Although we don't believe in timing the market or panicking over daily movements, we do like to keep an eye on market changes -- just in case they're material to our investing thesis.

The Dow Jones (^DJI +0.72%) index is trading largely sideways today, up just 28 points at 1:50 p.m. EST. But Verizon Communications (VZ 0.42%) marches to a different drummer. Verizon shares dipped as much as 1.3% over the weekend, making it the second-worst Dow performer today.

So what's wrong with Verizon today, when most of its Dow peers are sailing on smooth market waters?

Well, Verizon just announced that it's buying digital content delivery specialist EdgeCast, leaving investors to wonder if Verizon will get what it paid for -- or less -- from the deal.

Verizon didn't disclose exactly how much it's paying for the privately held media streaming service, but respected industry observer Dan Rayburn estimates the deal at "close to $400 million."

With more than $24 billion of intangible goodwill assets on its balance sheet, Verizon is no stranger to the buyout game. Still, Rayburn's estimate would make this one of Verizon's largest acquisitions in recent years, and the biggest bet so far on the teeming content delivery market.

Content delivery services aren't exactly news to Verizon, but the telecom giant has preferred to resell Akamai Technologies (AKAM +4.48%) services to cover its data customers' CDN needs. Akamai shares plunged 2% on the news that Verizon is taking a direct rival in-house, removing one of Akamai's most important channel partners.

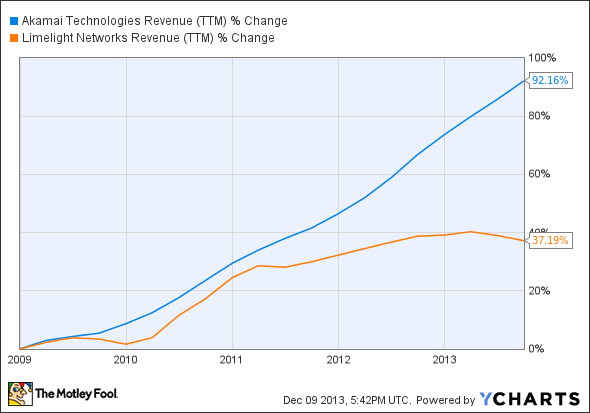

Verizon investors aren't sure that there's any real value in the content delivery market. Akamai has nearly doubled its sales over the last five years, which shows why Verizon might be interested in EdgeCast as a growth driver. On the other hand, smaller content delivery expert Limelight Networks (LLNW +0.00%) has jumped off the revenue growth gravy train. Content delivery is not a guaranteed success, and Verizon might fail to follow Akamai's example.

AKAM Revenue (TTM) data by YCharts.

This deal also flies in the face of recent content delivery trends. In particular, Netflix (NFLX 0.45%) has built its own content delivery system, cutting its ties to both Akamai and Limelight along the way. If the largest content wrangler on the entire Internet can roll its own CDN, then what's stopping other large content distributors from following the same template? On that note, Verizon just might be buying into a dead-end strategy here.

All valid concerns, but I think that the timing of the EdgeCast deal underscores how much value Verizon sees in content delivery. Remember, Verizon is in the middle of a $130 billion agreement to take over the remaining 45% of Verizon Wireless from longtime partner Vodafone. That deal involves a fresh $49 billion bond and doesn't leave Verizon with a lot of financial wiggle room.

But Verizon still sees enough value in content delivery to spend nearly half a billion dollars on EdgeCast, even with the Vodafone deal putting fiscal pressure on Big Red's wallet.

All things considered, EdgeCast won't make or break Verizon's business. I think investors overreacted to the potential risks in the EdgeCast deal. You can take this modest price drop as a gentle buy-in opportunity -- if you were already looking at Verizon as a potential buy.

If not, then nothing much has changed. Take a good, hard look at your Akamai holdings, which may actually suffer from Verizon's new position in the CDN market, and then move on.