Brent Crude Oil Spot Price data by YCharts

Recently plunging oil prices have added to the misery of offshore oil drillers such as Seadrill (SDRL +0.00%), Transocean (RIG +2.63%), Ensco (ESV +0.00%), Diamond Offshore (DO +0.00%), and Noble Corp (NE +0.00%). A short-term glut of new rigs, when added to the oil industry's recent desire to cut spending on expensive projects have resulted in shorter contracts, declining day rates, and have many Wall Street analysts questioning the industry's short-medium term growth prospects. For debt laden Seadrill, famous for its sky-high dividend, many are predicting that current market conditions make the dividend unsustainable. This has led to share prices declining to four-year lows and have sent the yield soaring to all time highs.

This article will examine why many analysts believe the dividend is about to be cut to see if the current yield represents either a red flag or an amazing investment opportunity.

Analysts expect dividend cuts

Recently analysts at Goldman Sachs, Barclays, and Wells Fargo have said they expect Seadrill's dividend to be cut.

|

Year |

Seadrill's Projected Annual Dividend Per Share |

|

2014 |

$4.00 |

|

2015 |

$3.96 |

|

2016 |

$2.31 |

|

2017 |

$1.70 |

Source: Fastgraphs.

Specifically, the Wells Fargo analysts cite concerns over falling day rates and the fact that Seadrill has raised funding in the past through sales of rigs to its MLPs, North Atlantic Drilling (NYSE: NADL) and Seadrill Partners (SDLP +0.00%). The ability to continue to do so is now being called into question. As Wells Fargo analysts Matthew Conlan and Tom Rhee put it:

"It has long been our analysis that [Seadrill's] aggressive dividend policy has never been funded solely by the operations of its high-quality fleet, but instead has been funded through the sale of (i) equity (and convertible debt) in [Seadrill], (ii) equity in sponsored "child" entities ([North Atlantic Drilling, Seadrill Partners)]), and (iii) the outright sale of rigs (including sales to its child entities). As long as [Seadrill] could sell these assets and equity for premium prices, it could sustain a high dividend, which in turn supported a premium valuation for [Seadrill's] stock price. As equity and asset values are slipping, we think [Seadrill] may fail to secure the sales prices and external financing required to sustain its current dividend.

Meanwhile Lenny Zephirin, an analyst for the Zephirin Group, recently told TheStreet that the probability of Seadrill having to cut its dividend in the near term are: "high; however, the chance of the company skipping a quarterly dividend payment is even higher."

I understand these analysts' concerns, especially given Seadrill's recent sale of the West Vela rig to a subsidiary of Seadrill Partners for 27.5% less than a similar rig back in March, news that sent shares plunging 8% that day. However, I disagree with their conclusion and think that Seadrill's dividend is safe for three primary reasons.

Factors protecting Seadrill's dividend

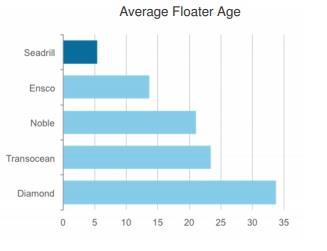

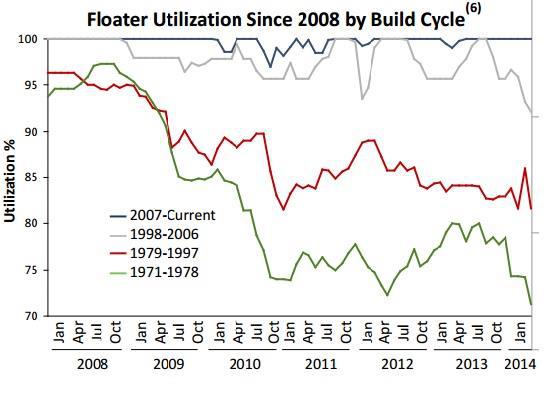

Seadrill's fleet of drill ships is among the youngest in the industry, which should help it secure contracts for its upcoming new builds as well as those rigs coming off contract within the next few years.

Source: Seadrill 42nd Annual Howard Weil Energy Conference presentation.

Source: Pacific Drilling May 2014 investor presentation.

As these two slides show, Seadrill's average drill ship was constructed in 2009 for which the utilization rate for those rigs remains near 100%.

In addition, Seadrill recently procured a two-year contract with ExxonMobil's Nigerian subsidiary for its West Saturn new build for a highly lucrative day rate of $633,750.

This recent contract, for a day rate that's 89% higher than recent contracts for older rigs such as those of Transocean's Leader and Amirante rigs (for $335,000 per day each) gives me confidence that Seadrill's fleet of newer, state-of-the-art rigs, is less likely to be affected by the industry downturn than its competitors.

The second reason I'm confident in Seadrill's dividend sustainability is that the company has both of its MLPs to use as a source of cheap financing. For example, in the first quarter, Seadrill sold 51% of its stake in the West Auriga rig to Seadrill Partners for an implied value of $1.24 billion. This netted the company $355.4 million in cash to reduce debt and secure the dividend.

Though the most recent drop down was for a substantially lower price with an implied value of $900 million, Seadrill will still gain $238 million from the deal and maintains about 75% economic interest in the rig.

In addition, Seadrill has 17 Ultra Deep-Water, or UDW, rigs remaining that it could drop down to its MLPs. If it obtains the same terms as its most current sale, these rigs would net the company $4.046 billion in cash.

Even if the prices obtained for these rigs are lower, the billions of dollars Seadrill could raise from its MLPs could still potentially secure the dividend long enough for the offshore drilling market to recover.

Finally, I feel confident in the sustainability of Seadrill's dividend because, as my Motley Fool colleague Matt DiLallo recently explained, Seadrill's management is "becoming increasingly confident that the dividend's safety can extend well into 2016 even without any significant recovery in the offshore drilling market." He continued: "Part of this security is because it can use Seadrill Partners as a source of capital to keep the dividend afloat."

Don't get me wrong: Management confidence should never be the sole reason for investing in a company. However, given the company's ability to thus far keep securing lucrative contracts during highly challenging market conditions, as well as John Fredrikson's (the founder and largest shareholder) recent purchase of 2 million shares -- I feel more confident taking management at its word that the dividend is safe.

Bottom line

Current and potential investors in Seadrill shouldn't misunderstand me, the risk of a Seadrill dividend cut is real. Otherwise shares wouldn't be yielding 18%. However, I continue to believe that Seadrill represents an amazing, if more speculative, income investment opportunity. Given the positive long-term prospects of the offshore drilling industry, I think investors should consider whether Seadrill deserves a small position as part of a diversified income portfolio.