Offshore Oil Drillers such as Transocean (RIG -3.19%), Seadrill (SDRL +0.00%), Ensco (ESV +0.00%), Noble (NE +0.00%), and Diamond Offshore (DO +0.00%) have faced a difficult year, with oil companies pushing back new drilling projects into 2015 and 2016.

In Transocean's most recent conference call, CEO Steve Newman, Executive Vice President and Chief Financial Officer Esa Ikaheimonen, and Senior VP of Marketing Terry Bonno made several statements regarding the state of the company, as well as the industry, that investors in these companies should be aware of.

Market conditions aren't improving

"Since our last call, the ultra-deepwater market outlook is largely unchanged. ... [We're facing] very challenging market conditions. ... While we see a few opportunities on the horizon in the Golden Triangle, India, and Mexico, continuing delays in customer programs and a growing sublet market continue to put pressure on utilization." --Terry Bonno

This is a major concern for Transocean, which is facing a massive number of contract expirations in the years to come.

Source: Transocean Investor Presentation, Pareto Offshore Energy Conference

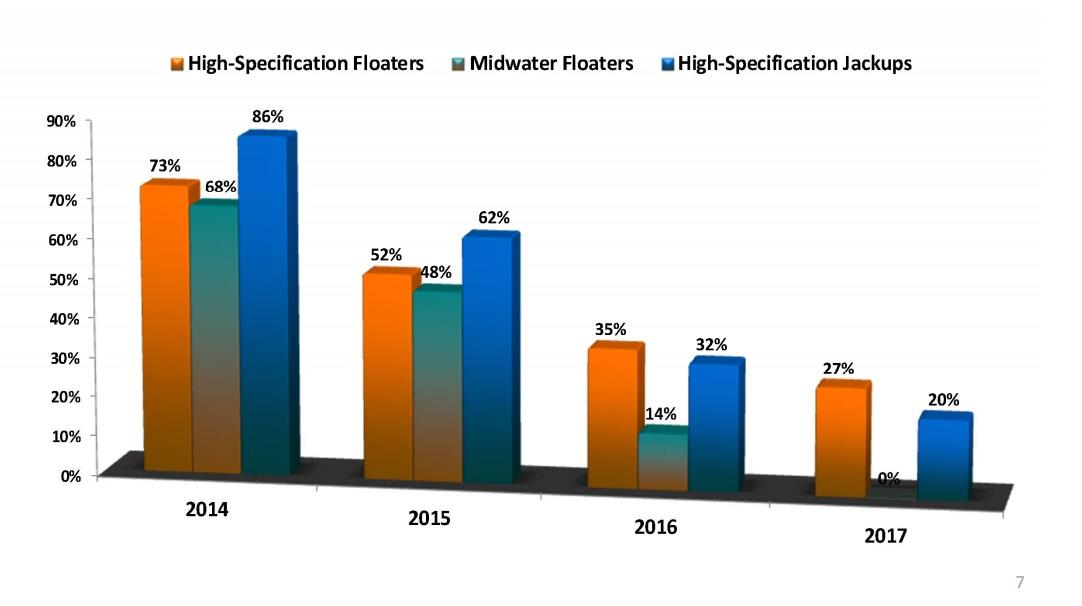

As the above image illustrates, through 2016 Transocean has a vast majority of its ultra-deepwater (UDW) drillships coming off contract, which is a far larger percentage of its fleet than its competitors:

- 81% of Transocean's drillships coming off contract by the end of 2016

- 74% of Diamond Offshore's drillships will be off contract

- 63% of Noble's drillships

- 62% for Ensco

- 38% for Seadrill

"The large influx of uncontracted newbuilds will challenge the less capable units and we are likely to see pricing pressure in the future from the increasing competition." --Terry Bonno

Source: Transocean Investor Presentation, Pareto Offshore Drilling Conference

"Year-to-date we generated $1.4 billion of contract backlog, including securing contracts for the KG1, Jack Bates, and the Celtic Sea." --Terry Bonno

Source: Transocean Investor Presentation, Pareto Offshore Drilling Conference

"The Deepwater Invictus, the most recent addition to our industry leading fleet of high-spec rigs has commenced its three year contract with BHP Billiton in the Gulf of Mexico at a dayrate of $595,000 a day. The Deepwater Asgard is expected to commence its three year contract at $600,000 per day any day now. As a reminder, five of the remaining seven ultra-deepwater newbuilds under construction are backed by attractive long-term contracts with key customers." --Steve Newman

Source: Transocean Investor Presentation, Pareto Offshore Drilling Conference

"We completed a very successful initial public offering of Transocean Partners (NYSE: RIGP) contributing net proceeds of approximately $420 million to Transocean." --Esa Ikaheimonen