In this age of near-zero interest rates income-starved investors have been gravitating toward high yielding companies. While there is nothing inherently wrong with this kind of income investing, several rules must be followed to avoid disaster.

Don't reach for yield

Normally, a high yield can signal trouble with a company, but certain classes of assets, such as MLPs (master limited partnerships), BDCs (business development corporations), and REITs (real estate investment trusts), are different. They pay out a high yield due to the nature of the how the company is structured for tax purposes (BDCs and REITs do not pay taxes as long as they pay 90%-98% of income as dividends).

This doesn't mean that all companies in these sectors are safe. Investors must never buy investments for yield alone. This is called "reaching for yield" and can lead to disaster. Boardwalk Pipeline Partners (BWP +0.00%) gives a perfect example of why.

Boardwalk recently was forced to cut its distribution by 81%. The unit price dropped by nearly 50% as a result, and overnight the yield went from 13% down to 4%. There were three reasons for this severe distribution cut.

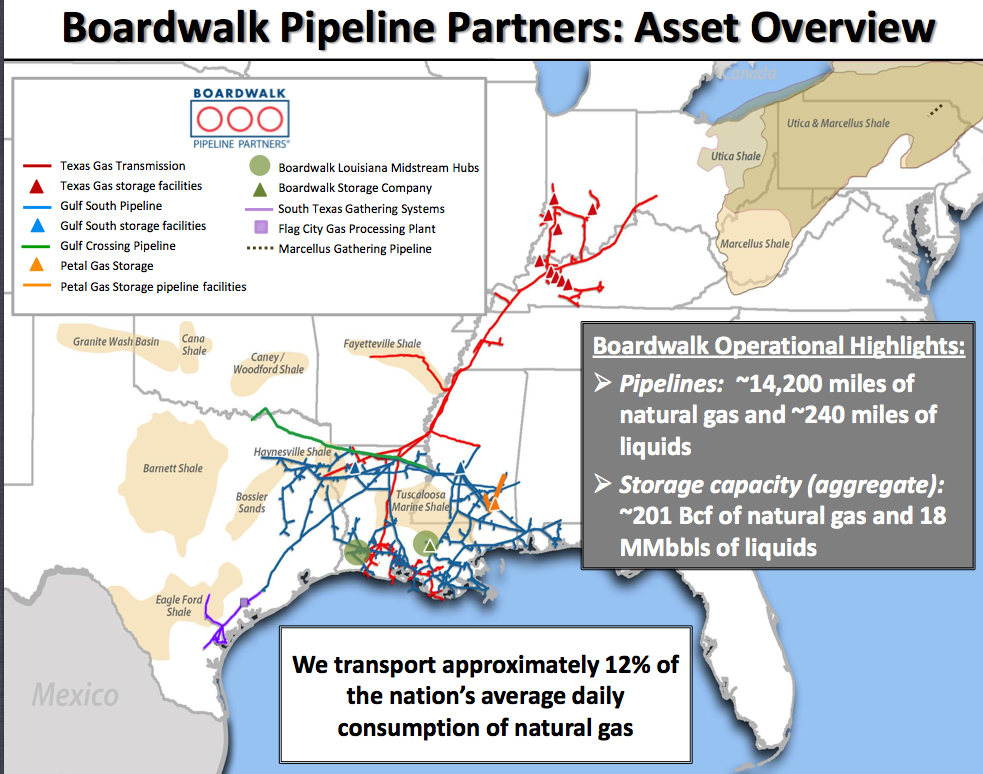

First, Boardwalk was hurt by the location of its assets.

Source: Jefferies Energy Conference presentation

As seen above, Boardwalk's current assets do not serve the most productive shale areas of the nation: the Bakken (ND/MT), Woodford (OK), Barnett (TX), Marcellus, and Utica (OH, WV, PA, NY) shales.

The second reason is the end of long-term, highly profitable contracts beginning in 2013 and extending into 2014 and 2015. These contracts provided fixed-revenue at very generous terms for the partnership's storage and transportation pipelines. However, these contracts were struck prior to the fracking boom and the fall in natural gas prices. When coupled with the poor location of the pipelines, this forced the company to accept lower prices on its new long-term contracts. Unfortunately for Boardwalk, its most profitable contracts will roll-off in 2018 and 2019, meaning that the current decrease in distributable cash flow (DCF) will continue for the long term.

The third reason for the distribution cut is the partnership's high debt level. The debt/EBITDA ratio is currently 5.01. Anything over 4.5 is considered a dangerous debt load and the credit rating Fitch predicted that "the partnership will be shut out of capital markets for a prolonged period of time."

Management is planning a turnaround with an emphasis on debt reduction (debt/EBITDA down to four) and investment in pipelines to serve booming shale areas such as Texas, the Marcellus, and the Utica regions. However, with access to debt markets temporarily cut off and DCF expected to decline from $560 million to $400 million in 2014, management is wisely choosing to retain earnings instead of pay out an unsustainable distribution.

Boardwalk Pipeline Partners is an example of how reaching for yield can blow up in investors' faces. There are far better places to invest one's money.

For example, Magellan Midstream Partners (MMP +0.00%) is perfectly situated to take advantage of America's natural gas bonanza. Its management has a track record of accretive acquisitions ($2.9 billion over the last nine years) as well as organic investment ($1.1 billion under way with $500 million under consideration) that allows for fantastic distribution growth.

Since 2001 Magellan has grown its distribution by 12% CAGR. In 2013, the distribution grew by 16% with management guiding for 20% growth in 2014 and 15% growth in 2015. This kind of distribution growth is possible because Magellan wisely bought out its general partner in 2009 during the height of the financial crisis for just eight times EBITDA. Now 100% of marginal income flows through into the distribution growth. With Magellan trading at a 3.3% yield compared to Boardwalk's 2.8% and boasting far superior distribution growth and fundamentals, investors have no reason to buy Boardwalk over the far superior Magellan.

Avoid "de-worsification"

De-worsification is diversification for its own sake. This means becoming so focused on "checking a sector box" that investors end up buying Boardwalk Partners over Seadrill Limited (SDRL +0.00%).

Seadrill is an undervalued offshore oil driller that has had its price slashed due to negative analyst short-term forecasts of its industry.

This represents an opportunity to buy a well run company that is yielding 11.3% and whose industry is projected to grow at 19% CAGR through 2020 (management is guiding for a 70% growth in EBITDA through 2016). Investors should never overlook a Seadrill just to buy a Boardwalk because of the sector it operates in.

Bottom line

Investors should never reach for yield at the expense of a company's fundamental quality. As Foolish investors we care about quality of the management and its track record for long-term success. In addition, don't fixate on diversification (feeling like you need to own a company in every sector). In the world of high-income investing there is a plethora of quality companies to choose from. A diversified, high yield income portfolio of 15 to 20 companies can be assembled without sacrificing quality, yield, dividend/distribution growth, or security.