The tale of pharmaceutical giant Pfizer (PFE 2.24%) is full of contradictions. Like an industry rock star, Pfizer stayed at the top of the charts for years. It rode high on the success of its best-selling cholesterol-lowering treatment, Lipitor.

Lipitor was approved in 1996, and went on to become the best-selling drug of all time and hitting peak sales of $13.7 billion in 2006. When the patent for Lipitor expired in 2011, however, it left a void that could never be filled. Between 2011 and 2012, sales of Lipitor dropped 59% from $9.6 billion to $3.9 billion.

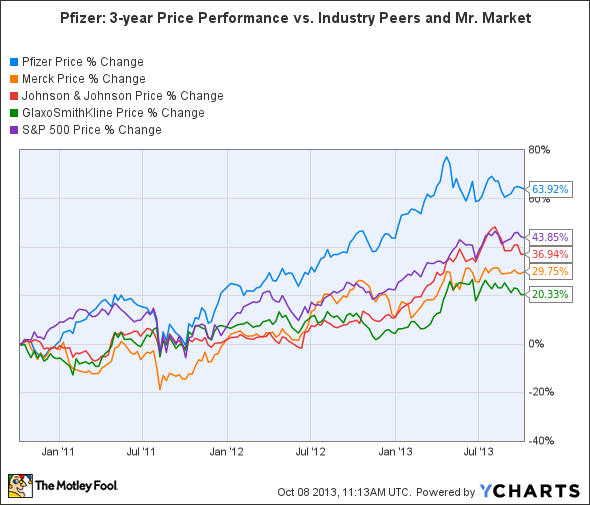

Despite that huge dip in revenue, Pfizer's stock didn't fall off a cliff. In fact, it actually climbed 64% over the past three years, outperforming the overall market as well as industry heavyweights Merck (MRK 2.15%), Johnson & Johnson (JNJ 1.41%), and GlaxoSmithKline (GSK 1.06%).

Source: YCharts.

Could it actually be time to buy Pfizer, despite its patent cliff troubles? Let's take a look at how Pfizer has kept its stock price rising against all odds.

The Foolish fundamentals

We should first take a look at how Pfizer stacks up fundamentally against its industry peers, based on its second quarter earnings report.

|

5-year PEG |

Forward P/E |

Return on Equity |

Qty. Earnings Growth (YOY) |

Qty. Revenue Growth (YOY) | |

|

Pfizer |

4.59 |

12.44 |

14.04% |

333.30% |

(7.10%) |

|

Merck |

4.97 |

13.23 |

9.77% |

(49.50%) |

(10.60%) |

|

J&J |

2.56 |

14.88 |

19.26% |

172.20% |

8.50% |

|

GSK |

3.52 |

12.82 |

55.50% |

(15.60%) |

2.40% |

|

Advantage |

J&J |

Pfizer |

GSK |

Pfizer |

J&J |

Source: Yahoo! Finance as of Oct. 8.

The main thing that stands out is Pfizer's 333% earnings growth. That earnings growth didn't come from product sales, however -- it was mainly attributed to the spin-off of its animal health unit, Zoetis, in May. This isn't a new strategy for Pfizer, as the company sold its infant nutrition business to Nestle for $12 billion in 2012 and its drug capsule business to Kohlberg Kravis Roberts for $2.4 billion in 2011 to preserve its bottom line growth.

Pfizer's revenue declined despite this growth. The decline was due to the loss of exclusivity for Lipitor, sales volatility in emerging markets, and a decline in government bulk orders of its pneumococcal vaccine for young children. Sales of newer cancer treatments fueled a 28% jump in sales of oncology drugs, however.

Pfizer has also been steadily reducing its workforce to cut costs. The company's original long-term layoff target of 10,000 in 2007 was raised to 16,300 in 2011. Those scheduled layoffs have continued throughout 2012 and 2013.

Analysis of revenue growth

This chart of Pfizer's second quarter revenue broken down by business segment shows that sales growth remains elusive for all of its business segments, except for the smaller oncology and consumer health businesses.

|

Business segment |

Q2 revenue |

Year-over-year growth |

Percentage of total sales |

|

Biopharmaceutical Products |

$12.1 billion |

(8%) |

94% |

|

Primary Care |

$3.3 billion |

(17%) | |

|

Specialty Care |

$3.4 billion |

(3%) | |

|

Established Care (generics) |

$2.4 billion |

(11%) | |

|

Emerging Markets |

$2.6 billion |

0% | |

|

Oncology |

$399 million |

24% | |

|

Consumer Healthcare |

$800 million |

4% |

6% |

Sources: Quarterly earnings report, author's calculations.

