It's easy to overreact when a company like FuelCell Energy (FCEL +0.54%) reports earnings. When the sales figures come out, overambitious investors throw piles of money at it and panicked ones head for the exit. This past quarter was no exception. Since the company released earnings earlier this week, shares have tumbled more than 10%, as sales figures weren't what people were hoping for.

Was the big sell-off warranted? Were investors overreacting? Or were shares of FuelCell overpriced in the first place? Let's look at some of the finer points of FuelCell Energy's quarterly earnings release to see what investors should be both excited and concerned about when looking at the future.

It wasn't that bad ...

The 20% revenue decline seemed to be what caught most people's attention, as it should. However, a company of FuelCell's size -- especially one that's selling an emerging technology like fuel cells -- is expected to encounter a few bumps in the road. According to the company's most recent conference call, several projects that were intended to be booked the past quarter were pushed into this coming quarter. That's a big part of why the company's inventory of finished products more than doubled to $19 million in the quarter.

The company was able to increase its gross margins despite the sales decline, largely thanks to a slight shift in its sales mix. Instead of sales that were dominated by one-off fuel cell kits, the company is starting to move toward sales of complete power plants and multi-megawatt fuel cell parks. This past quarter, sales of fuel cell kits and complete power plants were about equal for the first time ever.

As the company shifts toward more complete power plants and multi-megawatt fuel cell parks, these things may become more common. The longer lead times for manufacturing and construction could lead to higher inventory levels and potentially sporadic sales from quarter to quarter, so investors should worry more about sales on an annualized basis than each quarter individually. Also, increasing product revenue will be critical for FuelCell Energy to reach profitability. Transforming its sales mix will go a long way in accomplishing that goal.

... but it wasn't good, either.

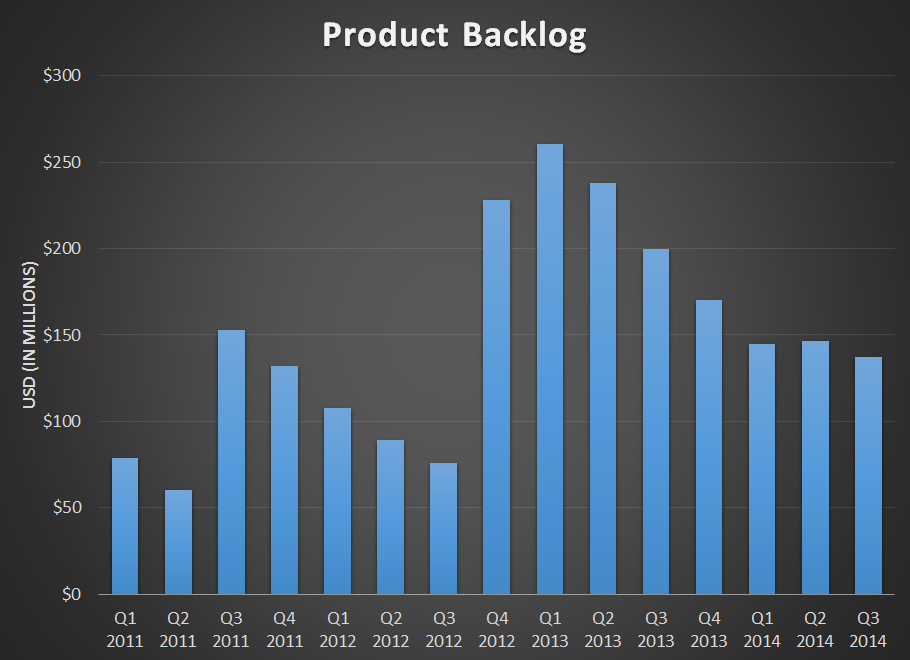

Of course, not everything was rainbows and unicorns this past quarter, either. Two things to watch are declining product backlog and declining margins on service revenue. Yes, total backlog for the company increased on a year-over-year basis to $350 million, which is a pretty healthy-looking number considering that it's only a $650 million company by market capitalization. Looking deeper at these numbers, though, it's hard to not see that the backlog of product sales decreased on both a sequential and year-over-year basis to $137 million, the lowest level in two years.

Source: company quarterly earnings releases.

This total backlog of sales is equivalent to about 83 megawatts of new products, and with the company maintaining a run rate at a factor of about 70 megawatts, the company could go through this entire backlog in a little more than a year. Granted, service backlogs have steadily increased as more and more production comes online, which gives the company a stable, growing revenue base to work from. However, FuelCell Energy can't get by on service of its existing fleet alone, and a declining product backlog should be slightly concerning for investors.

Then there was its service revenue margins. This past quarter, we saw service revenue margins slip from 7.5% this time last year to just over 6% this past quarter. Today, this didn't have a material impact on the company's overall results, since service revenue is a little more than 15% of total revenue, but as FuelCell's backlog suggests, service revenue will become a larger and larger aspect of the business. Even if product revenue margins were in the teens as the company hopes as it reaches annual production of about 80-90 megawatts, low-single-digit service margins will probably drag down profitability in the company and make the path to generating its first positive net income a little further away.

What a Fool believes

This quarter didn't change much when it comes to the overall investment thesis for FuelCell Energy. Yes, there are certainly signs that the company is headed in the right direction, but there are still lots of unanswered questions when it comes to competing technologies in the fuel cell space, as well as FuelCell Energy's ability to generate sustainable profits over the long term. Also, considering that the market currently values FuelCell Energy at a total enterprise value-to-total annual revenue figure of 4.3, you're not exactly getting a steal when buying shares. It may be worth keeping an eye on FuelCell for the time being, but it may not be the best time to buy.