Shares of InvenSense (INVN +0.00%), a leading provider of MEMS motion sensors and related semiconductor products, took a nosedive after its most recent earnings report. While the company reiterated its revenue growth outlook of between 25%-35% for the fiscal year ending in March 2015, the company reported mixed results in the most recent quarter (EPS miss by $0.03, revenue beat by $1.58 million). Furthermore, the guide for fiscal Q1 2015 came in at $63 million-$66 million on the top line and $0.07-$0.08 in non-GAAP EPS -- well below a $69.1 million/$0.16 consensus, respectively.

Even with these lackluster numbers and muted near-term outlook, InvenSense is still a pretty compelling long-term story for investors not afraid of a little quarter-to-quarter volatility.

Plenty of room to grow

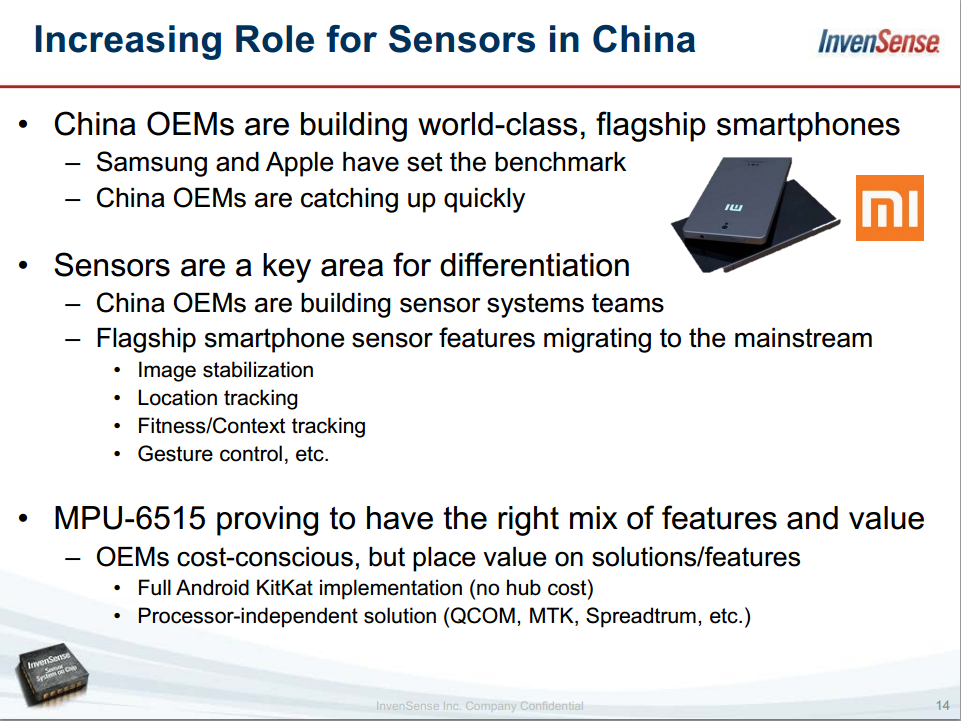

Taking a long-term view, it's important to understand that while the high-end smartphone market is maturing, there is a very long runway for the mass-market smartphones to "grow up" in performance, features, and capabilities. This means that most smartphones, from cheap $149 off-contract devices to premium devices like the Samsung Galaxy S5 that InvenSense is currently in today, will require increasingly sophisticated motion sensing to fully take advantage of next-generation smartphone usage models.

