In late September I took a close look at Devon Energy (DVN -1.20%) to see if its stock was cheap enough to buy. I compared the independent natural gas and oil producer's valuation to its closest peer group, and to its own historical valuation. After a lot of number crunching I reached the following conclusion:

While Devon Energy isn't a screaming bargain relative to its peers, it's not overvalued by any means. That suggests that the company just might be a good buy today for an investor looking for oil-focused growth and isn't concerned about paying up a little bit for that growth. Otherwise, Devon Energy makes a solid watchlist candidate for bargain hunters to watch in case future buying opportunities arise amid falling oil prices.

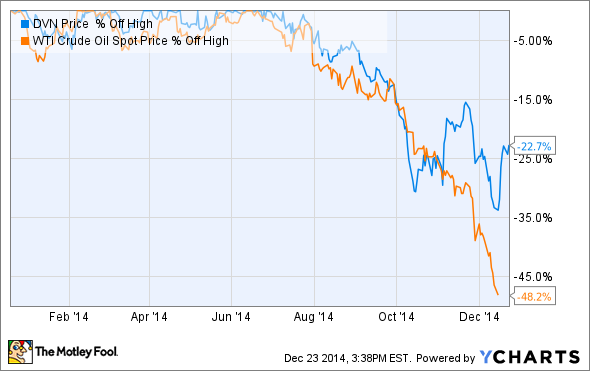

Note that last sentence. Turns out the continued plunge in oil prices might have created just such a buying opportunity as Devon's stock falls:

Along with that new data point, we also have another quarter of stellar results in the books to factor into an updated valuation. Given these changes, I thought I'd take another look at the company's valuation to determine if investors finally do have that buying opportunity.

Drilling down into the numbers

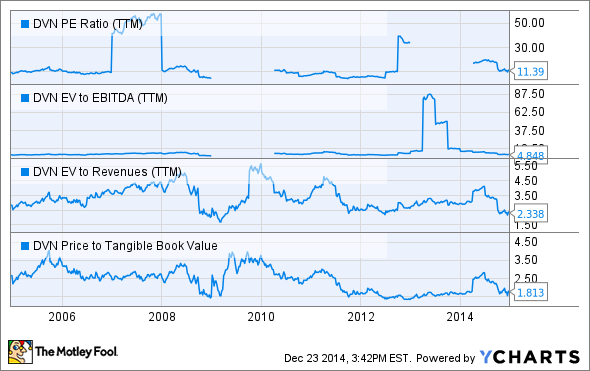

My last review of Devon Energy's valuation compared a basket of common energy valuation multiples to the company's historical average. Here's what that data looked like as of the end of the second quarter when reported in August.

|

Devon Energy |

2014 |

Historical Average |

|---|---|---|

|

Price/Earnings |

18.6x |

14.9x |

|

Enterprise Value/EBITDA |

6.8x |

5.5x |

|

Enterprise Value/Total Revenue |

3.4x |

3.4x |

|

Price/Tangible Book |

2.2x |

2.5x |

Source: S&P Capital IQ.

This time I'll look at that same basket of numbers, but in a slightly different way. Here's how these numbers have trended at Devon Energy over the last 10 years.

DVN P/E Ratio (TTM) data by YCharts.

As seen in the charts, the data can be a bit skewed at times. For example, the company's P/E ratio has occasionally been nonexistent, or exorbitantly high. That can happen when Devon Energy reports a quarterly loss, as it did in the first quarter of 2013. The company in that quarter lost $3.34 per share due to a big noncash charge, as falling oil and NGL prices forced Devon to write down the value of some of its assets. These charges are quite common among energy companies, which is why the P/E ratio doesn't always make a great valuation metric.

With that in mind, in looking back we want to look for normalization and averages. This shows that the company's current valuation metrics are all below the company's average over the past decade -- suggesting that now is a good time to buy thanks to a stock that appears undervalued, assuming energy prices normalize.

Investor takeaway

This is not to say that Devon Energy's valuation won't keep falling along with oil prices. The company's forward earnings are also likely to come down, as the drop in oil prices will weaken its cash flow and could force Devon to take another impairment charge in the upcoming quarter. All that aside, for investors who are bullish on oil and natural gas prices over the long term, there appears to be a very compelling opportunity to buy as the stock's valuation is well below its historical average and at one of its lowest points in some time.