Western Digital (WDC -3.81%) reported earnings for the first quarter of its 2015 fiscal year this afternoon. The hard-disk-drive leader generated $3.94 billion in revenue for the quarter ended in September, resulting in adjusted earnings of $2.10 per share, and both results topped Wall Street's expectations. Analysts had modeled $3.89 billion in revenue and $2.03 in adjusted EPS.

Despite the double beat, Western Digital's shares have slipped a bit in after-hours trading and currently cling to a loss of roughly 2% as of this writing. The reason lies in the company's forward guidance. Western Digital now expects to generate between $3.75 billion and $3.85 billion in revenue for its fiscal second quarter, which will result in adjusted earnings of $2.00 to $2.10 per share. These estimates both undershoot Wall Street's consensus numbers even on the high end, as analysts were expecting $3.9 billion in revenue and $2.20 in adjusted EPS for the second quarter.

In all, this wasn't a particularly compelling quarter for Western Digital, which saw its revenue rise by less than 4% year over year while its adjusted EPS declined 1% year over year. The company also lost market share in the HDD market, as its 44% share of an estimated 147.2 million HDDs shipped during the quarter was down from 45.7% in the prior quarter, and also lower than the year-ago quarter's 44.7% share.

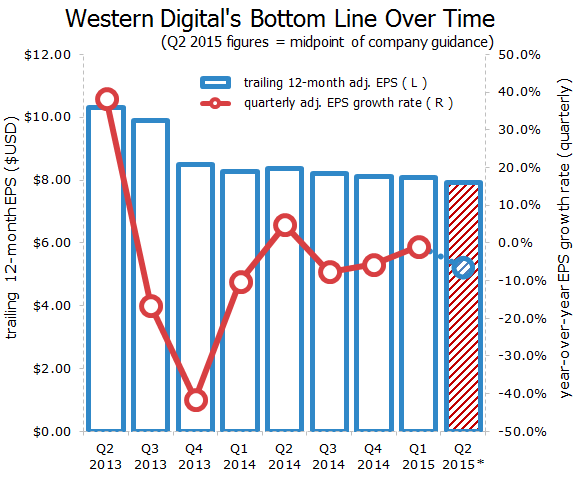

Let's look at Western Digital's progress in chart form now, to get a better idea of how it's progressed and where it might go from here. We'll start with the top and bottom lines:

Source: Western Digital earnings reports.

Source: Western Digital earnings reports.

The general trend hasn't been very good to Western Digital over the past two fiscal years. Western Digital enjoyed a spike in HDD sale prices because of supply constraints at the start of its 2013 fiscal year -- the average selling prices of Western Digital's HDDs peaked in the middle of fiscal 2012 as unit shipments plunged -- and ASPs have remained elevated since. This initially helped the company produce anomalously high growth rates, which have since given way to a multiyear slide. Only four of the nine quarters from mid-2013 to the upcoming second quarter of 2015 have shown year-over-year revenue growth, and Western Digital's adjusted EPS will grow in only two of those nine quarters, if the company's guidance holds up.

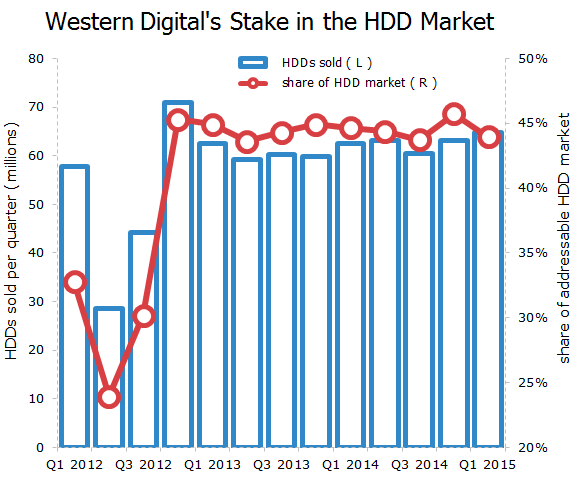

The company hasn't done much to change the calculus of the HDD market in recent quarters, either, as its 44% share of the market in its fiscal first quarter was not only lower than its share a quarter ago and a year ago, but it was also lower than the 44.9% share it reported during the fiscal first quarter of 2013:

Source: Western Digital earnings reports.

This is probably going to be good news for investors in rival HDD maker Seagate (STX +0.00%), which has seen its share of the addressable HDD market slip over the past year. In fact, Seagate's latest quarterly report came out just yesterday, and its market share in the first quarter of 2015 (both companies report on the same quarterly schedule) was up to 40.4% -- a big jump from its 38% share in the final quarter of fiscal 2014, according to Western Digital's own data on the overall HDD market. This recent data shows that the HDD market remains fiercely competitive, and one company's triumph in any given quarter may give way to disappointment in the next.