Xerox (XRX +0.00%) has struggled to transform itself into something other than "that copier company" for years, but transformation has been a long time coming. The company's third-quarter earnings, released this morning, won't offer much to either bulls or bears, as Xerox's slow shift toward services did not meaningfully accelerate in the third quarter. Its overall results were essentially in line with expectations, which is probably why its shares are essentially flat today.

For the third quarter, Xerox reported $5.12 billion in revenue, with adjusted earnings of $0.27 per share. Wall Street's analysts had expected Xerox to earn $0.26 per share on $5.19 billion in revenue, so the company narrowly beat on the top line while narrowly missing on the top line.

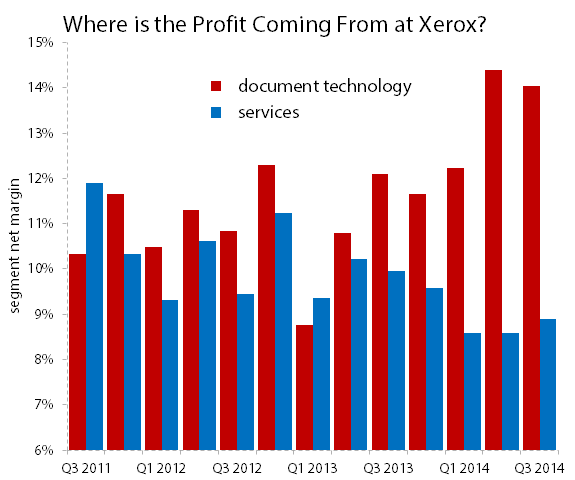

Xerox's cost-cutting efforts seem to have somewhat stalled, however, as margins in its Services segment fell year over year from an even 10% to 8.9%, while the segment's top line barely budged from its results a year ago. Margins in Xerox's Document Technology -- think hardware -- segment rose from 12.1% a year ago to 14% for the latest quarter; but that segment's top line also shrank by 6% year over year, resulting in lower actual earnings.

Looking ahead, Xerox now expects between $0.30 and $0.32 in EPS for the fourth quarter, which will add up to full-year earnings in the range of $1.11 to $1.13 per share. Wall Street has been expecting $0.31 in EPS for the fourth quarter, and $1.11 for the full year, so Xerox's guidance simply confirms existing expectations.

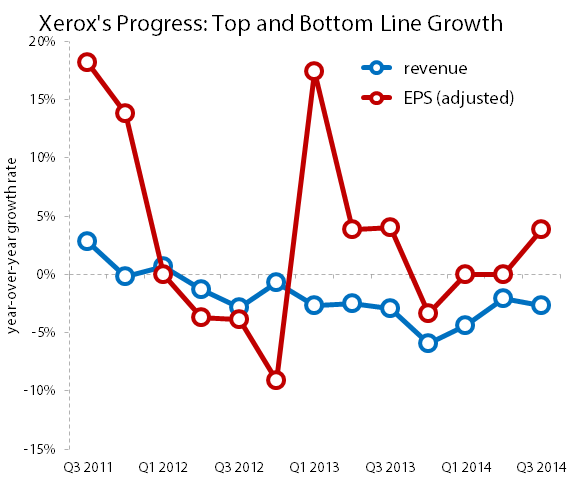

Let's take a closer look at Xerox's progress now, starting with top- and bottom-line growth, which you'll notice have continued a recent trend:

Source: Xerox earnings reports.

Xerox finally returned to growth on the bottom line, but its top line has been falling for nearly three years, without respite. The last time Xerox's revenue actually improved year over year was during the first quarter of 2012, and that was only the narrowest possible improvement. Xerox's bottom-line growth has been somewhat more erratic, but it remains lower on a nominal basis than it was two years ago. Third-quarter results for 2012 saw adjusted EPS of $0.25, but net income was actually $16 million higher at that point than it was during the third quarter of 2014, because Xerox has reduced its share count by roughly 6% during the past two years.

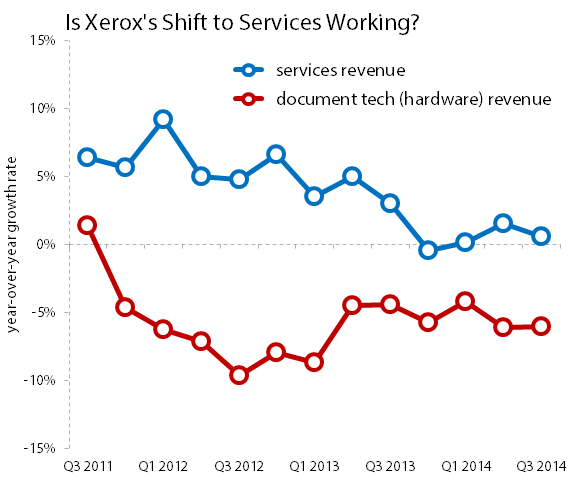

To understand why this is happening, we must look more closely at Xerox's two core segments: Services and Document Technology. Document Technology is Xerox's legacy hardware business, focused on copiers and printers, while services is broadly focused on helping companies and government agencies manage their data. Services is the segment on which Xerox has pinned its future; but its recent progress has not been particularly encouraging:

Source: Xerox earnings reports.

Services has seen its top-line growth stall out in recent quarters, which is bad news considering Xerox has been actively reducing its dependence on its Document Technology segment for some time. This might not be such an issue if Services were actually producing plus-sized profits; but margins in this segment have dwindled as Document Technology has become a better moneymaker than ever:

Source: Xerox earnings reports.

Weak Services earnings continues to be a source of some consternation among longtime Xerox followers, who expect service-based revenues to produce greater profits, because many service-focused companies have historically mustered strong double-digit profit margins. With Services comprising almost 58% of total company revenue in the third quarter -- its highest share ever -- the segment needs to prove that it can be more profitable than it's historically been to justify investor optimism for Xerox's shares. This isn't likely to happen in the fourth quarter, but investors should continue to watch Xerox's services segment closely for signs of stronger progress.

This quarter offered no surprises, and the market reacted accordingly. Xerox's transformation continues, but the end result remains uncertain.