Genworth Financial (GNW 1.60%) has had a rough couple of months. New regulations in the mortgage insurance market could prove to be costly and some of the company's older long-term care policies are hemorrhaging money.

However, the company is optimistic about the future of both of its major revenue streams: long-term care and mortgage insurance. And the valuation is extremely attractive. Maybe now is the time to buy Genworth, before things start firing on all cylinders and the fire-sale valuation goes away.

Mortgage insurance: turning a bad situation into a competitive advantage

In July, the Federal Housing Finance Agency (FHFA) issued a new set of requirements for companies that provide private mortgage insurance on loans owned by Fannie Mae and Freddie Mac.

Basically, the new requirements include stronger capital levels, a clearly established performance-monitoring system, and strong quality control requirements. The goal is for mortgage insurers to meet risk-based standards that reflect the quality and performance of the underlying mortgages.

While this will ultimately cost the company more money, Genworth is attempting to turn it into a positive catalyst. Essentially, Genworth plans to be fully compliant with the new regulations by the end of June 2015, a full year ahead of the requirement. CEO Tom McInerney said during the latest conference call that this will create a competitive advantage for Genworth in the MI business, especially with its banking customers.

Long-term care is still the future

Around the same time the housing crisis hit in the U.S., the long-term care business took a turn for the worse. Some companies, like MetLife, dropped the LTC business entirely. Genworth, on the other hand, made it through the tough times and now is the top provider of long-term care insurance in the United States.

However, Genworth's long-term care business isn't exactly raking in the profits right now. In fact, the July quarterly report showed just $6 million in operating profit from the LTC book, as compared with $46 million in the previous quarter. And the company reported that the higher claim losses might require a reevaluation of the company's reserves, which could ultimately result in a reserve charge.

Still, Genworth's management is optimistic on the future of the company's LTC business. Genworth is currently seeking approval by the states to increase rates on some of its older, money-losing LTC products. As of the most recent quarter, 43 states had improved some rate increases, and Genworth plans to continue to push for the remaining increases it needs.

According to management, this alone could result in $100 million in additional premium income, which would roughly translate to an extra $0.20 in earnings per share all by itself.

And, it's hard to make the case that there isn't money to be made from LTC in the future. According to the company, there are 78 million people in the U.S. between the ages of 50 and 68, and 70% of them will need some level of long-term care in their lifetimes. However, less than 10% of them currently have any LTC insurance. So, there is a huge opportunity here, and Genworth's leading market share gives it a head start in capitalizing on it.

Genworth is how cheap?

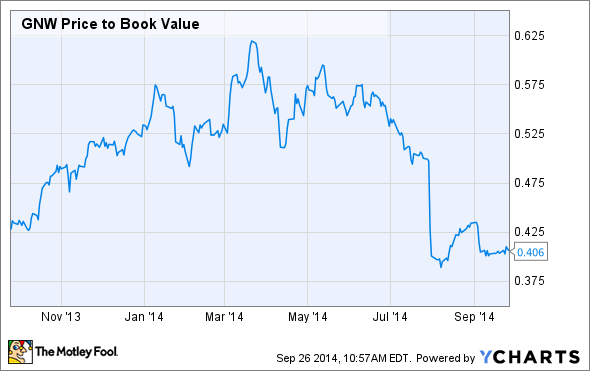

Perhaps the most compelling reason to consider Genworth for your portfolio is the valuation. Thanks to the pessimism in the market related to the company's current LTC business and the uncertainty surrounding a potential reserve charge, Genworth trades for just over 40% of its book value.

Genworth has traded for a substantial discount to book since the housing crisis began, but lately it has plummeted to its lowest valuation in more than a year.

Risks and rewards

Now, any company trading for such a steep discount doesn't come without substantial risk.

One big question mark is the potential for a reserve charge that I mentioned earlier. Some experts have estimated that it could be as high as $1 billion, but analysts think $200 million is a more likely figure. Still, uncertainty is uncertainty.

And, there is the question of whether or not the company will be able to execute on its plans, both in the MI and LTC businesses. While this will be no easy task, it can definitely be done.

However, if over the coming years, Genworth is successful and can trade closer to its book value, like it did before the financial crisis hit, it would mean a share price of more than $32, or about 140% more than the current level.

In my opinion, the potential reward here greatly outweighs the risk, and now may be the time to take a chance on Genworth. And, analysts tend to agree. In fact, the average one-year target price on the stock is more than 33% above the current price.