No one can blame the average dividend investor for salivating when he or she sees a yield north of 5%, or experiencing peace of mind by investing in the largest corporations in the world. We shouldn't forget, however, that there are plenty of great dividend stocks that don't fit either of those molds.

Because of that underappreciated aspect, these "hidden" companies represent outstanding stocks to consider buying now. Today I want to talk to you about one such stock: J.M. Smucker (SJM -0.98%). While you are no doubt familiar with the company's namesake jams and spreads, there's a lot more to the story than you might think.

Source: J.M. Smucker.

Two big slices of the pie

Smucker's business can be understood in two main parts: coffee and everything else -- which includes jams, spreads, peanut butter, and ice cream toppings. Each of these contributes about 40% to the company's total revenue (the remaining 20% comes from its international, foodservice, and natural foods segments).

When it comes to selling basic goods, the power of a brand cannot be underestimated. Well-known and trusted names engender repeat business and allow the company to benefit from tiny markups over lower-priced competition -- which make a huge difference in the long run.

Consider some of the names we're talking about here: Smucker's, Jif peanut butter, Hungry Jack pancake mix, Pillsbury goods, and Crisco oils. While these products don't necessarily represent a huge growth area for the company, they bring in steady amounts of cash that give it freedom to enter new markets and the flexibility to pay an ever-growing dividend.

On the coffee front, the company believes it has a significant opportunity in front of it. While Dunkin' Brands allows J.M. Smucker to manufacture and distribute its coffee in convenience and grocery stores across the country, Smucker isn't able to use Dunkin's coffee where it really counts these days: in K-Cups.

Instead, Smucker owns the Millstone, Folgers, and Folgers Gourmet Selections brands and is attempting to grow its presence in the at-home brewing segment. Though the company sold 1% more coffee last quarter than the previous year, record-low arabica coffee prices kept profits down. Now that those prices are rising -- mostly due to droughts in Brazil -- Smucker believes profits will pick up again.

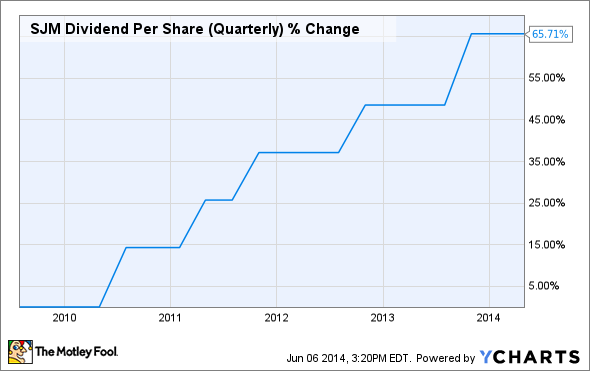

The strength of the dividend

With a solid base of food products and a growing influence in coffee, Smucker has produced steady increases in free cash flow. Between the company's fiscal 2011 and the past 12 months, free cash flow increased a whopping 160% to $553 million.

And yet, it is only using 42% of its free cash flow to pay out its midrange 2.3% dividend yield. A look at the past five years shows a company that has steadily increased its payout.

SJM Dividend Per Share (Quarterly) data by YCharts.

Along with this, Smucker has reduced its share count by 13% over the last three years -- adding even more value for shareholders.

Taken together, this gives you an under-the-radar dividend company with a wide moat, a growing coffee segment, prodigious amounts of free cash flow, and a growing-but-safe dividend. It might not be sexy, but for the long-term, buy-to-hold investor, it's worth looking into.