Ending a quest that started in 2008, General Electric (GE +1.06%) has found a buyer for its home appliance business. Swedish home goods giant Electrolux has signed on the dotted line, and will pay $3.3 billion for GE's most iconic consumer products division.

Source: Electrolux.

Assuming the deal clears regulatory reviews, the companies expect to close it in the second half of 2015. If not, Electrolux would be on the hook for a $175 million breakup fee.

Electrolux agreed to continue using the GE Appliances brand, via a long-term license agreement with GE. The Swedish company expects to reap some $300 million in annual cost synergies from this deal, as the two businesses bring together their operational logistics.

But manufacturing will continue to depend on GE Appliances' nine established sites, employing about 12,000 Americans. The Electrolux-owned operation will also exploit GE's nationwide distribution and marketing networks, giving Electrolux a much higher profile in North America.

Electrolux investors sent the stock nearly 6% higher on the Stockholm exchange. GE shares rose as much as 0.8% on the news.

For GE, the deal is an important step toward the company's long-term vision.

When CEO Jeff Immelt first said he would like to unload this asset, he was looking for exits from several slow-growth and highly volatile operations. The appliances segment fit both of these bills: "GE Appliances has a very strong brand," Immelt said in 2008. "However, it remains primarily a U.S. business, meaning its fortunes are tied to the rise and fall of a single market."

The deal also helps GE focus on business-to-business operations rather than sales to the fickle consumer. That's in line with the 2011 sale of media unit NBC Universal to cable broadcaster Comcast, and also plays well alongside the sale of credit card and consumer banking operations in markets like Thailand, Switzerland, and the U.S.

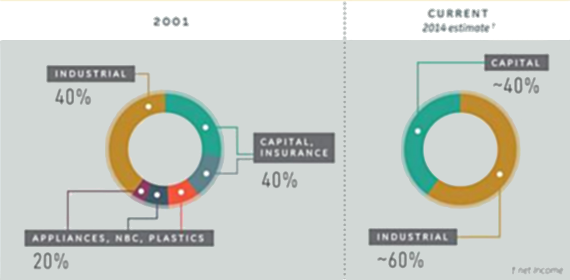

But wait -- there's more. If GE has one overarching goal right now, it would be to rebalance its dependence of the bank-like GE Capital division. The pending $17 billion acquisition of French power grid specialist Alstom hinges on this target. Management is hoping to collect 75% of its earnings from industrial operations and only 25% from financial finagling, up from the current 60/40 split.

Source: General Electric.

At first glance, selling a small but significant unit from the industrial side of the house would seem to work against this long-term target. Immelt would beg to disagree, though.

"This transaction is consistent with our strategy to be the world's best infrastructure and technology company," he said in a prepared statement. The press release went on to explain how GE wants more of its high-margin energy, power, aviation, and healthcare businesses at the expense of less profitable operations.

The appliances and lighting division accounted for 5% of GE's sales in 2013, but only 1% of total operating profits. In other words, the division is far less profitable than the average GE business.

By accelerating the strategy shift into more profitable segments, GE should reach its 75/25 target faster. Keep in mind that it's an earnings goal, not a new revenue balance. That's why it helps to remove a less-profitable unit from the industrial side of the equation.

So everyone leaves the deal-making table happy. Electrolux expands and enhances its North American operations, and General Electric takes steps toward meeting three different long-term goals.