China's largest online dating platform, Jiayuan.com International Ltd (DATE +0.00%), is very much a company in transition and its latest earnings report reflects the changes afoot. Essentially, the company is in the process of redesigning and relaunching its mobile offering in December, and the company is looking forward to increasing the monetization of its mobile platform. Unfortunately, this shift has somewhat skewed the key metrics at the company. Here is a look at its third-quarter results, reported this morning.

Before going into detail, readers should note that Jiayuan is a Chinese company and primarily reports in RMB. All the numbers in this article will be quoted and calculated in RMB, unless otherwise stated.

Third-quarter revenue grew an impressive 25.5%, but gross profit only grew 5.1% as gross margin fell to 53.9% from 64.3%. While the gross margin movement is somewhat disappointing, the revenue figure of $26.3 million was ahead of analyst estimates of $25.4 million. However, earnings came in a little light with adjusted diluted EPS of $0.02 versus analyst estimates of $0.03.

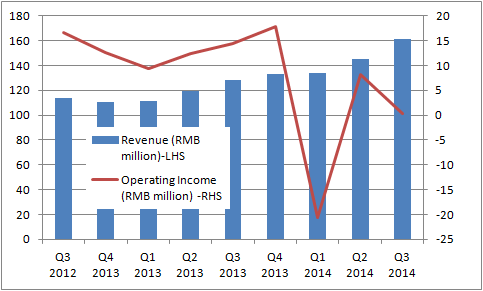

A quick look at revenue and operating income demonstrates the trends.

Source: Jiayuan.com International Ltd Presentations

Essentially, the reason why operating income fell to just RMB 305,000 from RMB 14.4 million in the same quarter last year, is because operating expenses rose a whopping 26.7% to RMB 86.7 million from RMB 68.5 million last year. Within this increase, sales and marketing expenses rose RMB 14.2 million to RMB 64.9 million "primarily related to a special marketing campaign for Chinese Valentine's Day in August," according to the third-quarter 2014 announcement. In other words, the cost increase wasn't just about preparing for the redesigning of its mobile platform.

Jiayuan.com earnings analysis

It's too early to say how the new mobile site will perform, but on the earnings call, management spoke of "significant new monetization" opportunities with its mobile site. The opportunity being to try and increase average revenue per user, or ARPU, -- probably the most coveted metric with this type of business. The second most sought after metric is likely to be average monthly paying user accounts. In the end, an online dating site will live or die based on how many paying customers it has, and how much they are spending.

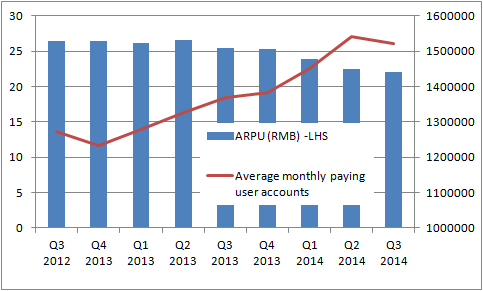

A look at the two key metrics.

Source: Jiayuan.com International Ltd Presentations

Paying user accounts have grown, -- albeit with a sequential decline in the current quarter -- but ARPU has been stagnant or declining for a while now.

Moreover, its online-based revenue -- the company also offers offline personalized matchmaking services -- actually fell 1.7% to RMB 106.7 million, or 66% of net revenue. The company cited the "decline in ARPU as the company shifts its product offering toward mobile."

Meanwhile, personalized matchmaking services saw revenue rise 259% to RMB 49.5 million, or 30.6% of revenue in the quarter.

Looking ahead, management gave revenue guidance of RMB 162 million to RMB 164 million for the fourth quarter, implying a 22.5% increase from the same period last year, but minimal growth sequentially.

The takeaway

All told, the key to the company's future is likely to be the growth in its new mobile platform -- due to be launched in December -- and its personalized matchmaking services. Revenue came in ahead of expectations in the third quarter, but earnings missed analyst forecasts as the company ramped up spending in order to try and generate growth. Investors will be watching the ARPU number very keenly in future quarters, and keeping an eye out to see if the new mobile site increases underlying performance in 2015.