ConocoPhillips' (COP +0.82%) stock is off 17.7% from its most recent high. This is largely the result of falling oil prices, which have tumbled in recent weeks as we see in the following chart.

While oil prices will always have an impact on ConocoPhillips' stock price, it's not the only factor that could fuel the stock in the future. In fact, some reasons for optimism surfaced in the company's third-quarter report that suggests the company doesn't need higher oil prices to fuel a rising stock price. Here are three reasons why the company's stock could rise even if oil prices stay low.

Low cost of supplies

ConocoPhillips doesn't need high oil prices to make a lot of money as the company's supply costs are rock bottom, which we can see in the two charts on the following slide.

Source: ConocoPhillips Investor Presentation

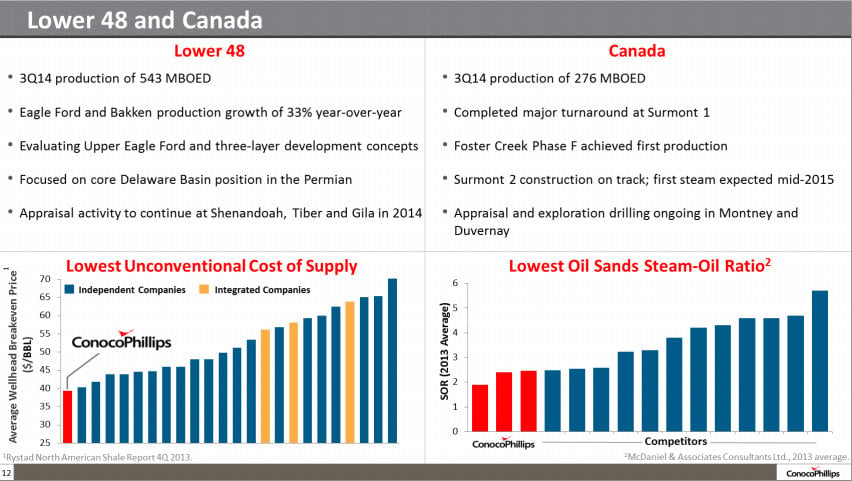

Note that when it comes to unconventional shale plays, specifically, the Bakken and Eagle Ford, ConocoPhillips has the lowest cost of supply in the industry. Because of this the company can make money on its oil production with oil prices as low as $40 per barrel. Further, in Canada ConocoPhillips owns a stake in three of the lowest cost oil sands projects as measured by the steam-to-oil ratio. This enables ConocoPhillips, and its partners Cenovus Energy (CVE +4.30%) and Total (TOT +0.00%), to produce oil for as low as $35 per barrel yielding a lot of cash flow even in a lower oil price environment.

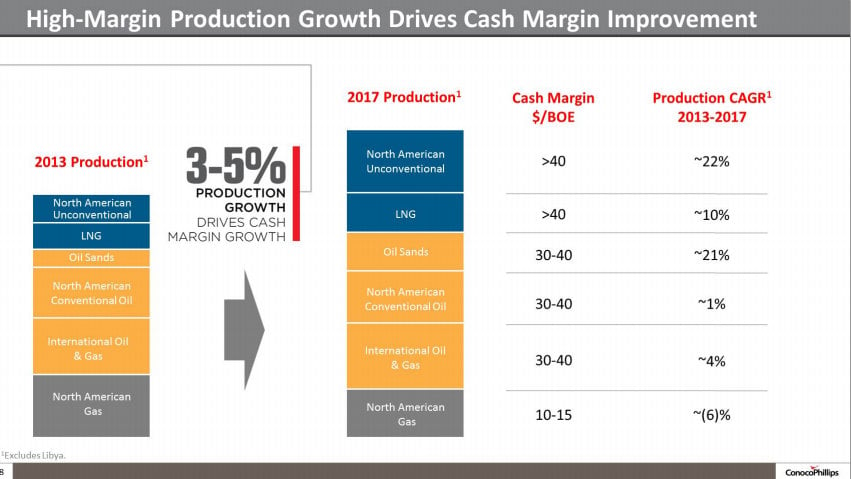

These low cost supplies also represent ConocoPhillips' two fastest growing production areas. As we see on the following slide, the company plans to grow production from unconventional sources by 22% per year through 2017 while also growing production from the oil sands by 21% per year over that same time frame.

Source: ConocoPhillips Investor Presentation

This focus on its highest margin production will enable the company to produce strong cash flow even if oil prices remain weak.

