Industrial equipment manufacturer Emerson Electric's (EMR +2.58%) stock price is down more than 8% year to date, and investors must be wondering when the company will join the broader market rally. By management's own admission, sales growth has been lower than hoped for this year. Moreover, there are a number of reasons the company could continue to disappoint investors in the near term. Let's look at three of them.

Emerson Electric needs more spending on energy infrastructure Source: Motley Fool Flickr.

An uncertain geopolitical situation

If there is one thing that has affected the company this year, it's geopolitical concerns. Essentially, sales have grown slower than orders as customers continue to display cautiousness on current spending due to global tensions. Unfortunately, there are no shortages of issues to worry about, including conflicts in the Middle East and Ukraine, the debt default situation in Argentina, and emerging market growth coming in lower than expected. Caution is not an uncommon situation in the industrial equipment sector right now.

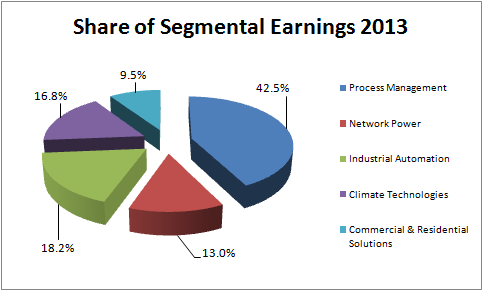

Many of these issues resonate strongly in the emerging world and affect the kind of long-cycle projects (oil and gas processing, chemicals processing, etc.) that Emerson Electric sells into. In particular, its two biggest segments (process management and industrial automation) are being affected negatively.

Source: Emerson Electric Presentations.

For example, in the third quarter the commercial and residential and climate technologies segments recorded respective underlying growth of 4% and 6%. However, process management and industrial automation grew underlying sales by only 2% and 0%. Process management's underlying sales growth in the Middle East and Asia was down 11% and 2%, respectively. In other words, geopolitical events are hurting its most important segments of process management and industrial automation. This certainly could continue.

China set to disappoint?

So far this year, the company's performance in China has been strong. However, given signs of a slowdown in growth in the country, how much longer can that continue?

A quick look at its China sales by segment in the third quarter reveals how well Emerson Electric is doing there.

| Segment | Third Quarter Sales Growth in China |

| Process Management | 7% |

| Industrial Automation | 7% |

| Network Power | 6% |

| Climate Technologies | 16% |

| Commercial & Residential Solutions | 10% |

Source: Emerson Electric Presentations.

Still, construction machinery stalwart Deere (DE +2.04%) recently argued that conditions were slowing in China, and Caterpillar (CAT +5.60%) (a significant customer of Emerson Electric) has also reported a weakening outlook in the country.

Putting this into context, China made up 12.9% of Emerson's sales in 2013. Looking forward, CEO David Farr expects 5%-8% growth in China next year, so things look positive for now. However, this outlook would have to be reduced should China's economy slow further in 2015.

Emerson Electric might miss estimates

The company has missed analyst estimates for the last two quarters, and underlying sales growth is trending at the lower end of management's forecast for 3%-5% for the full year. So investors have reason to worry about the fourth quarter. The company has an opportunity to generate growth by reducing its growing backlog in the quarter, but this is somewhat dependent on the spending plans of its customers. All told, internal guidance is for full-year earnings per share of $3.68-$3.80, but analysts forecast $3.70 -- toward the low end of management's figures.

The takeaway

All told, these three concerns combine a near-term risk (missing earnings) and two medium- to long-term risks (China's economy slowing and geopolitical concerns). Unfortunately, management can do little about global GDP growth or customers' sentiment toward geopolitical risk: Emerson Electric remains at the mercy of global political and economical considerations. Throw in the potential for some disappointing earnings and there is sufficient cause for concern with the stock.