Most investors would agree that rates are probably much closer to a bottom than a top. And many investors are rightfully looking for ways to profit should rates inevitably rise.

Business development companies such as TCP Capital (TCPC -0.57%) have emerged as a high-yield way to profit on rate hikes. The thesis for this BDC is relatively simple: since 77% of its debt investments are floating rate, rising rates should naturally boost its profitability.

The thesis is logical, but there are some complexities to consider before buying TCP Capital.

Just how high rates need to go

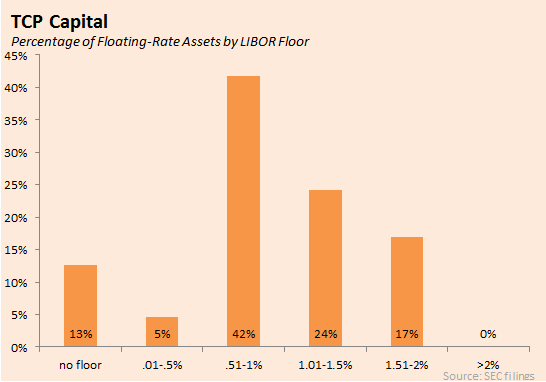

TCP Capital's financial statements reveal important information about its loan portfolio. Beside each loan are the basic terms -- is it floating or fixed, what rate is used, and does the loan have an interest rate floor?

When thinking about how interest rates might affect TCP Capital's profitability, the floors are critically important. An interest rate floor is a minimum rate charged on a floating-rate loan. Thus, for rising rates to result in higher yields on a loan, the current interest rate must exceed the floor rate.

I went through every floating-rate loan on TCP Capital's books and put them in a pile based on their floor rate. The result looks like this:

We can use this chart to get a bird's eye view of TCP Capital's sensitivity to higher rates. Roughly 13% of its floating-rate loans by fair value do not have a floor. Thus, any increase in LIBOR will result in a higher yield on these loans.

However, roughly 87% of its loans have a floor rate. And many of them need LIBOR to rise above 1% for the yield to increase from its current level.

The other side

In recent months, TCP Capital has improved its financial position by securing an SBIC license and issuing new fixed-rate debt.

However, the bulk of its borrowing will come from floating-rate credit facilities, which do not have a floor rate. Thus, a modest increase in rates would result in more interest expenses than interest income, negatively affecting its bottom line. Only after substantial increases would TCP Capital begin to benefit.

Its own disclosures point out that a 1 percentage point increase would cost the company about $1 million in annual income. A two percentage point increase, though, would generate $2.5 million in additional annual income.

Before blindly buying TCP Capital, or any BDC, on the basis of its exposure to floating-rate loans, consider carefully how much rates would have to rise before you see a benefit. In almost every case, BDCs would lose money if rates rise only by one to two percentage points.