This is turning out to be a very disappointing year for investors in SandRidge Energy (NYSE: SD). As the following chart shows, 2014 actually started off great as SandRidge Energy handily beat the market until this summer.

And then everything went downhill at incredible speed. The stock is down just over 24% year to date after being up well over 20% on the year just a few months ago. Let's look at what went wrong and if there is any chance that SandRidge Energy can reverse its slump.

It all started so well

SandRidge Energy got off to a strong start to 2014 as the company blew past analysts' estimates for the first quarter by delivering strong results in the three key areas that matter most to investors. Unfortunately, the company could not repeat those strong results in the second quarter, which has sent the stock spiraling lower.

SandRidge actually beat analysts' earnings estimates in the second quarter. The problem was production, which was affected by power and weather-related disruptions in the Mid-Continent, while the company also ran into water saturation issues while drilling wells for its SandRidge Permian Trust (PER +0.00%). This caused the company to curtail 250,000 barrels of production on the quarter while also lowering its full-year output guidance by 4%.

But wait, there's more

The poor operational performance in the second quarter wasn't the only bad news to come from SandRidge Energy this summer. Just a few weeks after announcing its disappointing quarterly results, the company said COO David Lawler would leave to become chief executive of BP's (BP 0.42%) newly separated U.S. Lower 48 onshore business.

That was disappointing news for investors, as Lawler had been in charge of leading the company's operations after the previous COO was ousted as part of an activist-led shake-up. He implemented several innovative development techniques that helped SandRidge Energy become a much more efficient operator.

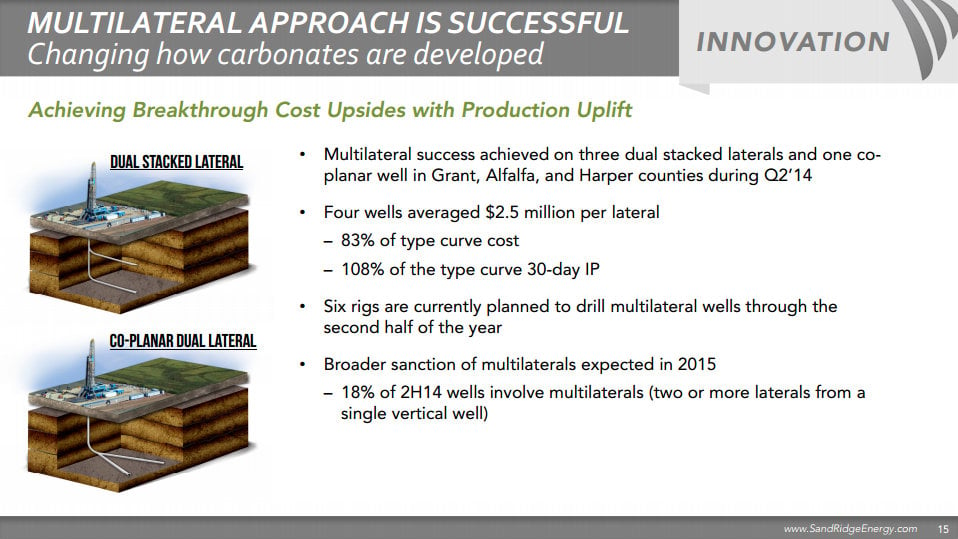

One of the innovations SandRidge has started to roll out is using dual-stacked laterals to drill more wells at a lower cost. The following slide details this technique.

Source: SandRidge Energy Investor Presentation.

SandRidge Energy was able to drill four wells for $2.5 million in the second quarter, which was 17% lower than a typical well costs. Even better, the production was 8% higher than that of a typical well.

Investors hate to see a member of the C-Suite leave. In SandRidge's case, the concern is that Lawler's replacement won't deliver the same level of innovation in the future, and so returns will suffer. The company is searching for a new COO; but until that replacement is found and delivers results, investors will be doubtful whether SandRidge Energy can achieve its goals.

And then there's oil

The final issue plaguing SandRidge Energy's shares this year is the plunging price of oil. The Mid-Continent isn't the best-returning oil play in America, and those returns are further squeezed when oil prices fall.

WTI Crude Oil Spot Price data by YCharts.

At its current well costs, SandRidge Energy's internal rate of return dropped from 65% with oil close to $100 to less than 50% as oil prices fell toward $90 per barrel. In this situation it's no surprise to see SandRidge Energy's stock drop as well, as it fuels the bulk of the company's returns and most of its cash flow.

Investor takeaway

It's remarkable how quickly SandRidge Energy lost momentum. One bad quarter, one executive leaving, and falling oil prices were all investors needed to head toward the exits. That being said, SandRidge can reverse its fortunes by delivering better third-quarter results and quickly finding a new COO, and if oil prices rise again.