The federal Bureau of Economic Analysis just released its report on personal income and spending in April. After a brief boost in March, we're back to sustainable long-term growth in April.

The March report showed a 0.5% increase in consumer spending over February levels. In April, the growth pace fell back to 0.3%. To put those short-term figures into perspective, the March growth rate works out to 6.2% annual growth. The lower growth seen in April amounts to 3.7% annually.

Over the past decade, personal income per capita has increased by an average of 3.1% per year. At the current rate, we're still running ahead of long-term growth trends.

But this healthy income growth isn't resulting in equally large spending growth. Personal spending fell 0.1% in April after showing a huge 1% jump in March. Taken together, the average monthly spending growth across these two months works out to roughly 0.4%. It's a return to normalcy after an unusual and unsustainable leap in the previous report.

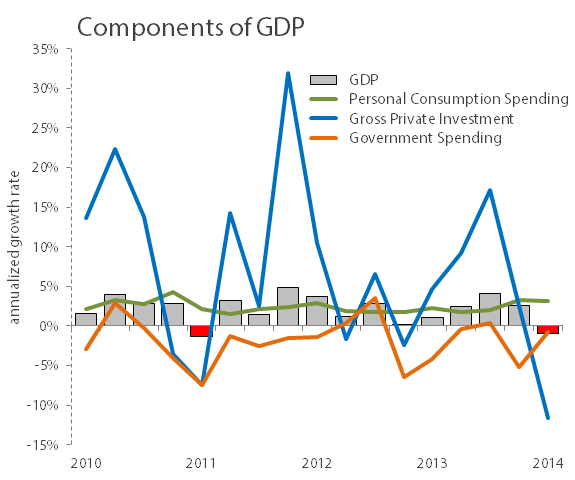

The economy continues to show signs of a healthy recovery on the consumer level. This report is one of many puzzle pieces required to analyze the broader economy, and it needs to be paired with other metrics for a complete picture. Long-term GDP growth and reasonable inflation are among the most important companion data points. Inflation looks good right now, but GDP is having a weak moment.

All things considered, the combination of strong personal-income growth and modest inflation should point to a slow and steady economic recovery. The occasional GDP disappointment works against my theory, but the long-term trend remains positive even there:

Source: U.S. Bureau of Economic Analysis.

Economic recovery is an investable trend, too. As market makers pick up on these strengthening metrics, and as they start to influence sales and earnings across American industries, share prices will follow suit.

Companies with an infrastructure focus often become leading indicators of this relationship. In that light, it makes sense to see United Technologies (UTX -0.10%) and Caterpillar (CAT -1.72%) beating the markets over the last 12 months:

UTX Total Return Price data by YCharts.

United Technologies has beaten earnings estimates in each of its last four quarterly reports thanks to strong organic growth across the board. Importantly, the industrial-machinery is giant is growing faster in America than in Europe.

That's exactly what my economic analysis would predict. A growing American economy should lead to infrastructure improvements in this market, and they can't happen until the builders have enough materials to get the job done.

Caterpillar stumbled in 2013 but is surging in 2014. The construction machinery builder is driven by surging industrial construction orders. Commercial builders sat on their Caterpillar inventories last year but have returned to buying new equipment again. Though we're basically looking at market analysis done by Caterpilar's customers, that's another clear sign of a bounce in the American recovery.

In short, evidence continues to gather for a sustainable recovery trend. The markets are not due for a major correction, at least not according to the tea leaves in my cup.