American Express (AXP 0.72%) will announce its 2014 fourth-quarter and full-year earnings on Jan. 21, and there are three things investors need to watch for when the earnings are released.

Can it still outpace its peers?

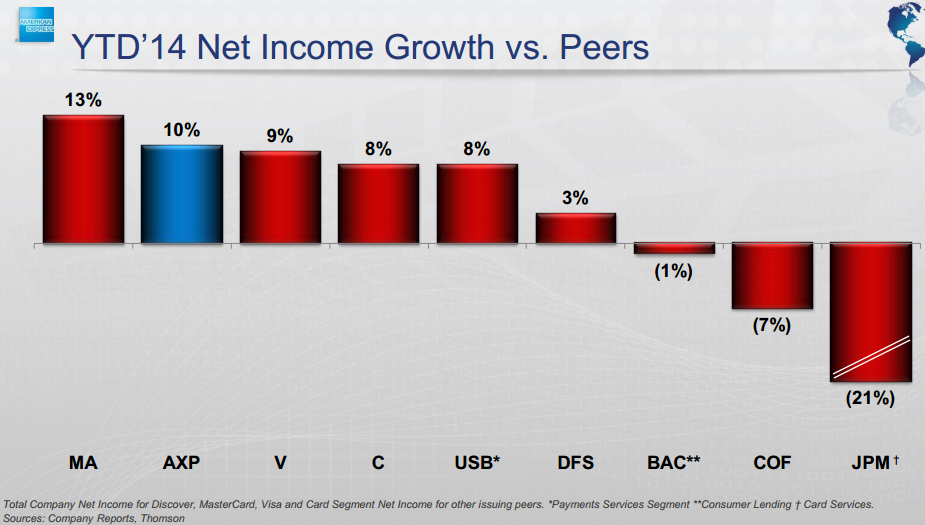

At the Goldman Sachs U.S. Financial Services conference, American Express revealed it was behind only MasterCard (MA +0.66%) in growing its income through the first nine months of the year:

Source: American Express presentation at the Goldman Sachs U.S. Financial Services conference.

It should be noted AmEx watched its revenue rise by just 3%, so its sizable gain in income was attributable to disciplined expense management. By comparison, MasterCard's revenue rose nearly hand in hand with its net income, with revenue up 13.4% and net income up 13%.

As a result, one of the first things to look for is whether this impressive growth in net income continued in the fourth quarter, especially in light of the recent news of the decline in retail spending. As reported by Reuters, "excluding automobiles, gasoline, building materials and food services, sales fell 0.4 percent last month after a 0.6 percent rise in November."

This may lead to lower revenue for companies in the credit card industry, so it will be important to see how net income trends at AmEx and whether or not the company can continue to operate efficiently to the benefit of its bottom line. One month of reduced consumer spending will in no way hurt the long-term investing prospects of American Express, but investors should monitor the company's growth trends, especially relative to its peers.

Can we get tangible evidence of growth in OptBlue?

In a review of the third-quarter earnings call, I noted it was encouraging to hear chief financial officer Jeff Campbell say, "We also made progress on several newer fronts this quarter, attracting additional partners to our OptBlue program, acquiring new card members on our EveryDay product, and participating in the upcoming Apple Pay mobile wallet launch."

OptBlue and EveryDay are products aimed at allowing American Express to be more widely used at merchants (in the case of OptBlue) and by consumers (in the case of the EveryDay card), which could provide meaningful growth opportunities for the company. But the fact remains that the company has provided little empirical data to enable investors to determine exactly what "progress" for these programs means.

So, with the full year officially in the books, it would be nice to see what these programs -- OptBlue, the EveryDay card, and others -- could mean to the future of American Express. Then investors could see whether these initiatives are marginal or material and in turn use that information to help guide their investment decisions.

Further guidance on share repurchases

In March 2014 we learned the Federal Reserve approved AmEx's plan to repurchase up to $4.4 billion shares in 2014 and $1 billion in the first quarter of 2015.

And, as shown below, since 2010, share repurchases have been instrumental in propelling earnings-per-share growth well beyond the aggregate gains in net income:

Given that American Express' approved share repurchase plan will conclude at the end of this quarter, one final thing for investors to monitor is whether or not management provides any guidance on how American Express will allocate its capital in the future. Will it continue to aggressively repurchase shares, as its stock has been essentially flat over the last year? Or will it once more raise its dividend?

Considering that American Express still trades at an attractive P/E of 16.2 and seeks to return 50% of its capital back to investors through dividends or share repurchases, the logical course of action would be to continue its sizable repurchase plans. But if the company indicates otherwise, it could be a cause for concern.

Of course, because it's ultimately up to the Federal Reserve's discretion whether or not the plan is approved, this issue will be fully known in March following the Fed's analysis of AmEx in its Comprehensive Capital Analysis and Review, but investors should be curious to know what guidance -- if any -- the company provides surrounding its capital allocation decisions.