It's not easy to find screamingly cheap shares in the industrial sector right now, as most of the big names seem to be pricing in a cyclical recovery. With that said, Ingersoll-Rand (IR +0.58%) looks decently priced should its end markets pick up. The tricky bit is that its rivals in the climate technologies space, such as Lennox International and Johnson Controls Inc. (JCI +2.90%), have both given results recently that confirmed positive underlying conditions, but not to the extent that many had hoped. The good news with Ingersoll-Rand is that its guidance looks a bit conservative, so any upside surprise is likely to be well received, and here is why.

Good, but not good enough

Frankly, expectations of a recovery in the commercial construction sector are getting a bit long in the tooth now, and the market was disappointed with recent earnings reports from Lennox International and Johnson Controls Both companies compete with Ingersoll-Rand in the heating, ventilation and air conditioning, or HVAC, market. For example, in discussing its recent earnings Johnson Controls CEO Alex Molinaroli expressed his frustration: "In the HVAC market, the commercial markets we're still awaiting for a rebound that we haven't seen. And unfortunately it continues to push and in spite of that we have been able to have great bottom-line results, but it's bit frustrating that the market hasn't turned on us yet."

It's not such an issue for Johnson Controls, because the larger part of its profits come from the automotive industry, but Lennox is primarily an HVAC company, and Ingersoll-Rand generated more than 72% of its revenue from its climate division in 2013.

In addition, Molinaroli specifically mentioned frustration with the institutional sector, and this would be a concern for Ingersoll-Rand, because it's a traditional area of strength for the company. Turning to Lennox International, its management expressed confidence that the residential sector would continue do well in 2014, but was less certain over conditions in the commercial sector.

Weather confuses the issue

Bad weather also played a part. On the one hand, extreme bad weather encourages replacement HVAC demand, but it holds back new construction activity. For example, Lennox International saw new commercial construction growth restricted to a low-single-digit amount thanks to extreme bad weather in North America.

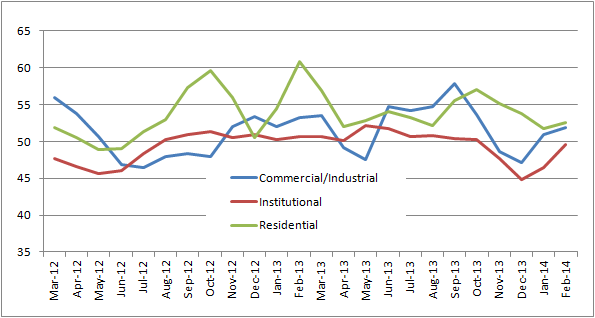

A chart of the commonly followed Architectural Billing Index from the American Institute of Architects illustrates the point:

Source: American Institute of Architects

A reading above 50 indicates growth, and Fools can see that the commercial/industrial index dipped below 50 on two occasions since the end of 2012. Specifically, in the unseasonably poor Spring of 2013, and the bitter winter of 2013 weather had a pronounced effect. However, the underlying indication is that the market is improving. Unfortunately, the improvement showed up too soon in the first-quarter results of these three companies.

Is Ingersoll-Rand being conservative?

There are three reasons why Ingersoll-Rand looks like its guidance could be conservative.

First, its revenue and earnings came in slightly better than expected in the first quarter. EPS came in at $0.29 versus analyst consensus of $0.26. It's not a big quarter for Ingersoll-Rand, so don't get too excited, because it's a small figure compared to its full-year guidance of adjusted EPS of $3.05-$3.20.

On the other hand, the fact that management didn't adjust its full-year guidance upward suggests that they are being prudent. It's overall revenue guidance is for 3%-4% growth in 2014, with the segment split outlined in the table.

| 2013 Operating Income | Forecast Growth for 2014 | |

| Climate | 930 | 4%-5% |

| Industrial | 456 | flat-2% |

| Overall | 1105 | 3%-4% |

Source: Ingersoll Rand presentations

The second point is that total order growth has come in at 2%, 8%, 5%, and 5% for the last four quarters, respectively. The last two numbers are significantly ahead of the 3%-4% revenue guidance for 2014, but again, the next two quarters are the most important for the company.

The third point is that its climate orders were actually up 7% in the first quarter, with the industrial segment seeing a 1% reduction leading to the overall 5% figure quoted above. In other words, the underlying growth in the climate segment is good. Moreover, investors can expect conditions to get better in its industrial segment, because the bad weather caused its golf car sales to be down in the high-single digits in the quarter.

The bottom line

All told, the results from Lennox International, Johnson Controls and Ingersoll-Rand said a similar story about the HVAC market. The residential sector remains strong, but the anticipated pick-up in commercial HVAC hasn't kicked in yet. Nevertheless, should it do so, then Ingersoll-Rand's conservative looking guidance should give it some upside.