry's best gross margin (see chart below). Its capacity utilization breakeven point will come in at less than 50% with a long range target of 45%. This is truly remarkable for a business operating in an industry as capital intensive as steel.

And, as mentioned earlier, Timken will generate a large proportion of its revenue from steel sales to the oil and gas industry, an area where significant growth is forecast.

For the barbarians possibly still lingering on the front porch steps at Timken savoring their sweet victory, a takeover of Timken Steel probably needs to be an all cash deal. Either Carpenter or Allegheny would simply come with too much financial baggage for Timken Steel shareholders. Allegheny, for example, has unfunded pension liabilities in excess of $1 billion, along with long-term debt obligations in excess of $2 billion.

Were Timken Steel to receive a non-cash offer for the company from Carpenter, it would also need to think carefully. Carpenter has roughly $400 million in unfunded pension liabilities and more than $600 million in long-term debt.