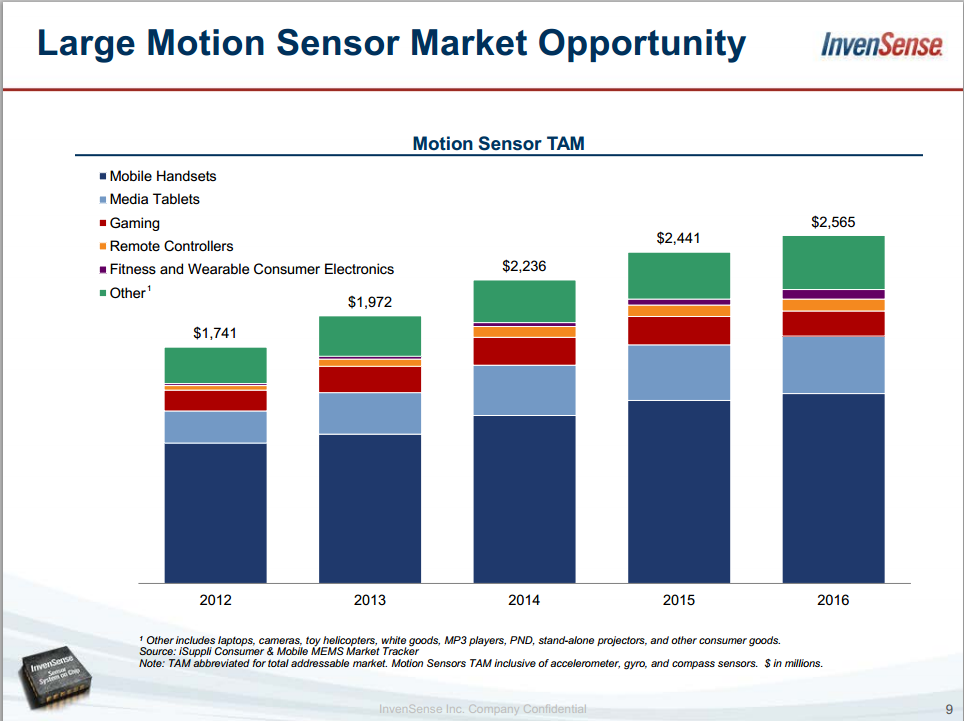

Indeed, as InvenSense notes in the slide above, the features that initially make it into the flagship Samsung (NASDAQOTH: SSNLF) and Apple (AAPL 0.19%) devices eventually find their way into hoards of white-box smartphones from Chinese OEMs. While this may be bad news for Samsung and Apple at the device margin level, this is fantastic news for component supplier InvenSense, which stands to grow its sales dramatically as the number of devices its parts go into grows nicely, as the following chart illustrates nicely:

Source: InvenSense.

InvenSense is investing in the future

In order to take full advantage of the opportunities that lie ahead of it, InvenSense has very nicely upped its research and development spending. The good news here is that this means the company is investing in next-generation technologies that will allow it to maintain a very strong competitive positioning going forward. The bad news (and what hit the stock price short term) is that the dramatically increased R&D spend ahead of the expected sales bump means that the bottom line looks worse than it would otherwise.

R&D spending, for instance, was up from $6.36 million in the March 2013 quarter to a whopping $15.99 million in the March 2014 quarter, representing a 151% increase. Now, year over year, revenues didn't grow anywhere near that much (they jumped from about $55.2 million to $59 million -- a more modest 6.9%) so GAAP net income went from a $13.52 million to a loss of $5.63 million. That's the short-term price a high-growth tech company has to pay in order to secure its long-term future.

The bad news is priced in

After the most recent earnings report, InvenSense was down over 20% in the after-hours session, trading below $17 per share. The stock has recovered from that nicely and is now knocking on $20 a share, but it's still quite a ways off from its 52-week high of $24.34. The good news is that the bad news is priced in. The mixed quarter and the weak guide -- everyone's already expecting bad things! So, the risk here really seems to be to the upside, particularly if InvenSense can finally nab Apple as a customer (either for the iPhone/iPad or for the upcoming iWatch).

This is a stock that's very volatile (as it's a highly shorted, high-growth small-cap tech stock), but the company's future is bright and the bad news seems to be priced in. For investors who can stomach a little volatility, InvenSense could be a great way to not only play the continued growth of the smartphone market but also the upcoming wearable device boom. This is a company investing in the future, and as long as it can execute, shareholders should reap the rewards quite handsomely over the next couple of years.