This article originally appeared as part of ongoing coverage in our premium Motley Fool Rule Breakers service...we hope you enjoy this complimentary peek!

Infrastructure construction and engineering small cap MasTec (MTZ 5.03%) on Monday announced second-quarter earnings that were in line with its reduced guidance and met analyst expectations -- though only after the latter projections were drastically lowered in recent weeks.

Earnings continue to struggle

MasTec reported a quarterly net earnings decline of 12% on a year-over-year basis, from $0.42 per share to $0.37 per share. This was on top of the prior quarter's 28% year-over-year decline. Analysts had expected that $0.37 per share figure; however, the estimate had been lowered by 26% in recent months following revised guidance from the company.

Revenue was up 13% to $1.1 billion thanks to 23% growth in the company's oil and gas segment and 49% growth in power generation. During its first-quarter conference call, management had guided for $1.15 billion to $1.2 billion in sales, but the company in June lowered that figure to $1.1 billion due to expectations of weakness in its wireless and oil and gas segments.

Cause for concern?

MasTec's weakest segment was its electrical transmission unit, which saw revenue fall 3%; but management is more worried about its communications segment, which posted 6% revenue growth. Specific weakness came from the wireless business, where 12% revenue growth was far below expectations and recent historical levels (61.25% compound annual growth over the last five years).

According to MasTec CEO Jose Mas, the problem with the wireless segment has been project deferrals from 2014 to 2015. However, management does foresee "a return to a more normalized level of wireless project revenue in 2015."

Another area of concern was continued weakness in pricing for oil and gas infrastructure, which has traditionally been one of MasTec's strongest performers.

During the quarter, adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) margin compressed to 9.8%, far from management's goal of 12%. However, the company expects margins to strengthen during the second half of the year as demand for oil and gas infrastructure improves.

Management remains bullish on long-term outlook

During the second-quarter conference call, Mas said that despite short-term weakness in certain key markets, "We are very encouraged by the long term outlook in all our businesses and ... we see unprecedented bidding opportunity in multiple markets."

Management offered several examples of its efforts to mitigate the short-term weakness in communications, including this quarter's acquisition of Speed Wire, a broadband and security installation company. Management believes this acquisition will grow its security revenue to $100 million by 2015. MasTec also received a $250 million 1-gigabit fiber contract that will contribute significant revenue growth in 2015 and 2016.

On the oil and gas front, management remains bullish due to this quarter's acquisition of Pacer Construction Holdings, which MasTec believes can greatly increase its presence in Canada's booming oil sands industry.

Canadian oil sands represent one of MasTec's largest growth opportunities. In the last decade, $125 billion in capital expenditure investment has poured into the region as oil sands production has soared from 980,000 barrels per day in 2005 to 2 million barrels per day in 2013. That production is expected to double by 2020, and the Conference Board of Canada anticipates $386 billion in additional natural gas investments by 2035.

What to watch for in the future

MasTec has outlined several short-term and long-term goals.

In the next year or two, investors should keep an eye out for continued weakness in operating margin in the oil and gas segment, as well as a recovery in the growth rates of MasTec's wireless division.

In the medium to long-term, the company has outlined four key areas investors should monitor.

First is continued strong growth in U.S. energy infrastructure, which analyst firm IHS believes is set to experience $890 billion in new investment through 2026. If oil and gas margins improve, the growth rate of this segment could greatly increase.

Second is international expansion, both into Canada, where MasTec expects to generate $700 million this year,and Mexico. The company today has a small presence in the Mexican wireless infrastructure, but it aims to cash in on the expected $10 billion in natural gas pipeline infrastructure that is expected to occur between 2013 and 2018 to support growth of Mexican imports of U.S. natural gas.

Another growth avenue management is targeting is further bolt-on acquisitions. With its recent Pacer acquisition, MasTec expanded its borrowing facility from $750 million to $1 billion and added the capability to borrow in Canadian dollars and Mexican pesos.

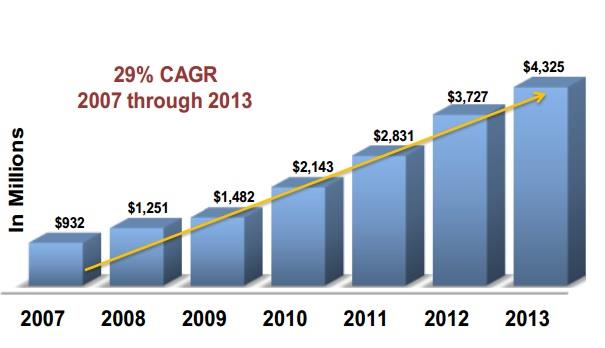

MasTec has acquired $1.2 billion worth of companies since 2007; this has allowed expansion into new markets, which (alongside strong post-acquisition organic growth) has been a major reason for the company's growth success.

Source: MasTec August Corporate Presentation, page 5.

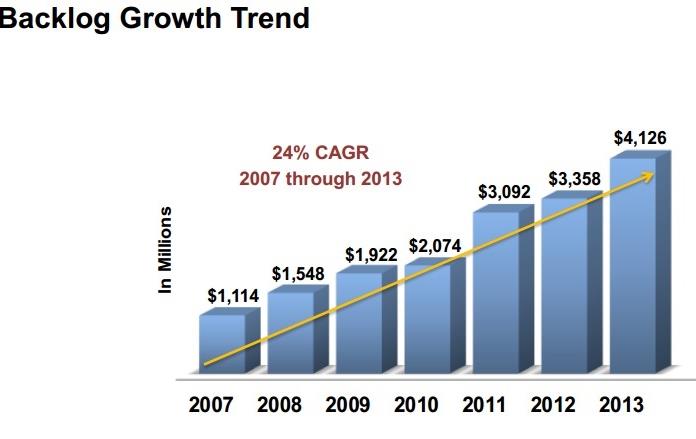

One final area to watch is the company's project backlog. After this quarter's results the backlog is down 5% compared to the second quarter of 2013. While this isn't currently a trend, it's something investors should watch going forward.

Source: MasTec August Corporate Presentation, page 8.

Final takeaway

MasTec has reported two bad quarters, but management is confident the company's long-term growth potential remains intact due to its exposure to megatrends in the energy and telecommunication industries.