The demand for packaged food items and ready-to-eat products is increasing as a result of quick service restaurants, modern retail trade and also a fast-changing lifestyle. Yet another factor driving growth in this industry is the rise in commodity prices, as a result of which there's more of cooking at home due to a sluggish economy.

B&G Foods (BGS 2.23%) has been on a serial acquisition and merger spree for quite a while, and at the same time it has kept dividend-hungry investors happy through a series of dividend hikes.

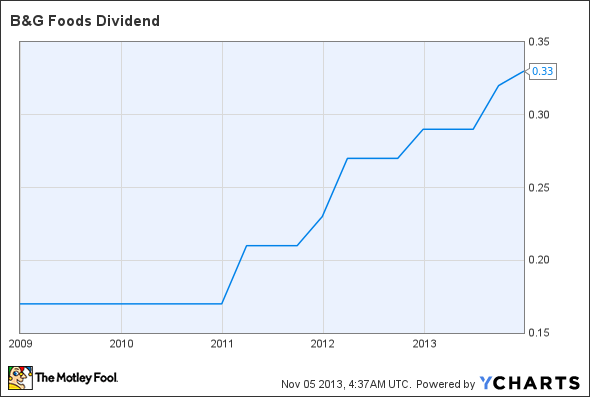

As you can see below, since 2009 B&G Foods has raised its dividend annually by 14%.

BGS Dividend data by YCharts

Hitting a roadblock

Its third-quarter results, however, weren't quite impressive, and this caused a drop in B&G's share price. The primary reason behind weak results was that the core business of the company was declining, and this was getting smartly masked by growth through acquisitions.

Consolidated results looked good as B&G Foods reported an increase in net sales of 17.6% versus the year-ago quarter, bringing net sales to $181.4 million. In the third quarter B&G Foods saw net income slide 9.2% to $15.4 million. This was attributable mainly to acquisition-related costs, as well as debt extinguishment. The company has been growing primarily on the back of acquisitions alone.

For example, Pirate's Brands, which was acquired in July 2013, contributed $16.5 million to the overall increase of $27.2 million in sales. New York Style and Old London brands, which were acquired at the end of October 2012, contributed $11.4 million to the overall increase in revenue. TrueNorth brand, which was acquired in May 2013, contributed $5.4 million to the overall increase.

These accretive acquisitions came to rescue of the company as sales from the core business of B&G Foods decreased by $6.1 million, or 3.9% versus the year-ago quarter, of which $3.5 million was attributable to a net price decrease and $2.6 million was attributable to a volume decline .

A decrease in prices is understandable as the company resorts to promotions and discount coupons. The decline in unit volumes, however, is an ominous sign, and to make matters worse B&G President and CEO David Wenner added that

"Our base business net sales followed industry trends and declined for the quarter. Given current trends in the packaged foods industry, we expect growth in our base business to be challenging during the fourth quarter of 2013."

Acquisitions expected to deliver value

However, continuing its strategy of growth through acquisitions, B&G recently acquired Rickland Orchards from Natural Instincts – a well-known maker of Greek yogurt-coated granola bars and bites -- for $57.5 million. Rickland Orchards has already generated annualized net sales of more than $50 million, and this should lead to continued growth of the brand, as well as incremental sales of existing B&G brands.

Not only does this allow the company to benefit from the current popularity of Greek yogurt, but it's a grab-and-go item that suits today's on-the-go consumer. Food on the run is growing to be a big market, currently valued at $90 billion , according to data from Information Resources. The Rickland Orchards acquisition could allow B&G Foods to step into this burgeoning market.

An industry-wide trend

Much like B&G Foods, TreeHouse Foods (THS +0.83%) has also been focusing on acquisitions, and in July it completed the acquisition of Cains Foods. This acquisition is expected to be accretive to earnings by $0.05 per share in 2014.

In addition, TreeHouse also announced that it would be acquiring Associated Foods, and this is expected to add between $0.14 and $0.16 per share to 2014's earnings, besides adding $200 million to the top line. This would also provide TreeHouse with the private label powdered drinks, specialty teas, and sweeteners that Associated Foods makes. Moreover, it is anticipated that specialty teas will quickly find their way to the K-cup pods. TreeHouse has been an early mover into the K-Cup knock-off market after the patents expired.

TreeHouse has been doing fairly well, and shares have moved up by around 40% year-to-date as compared to around 20% for both B&G Foods and Campbell Soup (CPB 3.05%), another ready-to-eat food company that has been relying on acquisitions like its peers.

Campbell recently acquired Kelsen Group, which produces baked snacks that are sold in 85 countries around the world, with sales of $180 million in fiscal 2012. This acquisition should benefit Campbell Soup's prospects in the Chinese market and increase its global footprint as well.

Campbell is the leading soup brand in the US. The company recently announced that it is going to offer K-cup soup packs that can be instantly prepared through Green Mountain Coffee Roasters' single-serve coffee machine, Keurig, and for this it has already entered into an agreement with Green Mountain.

Bottom line

Acquisitions seem to be driving growth in the food industry, and B&G Foods has been following that path. Recent results might have been a dampener, but a sweet dividend yield of 3.90% should have a calming effect on investors.

The stock itself hasn't done badly this year either. With earnings expected to grow in the double-digits in the next five years, the recent pullback might prove to be an opportunity to get into B&G Foods.