The nosedive in oil prices has sent riskier investors hunting for opportunities and conservative investors searching for ways to protect against further falls. Both, it seems, have stumbled upon two ETFs from Direxion Investments. But both harbor fatal flaws for long-term investors.

For the past five years, the Direxion Daily Energy Bull 3x (ERX +3.37%) and the Direxion Daily Energy Bear 3x (ERY -3.42%) have together traded about 2.5 million shares each day. Since October, they've averaged over 6 million.

Before we get into their flaws, let's talk about what these ETFs are supposed to do. They are both leveraged ETFs, so called because they attempt to multiply -- or leverage -- the return of some part of the market. In this case, the target is triple the return of energy stocks. If energy stocks rise 1%, the Energy Bull 3x is supposed to go up 3% and the Energy Bear 3x is supposed to fall 3%.

On the surface, the surging interest in these ETFs makes sense. These two ETFs are intended to deliver 3 times (in the case of Energy Bull) or negative 3 times (Energy Bear) the return of energy stocks as a whole. With volatile oil prices come volatile energy stocks, and unique opinions about the future of those stocks abound. Investors with high convictions might opt to amplify their returns -- assuming they are correct -- by buying one of these leveraged ETFs.

Deeply flawed investments

The Energy Bull and Energy Bear's fatal flaws become immediately obvious when you look at their price history.

Source: YCharts

Over this four-year period, energy stocks, as represented by the Energy Select Sector SPDR ETF (XLE +1.77%), returned 19%. So one might expect Energy Bear to fall about 60% and Energy Bull to rise about 60%. Energy Bear fell 82%, even further than intended. And shockingly, Energy Bull also fell 10%.

Huh? The problem is that Energy Bear and Energy Bull are biased downward over time. This becomes even more evident when you see Energy Bear's full price history since its 2008 debut.

Source: YCharts

What causes this long-term erosion of value? The flaw is embedded in the funds' DNA.

A flaw is born

Technically, Energy Bull and Energy Bear are supposed to triple or inversely triple the one-day return of energy stocks. This they accomplish very well.

But consider what happens over time. Let's say energy stocks close at $100 on Monday. On Tuesday they rise 25% (to $125), and on Wednesday they fall 20% (back to $100). What does Energy Bull -- which is supposed to triple the return -- do? On Tuesday it rises 75% (to $175), and on Wednesday it falls 60% (to just $70). In a period where energy stocks broke even, Energy Bull manages to lose 30%.

Of course, this example uses extreme price movements. It illustrates, though, how leveraged ETFs break down over time. Like other such ETFs, Energy Bull and Energy Bear invest in a complex array of derivative contracts in order to deliver on their triple-return promise. On Tuesday night -- back in our example -- the fund managers need to rebalance those contracts to make sure the ETF will keep its promise the following day.

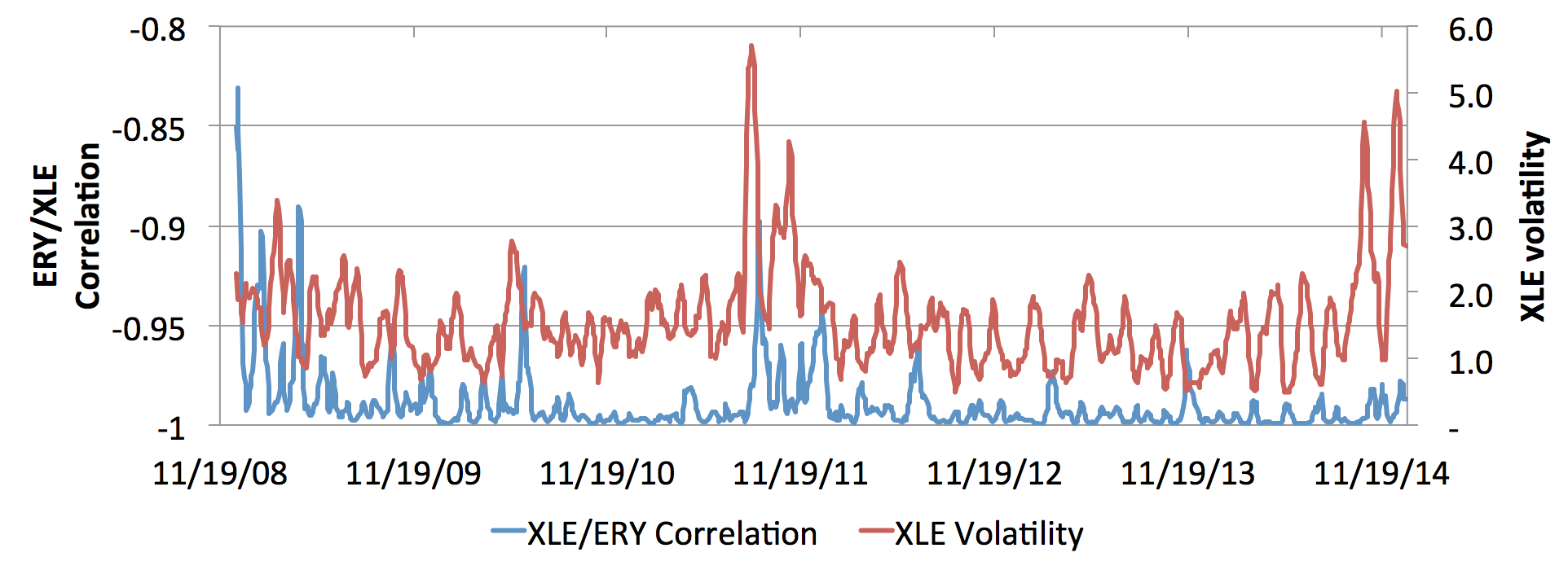

Any investor looking to hold these ETFs more than a few days is at risk of being burned. This is especially true in times of high volatility, when Energy Bull and Energy Bear break down even faster than usual.

Source: S&P Capital IQ and author's calculations.

The more volatile energy stocks are, the more rebalancing each ETF needs to do each day, and the more the ETFs diverge from energy stocks. Worse, investors pay a 0.95% management fee for the privilege of watching their money shrink over time. Long-term investors should stay far away from Energy Bull and Energy Bear, especially in volatile markets such as these.

How to profit from their shortcomings

The enterprising investor might take this conclusion a step further. Because these ETFs erode over time, they can make excellent short candidates. At the moment, betting against Energy Bear is particularly attractive.

Since it launched over six years ago, Energy Bear lost value in 99% of rolling one-year periods. As we've seen, it deteriorates fastest in times of high volatility, and volatility hasn't been this high in the energy sector since 2011.

Even better, energy stocks as a whole are relatively cheap after a 23% decline over the past six months. Flaws aside, shorting Energy Bear is similar to buying energy stocks. As energy stocks rebound -- whether this quarter or three years from now -- the short will profit further.

Protect first, profit second

No investor should own leveraged ETFs over the long term. Beware Energy Bull, Energy Bear, and the many others like them.

If you think -- as I do -- that energy stocks will perform well in the coming years, buy a basket of them. There's no need to leave your comfort zone or dabble in complex funds to profit when the sector rebounds.

Yet, investors with a stomach for volatility shouldn't outright ignore these ETFs. When the stars align, as I believe they have for Energy Bear, they can make enticing short opportunities for more experienced investors.