Shares of Costco Wholesale (COST +1.50%) have gained a little more than 10% in the last year even though the company's earnings fell short of analyst estimates for 4 consecutive quarters.

Costco 1 Year Stock Chart, data by YCharts

On Wednesday morning, Costco reported earnings for Q4 of its 2014 fiscal year, and investors were finally rewarded for their patience. For the first time in more than a year, Costco produced robust earnings growth and comfortably beat analysts' earnings estimates.

Earnings growth accelerates

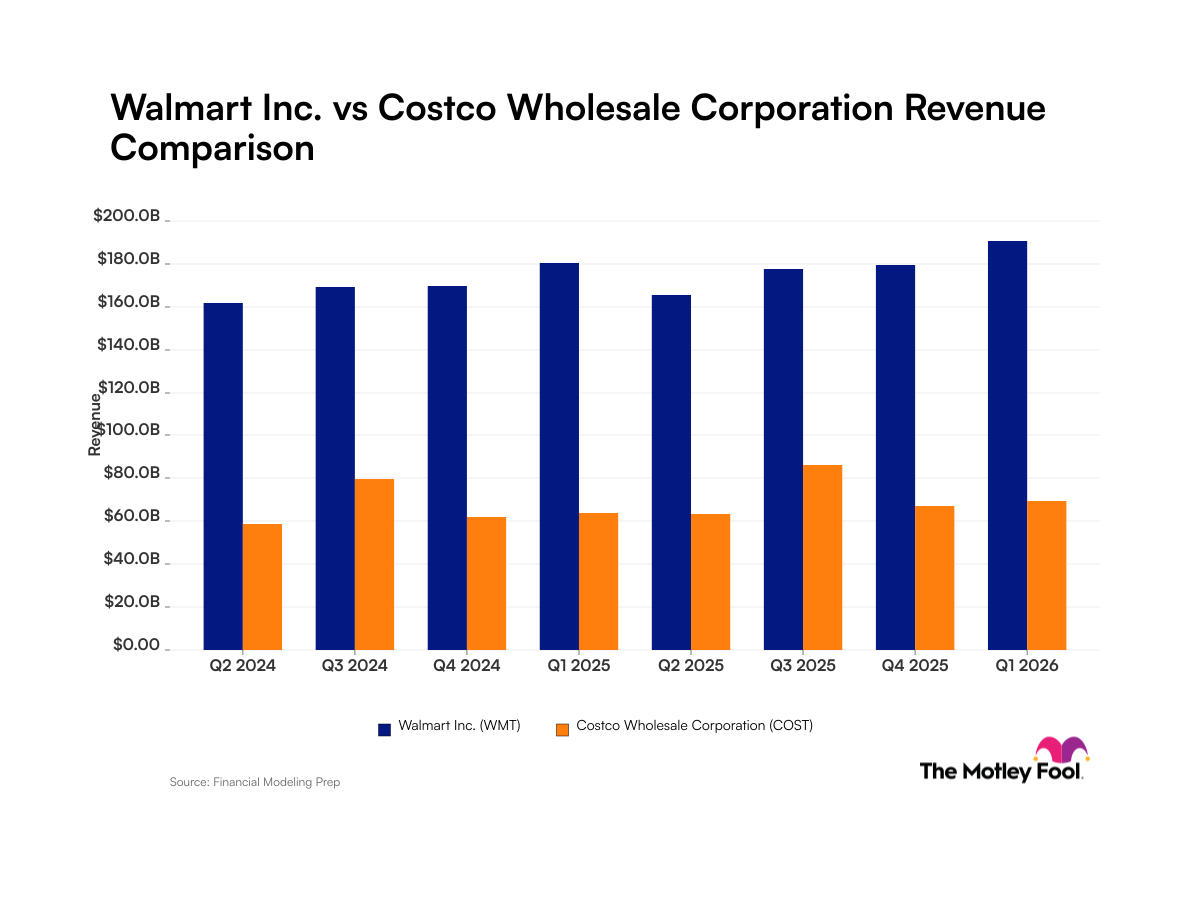

Last month, Costco announced that Q4 sales rose 9% to $34.8 billion. Including $768 million in membership fees, Costco's revenue totaled just more than $35.5 billion, in line with the average analyst estimate.

Costco's gross margin (excluding membership fee income) widened slightly from 10.55% to 10.70%, while operating expenses declined from 9.75% of sales to 9.73% of sales. The slight increase in gross margin and even smaller decline in Costco's operating expense rate led to a somewhat higher profit margin.

Costco grew net income 13% year-over-year to $697 million. EPS also rose 13% year-over-year, reaching $1.58. On average, analysts had been expecting EPS of $1.52, and $1.58 was in line with the highest of 26 Wall Street analysts' estimates.

Costco members are extremely loyal (Photo: The Motley Fool)

This return to double-digit earnings growth is very comforting for shareholders, because earnings had stalled out earlier this year due to slower sales growth and margin contraction. In fact, through the first three quarters of FY14, Costco's earnings were down slightly year-over-year.

Costco's solid Q4 performance confirms the strength of its business model. Whereas other big-box retailers have been struggling to produce sales growth, Costco has consistently grown sales at a high single-digit rate. Its industry-leading prices drive a steady influx of new members and high renewal rates (around 90% in the U.S. and Canada) among existing members.

Looking forward

Costco released its September sales report along with its quarterly earnings report, providing a peek at early trends in FY15. Comparable sales rose 4% last month, or 6% excluding the negative impact of gas price deflation and currency fluctuations.

Those sales results are in line with Costco's results for FY14, but worse than what Costco has been posting for the past few months. Investors shouldn't worry too much about a single month of data, but it's worth paying attention to the next few sales reports just to make sure that Costco's growth trajectory remains intact.

In addition to growing comparable sales within its existing warehouses, Costco also has a large opportunity to grow by adding new warehouses. Recently, it has been growing its footprint by about 4% annually -- opening 25-30 new warehouses each year.

Costco is growing its warehouse count by about 4% annually (Photo: The Motley Fool)

Today, the vast majority of Costco warehouses are in North America. However, Costco has been successful in various other countries -- from Japan to Taiwan to the U.K. -- suggesting that the appeal of discount warehouses travels well. In May, Costco opened a warehouse in Spain: its first in continental Europe.

Costco plans to open another warehouse in Spain within the next year. Expansion throughout the rest of Europe and Asia and into Latin America provides a long growth map for Costco.

A strong performance

Costco returned to double digit earnings growth last quarter, suggesting that the margin issues that were holding down earnings for much of the past year are finally receding. That bodes well for Costco's FY15 performance.

Costco shares rose about 2% in pre-market trading on Wednesday, and could set a new all-time high during the day. Considering that Costco stabilized its profit margin last quarter while still growing sales rapidly, these gains seem well-deserved.