Johnson Controls (JCI +0.59%) investors must be disappointed this year as they have watched their stock underperform the S&P 500 by nearly 14% to date in 2014, at the time of this writing. However, the poor stock price performance largely has resulted from end-market conditions rather than anything the company has done. On the contrary, the multi-industrial company's management has made a host of exciting initiatives that could propel earnings higher in the future. With these initiatives in place, and some of its end markets starting to look better, is now the time to buy into Johnson Controls?

Source: Johnson Controls.

What happened to Johnson Controls in 2014

Johnson Controls has actually had had a strong year operationally. It raised its adjusted earnings per share by 24.7% in its fiscal year ending in September, increasing segmental margin by almost a percentage point in the process. Moreover, analysts project 13.8% and 16% EPS growth, respectively, for the next two years. Johnson Controls is definitely a growth stock, but is it a good value?

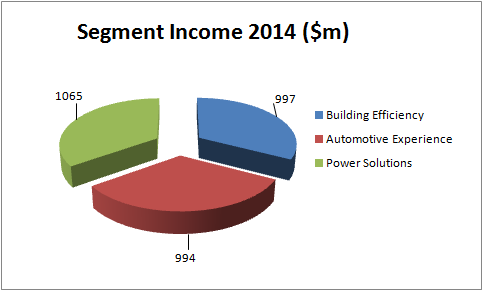

Before I attempt to answer this question, a few words on why the stock has underperformed this year. The company reports three segments, which contributed the following income amounts in its fiscal 2014.

Source: Johnson Controls Presentations.

It's pretty much a three-way split. You can think of power solutions (car batteries) as basically a play on automobile miles driven -- when cars are used more, they tend to require new batteries. Typically, about three-quarters of power solutions sales go to the aftermarket, with the rest going to original equipment manufacturers, or OEMs. The building efficiency segment sells heating, ventilation, and air-conditioning equipment to global construction markets, with U.S. institutional markets being its traditional core. The automotive experience sells car seats and interiors, primarily to automobile OEMs.

Roughly speaking, 45% of income comes from automobile OEM production (automotive experience and power solutions), a third from construction markets (building efficiency), and a quarter from automobile aftermarket demand (power solutions).

Essentially, a weaker-than-expected institutional construction market led to frustrating conditions in Johnson Controls' building efficiency segment in 2014, while a combination of sluggish economic growth and a warm winter in Europe caused power solutions customers there to de-stock car battery inventories and eschew new purchases. By way of contrast, the automotive experience segment outperformed expectations in 2014, with its European operations reporting surprisingly strong growth. More detail on what happened in 2014 and the company's recent fourth-quarter results can be found here.

Looking to 2015 and beyond

For a balanced view on Johnson Controls' prospects in 2015 and beyond, readers can read these bull and bear cases for the company. I've summarized the three key pros and cons from those articles below.

| Bull Points | Bear Points |

|---|---|

| Industry data suggests a good recovery in U.S. institutional construction markets (building efficiency). | China's automobile sales appear to be slowing (automotive experience). |

| Restructuring of the auto experience segment is intended to lead to a significant increase in margin and profitability in future years (automotive efficiency). | Its European automobile OEM customers don't appear to be outperforming a sluggish European production market anymore (automotive experience). |

| Management forecasts significant increases in free cash flow in the next two years. | Johnson Controls has a patchy record of free cash flow conversion. |

Looking to 2015, management has a number of initiatives in place to generate growth and increase margin and free cash flow conversion. In the building efficiency segment, these include separating North American operations from its global business, divesting its facilities management business, and forming a joint venture with Hitachi to expand its product offerings. Meanwhile, automotive efficiency has a joint venture planned for its underperforming auto interiors business.

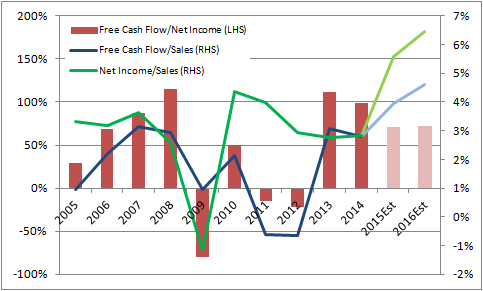

The following chart demonstrates how all these measures could come together to increase margin and free cash flow conversion. The chart uses analyst estimates for revenue and net income, and management's forecast for free cash flow.

Source: Yahoo! Finance, Johnson Controls Presentations, author's analysis.

Clearly, significant increases in free cash flow conversion and income generation are expected in the next two years.

Is Johnson Controls a good value?

All told, it's clear that the company has strong earnings growth prospects, but it will need to execute well. The good news is that its internal performance was good in 2014, and management has been aggressive in restructuring the business. Moreover, end-market conditions look set to improve in its building efficiency segment, and North American car production continues to grow.

However, the company's valuation suggests there isn't much margin of safety for error. Its current enterprise value (market cap plus net debt) is about $39.7 billion. In other words, based on its internal forecast of $1.7 billion and $2 billion in free cash flow for the next two years, the stock is on a forward free cash flow/enterprise value yield of 4.2% and 5% for the next two years, respectively. Frankly, I would want a cheaper entry point into the stock.