As we're nearing the halfway point of 2014, I dove behind the scenes to see what Warren Buffett's Berkshire Hathaway (NYSE: BRK-A)(NYSE: BRK-B) has done to cause its stock to rise by 7% on the year and what the next six months may hold.

Why the stock has moved

As you can see in the chart above, Berkshire Hathaway narrowly trails the total return of the S&P 500, which includes dividends -- but remember Buffett is not a fan of paying those -- through the first half of the year.

After the first five or so weeks of the year the broader market tumbled, as fears about the investing landscape persisted thanks to geopolitical turmoil and concerns about the economic recovery in the U.S. arose. And Berkshire Hathaway wasn't immune to the concerns. Yet those fears quickly subsided and things began to rebound throughout February.

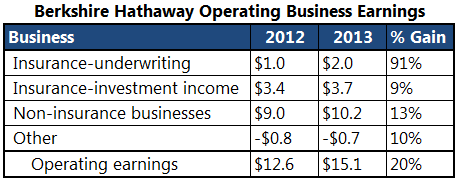

But the big jump in Berkshire Hathaway came after the fourth quarter and resulting full-year financial results were announced on March 1. Berkshire Hathaway saw impressive gains across all of its businesses, as its insurance-underwriting income nearly doubled to $2 billion, its investment income rose by 9%, and the profits from its noninsurance businesses rose by 13% to $10.2 billion.

Combined, these resulted in its operating earnings jumping by 20% year over year:

$billions. Source: Company Investor Relations

This gain of 20% fails to even account for the unrealized gains from its investment portfolio, which grew by a staggering 61% from $38 billion at the end of 2012 to a stunning $61 billion at the end of 2013.

All of this is to say, it's no wonder the stock rebounded when the full-year results were revealed.

The steady movement

Since then, the year has been somewhat quiet for Buffett and Berkshire Hathaway. Thanks to a dip in the underwriting income available from its insurance business -- it was roughly sliced in half -- its earnings through the first three months of the year actually dropped by about 7% to $3.5 billion.

And apart from the announcement of the acquisition of a small subsidiary, which includes a Miami-based TV station, no major moves have been announced or hinted at.

The look ahead

Buffett has suggested he wouldn't buy back the shares of Berkshire Hathaway when they are trading above a 1.2 price-to-book-value multiple, and they currently sit right around a multiple of 1.4. Yet that shouldn't deter investors from considering an investment in Berkshire Hathaway itself, because there is still a lot to like.

All signs point to 2014 continuing to be a year in which Berkshire Hathaway progresses along and performs admirably well, as it continues to position itself to be at the center of the American economy through its railroad, energy, manufacturing, and other core operations -- to say nothing of its insurance businesses.

And knowing Buffett believes "both Berkshire's book value and intrinsic value will outperform the S&P in years when the market is down or moderately up," 2014 could be another great year of outperformance for Berkshire Hathaway.