Celgene (CELG +0.00%) recently reported a strong third-quarter revenue and raised its financial guidance for the full year. The company expects total net product sales to exceed $6.2 billion and expects full-year adjusted earnings per share to be in the range of $5.90 to $5.95, from a previous range of $5.80 to $5.90 .

Using Celgene's revenue guidance and product sales estimates for the first nine months of 2013 combined with historical sales trends for each product, I have managed to extrapolate sales estimates of leading products for full year 2013. Based on these estimates, I will venture an objective valuation of the company.

Celgene's current commercial stage products include Revlimid, Vidaza, Abraxane, Pomalyst, Thalomid, and Istodax. Combined they are expected to generate $6.2 billion in 2013. Celgene also receives royalties from Focalin and Ritalin licensed to Novartis and generates some revenue from the sale of services through its Cellular Therapeutics subsidiary. Combined, Celgene could be looking at generating slightly over $6.3 billion in total sales in 2013.

Revlimid (lenalidomide)

Revlimid -- an oral immunomodulatory drug approved to treat patients with multiple myeloma who have received at least one prior therapy -- is expected generate $4.3 billion in 2013, an increase of 14%, compared to 2012.

Revlimid is also approved for patients with mantle cell lymphoma, or MCL, whose disease has relapsed or progressed after two prior therapies and for the treatment of transfusion-dependent anemia due to low- or intermediate-1-risk myelodysplastic syndromes associated with a deletion 5q cytogenetic abnormality.

Celgene continues to evaluate Revlimid in numerous clinical trials for the treatment of a broad range of hematological malignancies. The most important of which is FIRST -- or Frontline Investigation of Revlimid and Dexamethasone versus Standard Thalidomide -- in combination with dexamethasone in newly diagnosed multiple myeloma. Revlimid managed to achieve the primary endpoint of progression-free survival in the pivotal phase 3 trial, and Celgene expects to submit regulatory applications in the U.S. and in Europe for Revlimid use in newly diagnosed multiple myeloma patients during the first quarter of 2014.

Vidaza (azacitidine)

Vidaza, an injectable pyrimidine nucleoside analog for the treatment of patients with myelodysplastic syndromes, is expected to generate sales of $860 million in 2013, a 4% increase compared to 2012. Vidaza lost U.S. regulatory exclusivity in May 2011 but is expected to retain orphan drug exclusivity in Europe through the end of 2018 and in Japan until January 2021.

Abraxane (paclitaxel)

Abraxane, injectable paclitaxel albumin-bound particles, is a chemotherapy treatment option for metastatic breast cancer and non-small-cell lung cancer. Celgene acquired Abraxane, together with Abraxane Bioscience, in October 2010 for $2.9 billion. Abraxane is expected to achieve $630 million in 2013, a 50% increase compared to 2012. In September, the FDA expanded the approved uses of Abraxane to treat patients with late-stage pancreatic cancer.

Pomalyst/Imnovid (pomalidomide)

Pomalyst, a small molecule orally administered immune system modulator, was approved by the FDA in February for patients with multiple myeloma who have received at least two prior therapies, and the product was approved in Europe in August.

Pomalyst is on track to achieving $300 million in 2013, its first year on the market. Such impressive performance points to a potential blockbuster status especially that the product is also being evaluated in a phase 3 clinical trials for the treatment of myelofibrosis and for expanded usage in multiple myeloma. Already analysts are forecasting sales of more than $1 billion by 2017.

Thalomid (thalidomide)

Thalomid, marketed for patients with newly diagnosed multiple myeloma, is expected to achieve net sales of $240 million in 2013, a decline of 21% compared to 2012. Thalomid, an old molecule that is being phased out in favor of Revlimid, is expected to continue a declining trend till it gets completely replaced with newer molecules.

Istodax (romidepsin)

Istodax -- approved for the treatment of cutaneous T-cell lymphoma in patients who have received at least one prior systemic therapy and for the treatment of peripheral T-cell lymphoma in patients who have received at least one prior therapy -- is expected to realize sales of $55 million in 2013, an increase of 10% compared to 2012.

Istodax, which was acquired in January 2010 together with Gloucester Pharmaceuticals for a total of $640 million, has also received orphan drug designation for the treatment of non-Hodgkin's T-cell lymphomas, however, overall it is a niche product and is not expected to reach a blockbuster status.

Apremilast

Apremilast, Celgene's lead product candidate for psoriatic arthritis, psoriasis, and ankylosing spondylitis is currently under active regulatory review and is on track for a possible U.S. launch in 2014. Several analysts estimate global peak revenue north of $1 billion for the product.

Valuation

Celgene is a very successful company with impressive track record and a great potential moving forward. It has purchased approximately 1.5 million of its own shares during the third quarter of 2013 at a total cost of approximately $211 million and, year-to-date, it has repurchased approximately $2 billion worth of its common stock. Celegene also ended the third quarter with $5.9 billion in cash and marketable securities.

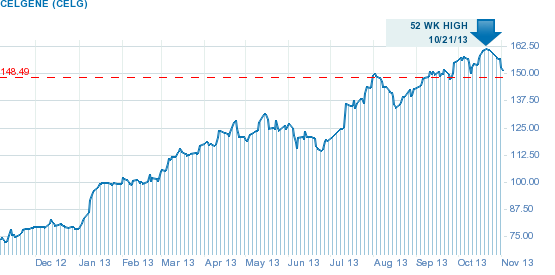

Celgene's share price has almost doubled since the begining of the year, adding an impressive 92% of value, partly due to its exceptional performance and partly due to the share buyback program which reduced the number of total shares. Currently, Celgenes P/E ratio is estimated at 43, and its price-to-sales ratio is estimated at 11.3.

At current share price, and based on Celgene's management full-year guidance, I estimate a P/E of 25 and a price-to-sales ratio of around 10 at the end of the year. If we add the prospects of an Apremilast launch in 2014 coupled with an approval for Revlimide in the newly diagnosed multiple myeloma setting, we could be looking at a healthy company with excellent growth prospects and a reasonable valuation, taken into consideration current valuation levels in the medical biotech space.