Green energy stocks are among the most exciting investments right now, and many investors might be wondering if fuel cell stocks could be the next "big thing." After all, in the last year, shares of Plug Power (PLUG -0.44%), Ballard Power Systems (BLDP 0.28%), and Fuel Cell Energy (FCEL 3.66%), have thoroughly trounced the market.

However, there are three fundamental reasons investors should steer clear of these investments -- reasons likely to lose you a lot of money in the long term.

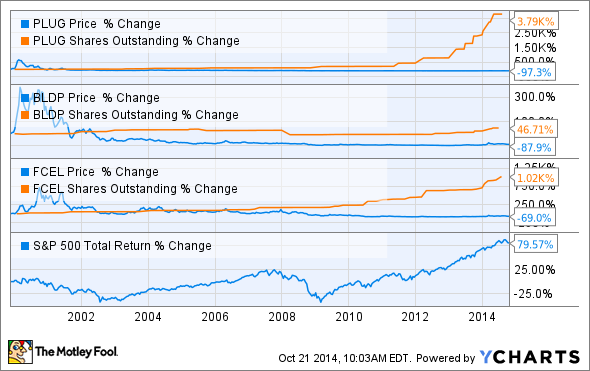

Fuel Cell stocks: diluting away your returns

| Company | 14-Year Annual Total Return | 14-Year Annual Dilution Rate |

| FuelCell Energy | -5.80% | 18.83% |

| Ballard Power Systems | -14.99% | 2.79% |

| Plug Power | -20.83% | 29.89% |

| S&P 500 | 6% |

Sources: Fastgraphs, YCharts.

As the above table and chart illustrate, these companies, with the exception of Ballard Power Systems, have the unfortunate habit of selling massive amounts of additional shares to finance their continued operations. This is understandable as these companies have a 20-year history of racking up large losses.

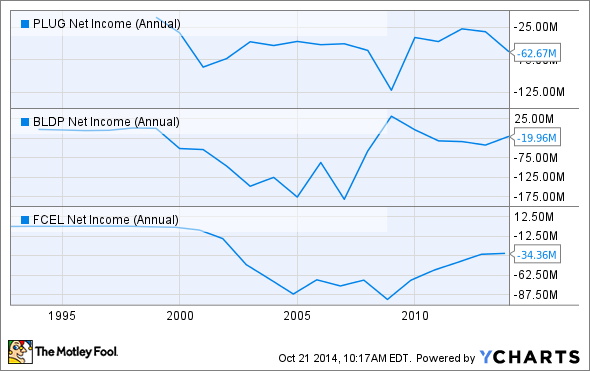

PLUG Net Income (Annual) data by YCharts.

The combination of large losses over decades, along with the frighteningly high dilution rate, has resulted in catastrophic losses for long-term investors. However, large shareholder dilution is just one reason to avoid these companies. Two others are limited market potential and the poor economics of fuel cell technology compared to cheaper alternatives such as natural gas.

What about Plug Power's recent success?

Plug Power supporters may argue that its unfair to point to the company's distant past, given its recent profitable quarter and strong growth. While I disagree, let's examine the bull case for Plug Power to see if the company truly could be a knock-out performer.

Plug's recent run-up was mainly triggered by Walmart's ordering of 1,738 forklift power units and servicing over two years.

This order, along with smaller orders from the likes of Fedex, BMW, Procter & Gamble, Mercedes, and Sysco, allowed the company to report 680 shipments of its GenDrive fuel cells this quarter and post gross margins of 17%, its first positive gross margins since 2003.

The truth behind the profitable quarter

Plug Power's earnings reveal that the company, although reporting impressive annual revenue growth of 125% for the quarter (54% for the first six months of the year), actually had an operating loss of $6.642 million this quarter, and $14.02 million for the first six months of the year. Those losses are on par with last year's operating losses.

The reason for the company's profits was an adjustment to the fair value of its warrant liabilities. Remove that, and the company actually lost $5.75 million, or $0.04/share. Compared to last year, its actual net loss grew 64%.

