Thinking about investing in an insurance company? Then you need to know one number: the combined ratio.

What is it?

In short, the combined ratio is the measure of the premiums an insurer earns -- i.e, the revenue it collects from policy holders -- relative to the total it pays out in claims, plus its expenses.

For example, if for every $100 an insurer collects in premiums, it pays out $80 in claims and expenses related to those claims, plus another $15 in operating expenses, it would have a combined ratio of 95%.

The loss ratio -- which measures how much an insurer pays out in claims or losses divided by what it receives in premiums -- is important because it measures the insurer's discipline in underwriting its policies. The expense ratio -- which measures daily operating expenses divided by premiums -- gauges the efficiency of an insurer and how well it uses its resources to drive top-line growth.

Image source: Getty Images.

But ultimately, the combined ratio is the most critical of these ratios, because it is one of the truest measures of an insurer's profitability.

For example, a company could boast that it has a loss ratio of 60%, meaning it displays immense underwriting discipline and risk mitigation. But if its expense ratio is 45% thanks to lofty sums for underwriting expenses -- things like advertising, agent commissions, and employee salaries -- then its combined ratio would stand at 105%, meaning total expenses outweigh the revenue it collects.

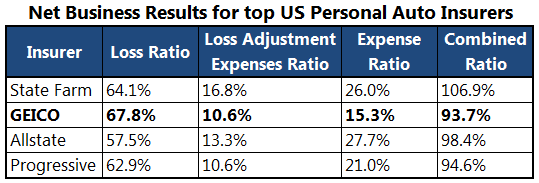

As an example, look at the following comparison between GEICO -- owned by Warren Buffett's Berkshire Hathaway (NYSE: BRK-A)(NYSE: BRK-B) -- against peers Allstate (ALL +2.14%) and Progressive (PGR +3.28%) in the auto insurance business:

Full Year 2013 data. Source: SNL Financial.

As you can see, GEICO had the highest loss ratio in 2013, but thanks to its incredible expense discipline, it had the lowest expense ratio and was thus the most profitable. As a result, GEICO posted an underwriting profit of $1.1 billion in 2013.

By comparison, Allstate wrote just 3% fewer policies than GEICO, yet its underwriting profit of $668 million was 40% lower as a result of its higher expenses.

The takeaway

Keep in mind that while a combined ratio above 100% represents an underwriting loss, it does not mean the company as a whole is unprofitable. This is because there's a difference in timing between when an insurer collects its premiums and when it pays out its claims, and in the interim, it is free to invest the money as it chooses.

However, the combined ratio is essential when it comes to gauging an insurer's discipline in both operating and underwriting, so insurance investors should always keep their eye on this number.