A lot is said about the stocks Warren Buffett buys through Berkshire Hathaway (NYSE: BRK-A)(NYSE: BRK-B). But Buffett wants you to see that those are starting to matter less and less to the company itself.

What Buffett wants you to know

Sections of the Berkshire Hathaway annual report are often repeated on a yearly basis. For example, in every year's report you can find a 1996 booklet Buffett wrote called "An Owner's Manual." You'll also see the six things Buffett requires of any business Berkshire Hathaway would acquire.

But one of the most fascinating things is the recent addition of a section from the 2010 letter to shareholders entitled "Intrinsic Value -- Today and Tomorrow." This has been included in the last three annual reports, with no indication that it will disappear anytime soon, suggesting it's something Buffett wants to ensure individuals note.

Source: The Motley Fool.

The critical thing to see

The section details exactly how Buffett and longtime Berkshire Vice Chairman Charlie Munger gauge the true value of Berkshire Hathaway. Unsurprisingly, the first thing noted is the value of the company's investments in stocks and bonds, as well as cash equivalents held by Berkshire.

After all, Berkshire's monstrous insurance business not only makes an underwriting profit, but it also provides a float -- the difference between what it has taken in through premiums versus what it will eventually pay out -- that can be invested. At last count, that float stood at more than $77 billion.

Buffett's second point in this section was to highlight Berkshire Hathaway's large stable of noninsurance businesses, including Burlington Northern Santa Fe railroad, Berkshire Hathaway Energy, Lubrizol, Marmon, and many more.

Yet what Buffett really wants us to see is this: "In Berkshire's early years, we focused on the investment side. During the past two decades, however, we've increasingly emphasized the development of earnings from non-insurance businesses, a practice that will continue."

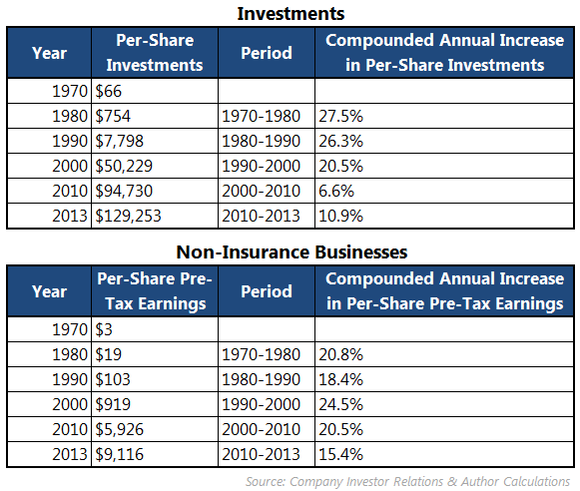

This is evidenced by the following powerful example of the difference between the relative growth of Berkshire Hathaway's investments versus the earnings provided by its noninsurance businesses:

From 1990 to 2013, the per-share earnings from its noninsurance businesses grew at an average annual rate of 21.5%, while its investments rose at 13%.

That staggering difference resulted in the earnings of the noninsurance businesses standing nearly 90 times higher at the end of 2013than in 1990, versus "just" a 16 times greater value in its investments.

The key takeaway

For good reason, we are quick to watch how Buffett and Berkshire Hathaway invest in companies that we too can buy on the open markets.

But when we consider investing in Berkshire Hathaway itself, we must see that those investments are starting to matter less and less to not only its success, but to its true value as well.