More flexible than ever

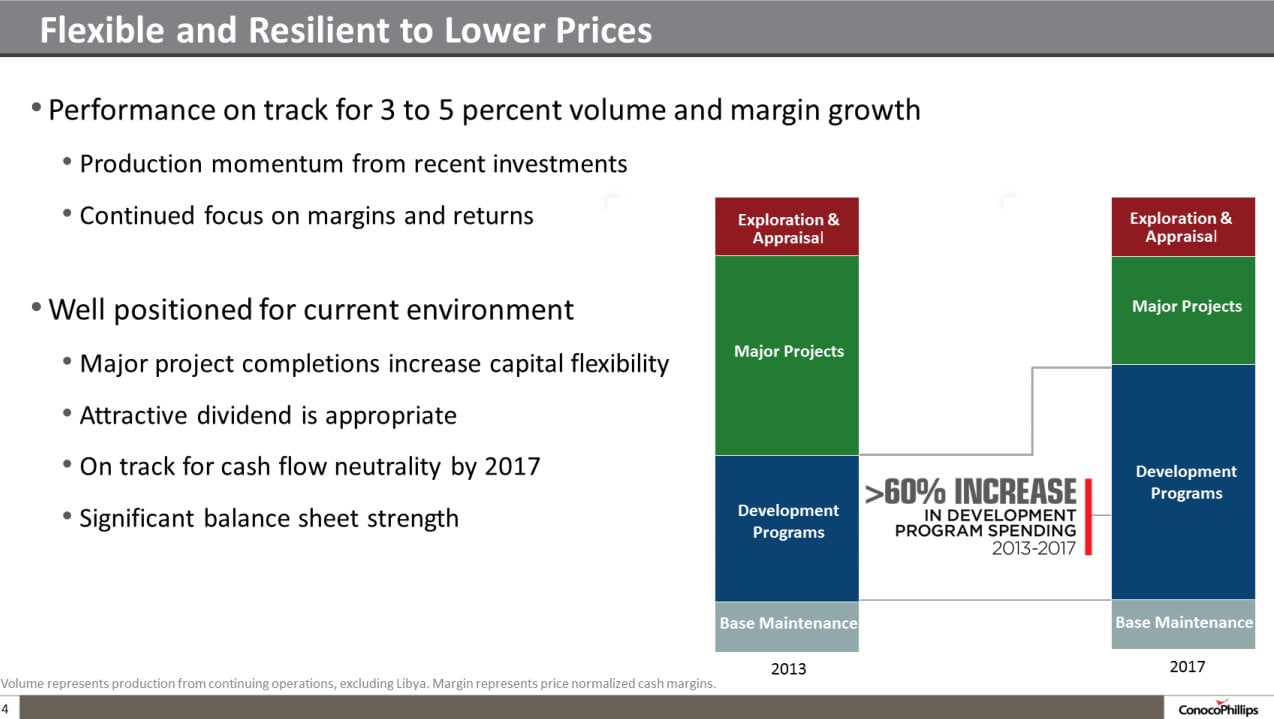

This year ConocoPhillips expects to spend $16.7 billion on capital projects. Of that amount 35%, or nearly $6 billion was spent on major capital projects around the world. However, 2014 represented the peak spending for several major projects including APLNG in Australia and the second phase of its Surmont oil sands project in Canada. With that peak now past, ConocoPhillips has more flexibility than ever to cut capital spending as well as focus capital on projects that will yield an immediate boost to cash flow.

As this next slide points out, the company's capital plan is shifting from a focus on major projects to development programs.

Source: ConocoPhillips Investor Presentation

This enhanced flexibility will allow the company to direct its spending on the development projects that will move the needle, while at the same time pulling back spending in areas that are weaker. That will enable the company to make more money even if oil prices remain weak.

Dividend will grow even if oil prices don't

The final reason why ConocoPhillips doesn't need higher oil prices to fuel an increase in its stock price is because of the priority the company has placed on its dividend. CEO Ryan Lance noted on the company's third-quarter conference call that:

As we think about capital levels going into 2015, we first consider all of our priorities for investment. As we have said, consistently since the spin, our top priority is the dividend. This is an important part of our investment thesis as the dividend provides discipline in our capital allocation process, and we believe it is important in a mature business. So, no change to the outlook on the dividend.

This is important because a rising dividend typically yields a rising stock price because the higher yield entices income investors. Given the priority ConocoPhillips has placed on its dividend, there's reason to believe the stock could head higher even if oil prices don't budge.

Investor takeaway

ConocoPhillips' stock price has taken a hit due to falling oil prices. However, the stock price could very well head higher even if oil prices are not what's fueling those gains. Thanks the company's low cost of supply, flexibility to spend on needle-moving development and a growing dividend, ConocoPhillips doesn't necessarily need higher oil prices to push its stock price higher.