Starting in fiscal 2014, Pfizer's two business segments will be reorganized into three new divisions. The first business will consist of its immunology and metabolic treatments, along with other products with are patent protected until after 2015. The second business will focus on patented vaccines, oncology treatments, and consumer health care. The third one will manage all of Pfizer's generic medications and branded treatments scheduled to lose patent protection before 2015.

These three businesses will remain under Pfizer's umbrella, though they will report their revenue and earnings separately. Pfizer could eventually use this new setup to split into three companies, or possibly to spin off its money-losing generics business into a new company. However, Pfizer has stated that any decision to sell or spin off businesses would only occur after analyzing three full years worth of financial statements.

Recovering from past losses

Looking back over the past decade, Pfizer's worst loss was obviously Lipitor. However, two other patent expirations -- Protonix and Xalatan -- took their toll on the company's top line as well.

Protonix was an antacid that hit $1.9 billion in peak sales in 2007 before Teva Pharmaceuticals and Sun Pharmaceutical Industries started selling generic versions in 2007 and 2008, respectively. As a result, Protonix sales dropped to $480 million in 2010.

Xalatan was a glaucoma and eye pressure treatment that generated approximately $1.6 billion in annual sales for the company before its patent expired in 2011. Today, companies like Mylan now produce generic versions.

Between 2010 and 2012, the patents on these drugs and several others -- which accounted for 42% of Pfizer's pharmaceutical revenue -- all expired.

Surveying the bumpy road ahead

That bumpy road of patent expirations hasn't ended for Pfizer, however. Pfizer's Celebrex, a $2.7 billion arthritis and menstrual pain medication, could face generic competition by 2015, especially from Novartis subsidiary Sandoz. Meanwhile, sales of the arthritis treatment Enbrel, which it previously co-marketed with Amgen, already faces generic competition across Asia.

There is hope for Pfizer in some of its newly approved treatments, however. These treatments could generate combined peak sales of $10.5 billion, according to the following chart.

|

Treatment |

Application |

Possible peak sales |

|

Xeljanz |

rheumatoid arthritis |

$3.0 billion |

|

Elelyso |

Gaucher disease |

$225 million |

|

Inlyta |

renal cell carcinoma |

$600 million |

|

Xalkori |

non-small-cell lung cancer |

$2.5 billion |

|

Eliquis |

stroke prevention |

$4.2 billion |

| Total |

$10.5 billion |

Sources: Analyst estimates, author's calculations.

While $10.5 billion in additional diversified revenue looks like a good way to eventually fill the void left by Lipitor, there are a few problems investors should be aware of.

Although Xeljanz was approved by the FDA last November, it was rejected by the European Commission due to a lack of sufficient efficacy. The treatment will also face a crowded rheumatoid arthritis market dominated by J&J and Merck's Remicade and Simponi. Xalkori ran into trouble in the U.K. in August, after the British health care guidance body, NICE, recommended against health care reimbursement for the treatment on grounds that it was too expensive.

Meanwhile, though Eliquis showed remarkable efficacy during clinical trials with a 21% reduction in the likelihood of strokes in patients with atrial fibrillation (AF), adoption of the treatment has been slow. This is because Eliquis arrived much later than two other treatments -- Boehringer's Pradaxa in 2010 and Bayer's Xarelto in 2011.

The Foolish takeaway

Although the loss of Lipitor took a huge bite out of Pfizer's top line, the company has maintained balance fairly well by selling off its businesses, reducing its workforce, and gaining approval for new products. In that regard, it's doing much better than Merck, which was hit by the patent expiration of its top selling asthma drug, Singulair, and a series of disappointing pipeline failures.

Although steep challenges still remain, especially in Europe, Pfizer's disciplined method of preserving its bottom line growth should limit the stock's potential downside. Meanwhile, investors will still be paid a forward dividend yield of 3.3% for buying and holding on to shares of Pfizer.