For the first half of the year, Plug's actual net loss attributable to common shareholders was $72.1 million, up 300% from last year's $18 million. On a per share basis, that's a loss of $0.49/share, up 58% since last year. The only reason it's not higher is because the share count increased 150% during that time, illustrating that Plug's dilutionary days are nowhere near over.

Limited market and earnings growth potential

The fact is that among the three major fuel cell stocks, Plug Power's global potential of $40 billion in the global forklift and delivery systems market is the largest, however, outside of the large Walmart contract, the company has yet to prove it can be a dominant player. For example, between the first and second quarters its backlog declined by 29%.

Unless Plug can prove it can make big inroads into its primary market, and do so profitably, then it may very well miss Wall Street's expected sales growth of 184% this year, and 67% next year. Given its continued losses and ongoing dilution (analysts don't expect Plug to become profitable until 2016 at the earliest), that would likely result in a decline in share price.

What about Ballard and Fuel Cell Energy? Those companies operate in different markets than Plug, so perhaps they make better fuel cell investments. Unfortunately, when it comes to the market and growth potential of Ballard and Fuel Cell Energy, things look even worse for them.

The reason is because Ballard's primary market, remote power generation and gas-fed backup systems for the telecommunications industry, is only a $4.5 billion market, nine times smaller than Plug Power's potential. Meanwhile, Fuel Cell Energy is focused on the $10 billion to $12 billion heat and power generation industry.

| Company | Projected Sales Growth 2013-2015 | First Year of Anticipated Profit | First Year's Projected Profit/Share |

| FuelCell Energy | 30.30% | 2016 | $0.03 |

| Ballard Power Systems | 88% | 2017 | $0.05 |

| Plug Power | 375% | 2016 | $0.03 |

Sources: Yahoo! Finance, Fastgraphs.

As this table shows, when it comes to sales growth, Plug Power is the king of the major fuel cell stocks. It's also tied for the earliest when it comes to anticipated profits, though future projected profits hardly justifies the current valuation of any of these companies.

Fuel cells are not cost competitive and not likely to be for many years

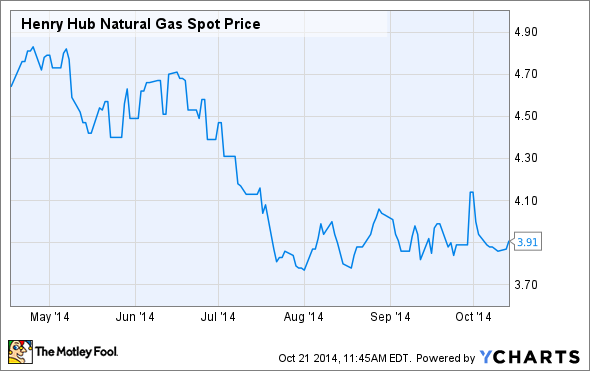

Back in May, two of my Foolish colleagues, Travis Hoium and Tyler Crowe wrote an excellent article explaining why fuel cell backup power systems, which Ballard and Fuel Cell Energy specialize in, were 20%-30% more expensive to operate than natural gas.

Henry Hub Natural Gas Spot Price data by YCharts.

As this chart shows, since that time, the price of natural gas has declined by 18.6%, making Ballard and Fuel Cell Energy's sales pitch to potential customers all that much harder.

Source: Energy Information Administration.

As this chart from the EIA shows, gas prices aren't expected to reach $6/thousand cubic feet (when fuel cells achieve parity with gas) until 2023-2030.

Bottom line

Fuel cell technology is a much-hyped industry, but long-term investors should be warned of its speculative nature and the risks that rapid shareholder dilution, limited market potential, and poor cost competitiveness represent. Plug Power, Ballard Power Systems, and Fuel Cell Energy, the three largest pure-plays in the space, have long track records of heavy losses, broken growth promises, and rampant dilution that have resulted in terrible investor returns. Until these companies can prove they can grow profitably and generate sufficient operational cash flow to make further dilution a thing of the past, I would recommend investors stay away from them.