It's hard to argue against the long-term track record of Big Oil companies when it comes to generating wealth for their shareholders. When you include the magical power of reinvested dividends, Big Oil companies have soundly beaten the S&P 500 since 2005.

Knowing the effect these stocks can have on one's portfolio, we asked three of our energy analysts to make their pitch for why you might pick one of these companies over the others today. Here's what they had to say.

Matt DiLallo: ConocoPhillips (COP -1.08%) has always been on the edge of being considered a Big Oil company. It's not one of the five supermajors, nor is it an integrated oil company with refining operations (it jettisoned those in 2012). That said, it is the largest U.S. independent oil and gas company, meaning it certainly is in the realm of Big Oil. Furthermore, with all of its business tied to the development of said resources, I think it is nimbler than its larger brethren and a much better buy right now.

ConocoPhillips' focus since 2012 -- when it spun off its downstream segment to Phillips 66 -- has been on growing its production and its margins by 3%-5% per year. To get there it shed lower-margin assets and reinvested those proceeds into high margin growth. That has led to steady improvement in the company's returns and margins over the past five years.

COP Return on Equity (TTM) data by YCharts.

ConocoPhillips' valuation, which had improved along with those returns, has now fallen a bit from recent highs thanks to the shellacking in the oil market. As this next chart shows, the company's valuation across a basket of metrics is close to its numbers right around the time of the spinoff.

COP EV to EBITDA (TTM) data by YCharts.

This shows the market is discounting all the progress the company has made over the past couple years -- progress that not only put it in a better position to endure the current downturn, but to thrive once conditions improve. Add in the compelling valuation and other incidentals like a strong balance sheet and a compelling dividend yield, and ConocoPhillips is clearly a great Big Oil stock to buy now.

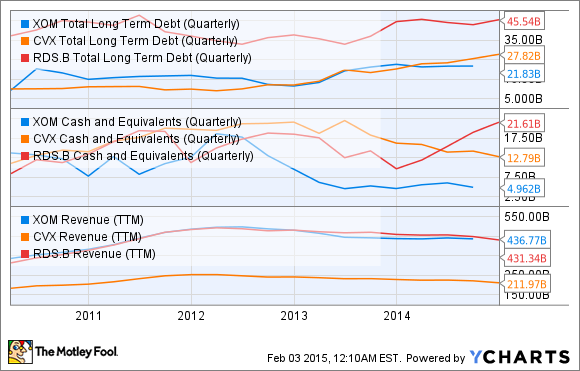

Jason Hall: I'm going with the safe bet here, in ExxonMobil (XOM 0.15%), even though Mr. Market has taken a bigger bite out of the stock price of most of its Big Oil peers. Furthermore, the company's balance sheet has been trending in the wrong direction lately:

Cash and equivalents is at the lowest level in years, while long-term debt is the highest it's ever been. However, the company is still in an enviable position, considering that it carries a debt level similar to companies half its size, or half the debt of its closest supermajor competitor, if you prefer:

So why ExxonMobil? Because the company's management might be the best in the business at conservative capital allocation, and investors in the oil and gas business want conservative hands at the wheel of the companies they invest in today. Other oil majors' stock might outperform ExxonMobil over the next few years, but if oil prices stay down longer than anyone expects, investors who choose defensive investments such as ExxonMobil will be glad they did. If oil prices bounce back sooner rather than later, you'll still own shares of one of the best operators in the business.

Tyler Crowe: I'm going to slightly stray away from my norm, which is to recommend ExxonMobil -- thanks Jason -- and go with Chevron (CVX 1.06%) instead. While ExxonMobil has some advantages in a head-to-head comparison, two things pop out at me right now with Chevron.

First, Chevron's balance sheet gives the appearance that the company might be ready to do something big, such as an acquisition or initiating a major stock buyback program. As management stated at last year's analyst meeting, its total capital employed is disproportionately tied up in projects that aren't yet producing, such as its Australian LNG terminals Gorgon and Wheatstone, as well as several Gulf of Mexico developments. As these projects come online, much more of its capital will be from cash-generating assets.

The other component that suggests something big could happen soon is Chevron's high level of dry powder, in terms of excess cash on hand and lots of room to take on debt. Chevron's cash on hand of close to $15 billion and a current ratio of 1.27 times means it has a bunch of cash that isn't needed for working capital, and the company's debt-to-capital ratio of 12% is on the low end of its target ratio of 10%-20%.

The other reason Chevron looks appealing today is that it is so cheap. By deducting cash from the company's market cap, you get a price-to-earnings ratio of less than nine times. Granted, earnings are expected to decline as long as oil prices remain low, and that will eventually be reflected in the P/E ratio, but all that firepower to do something in this down market could lead to big rewards down the road.