Investors have a love/hate relationship with 3D Systems (DDD 2.28%) stock. There are probably few better recent examples of stocks that have made some investors a lot of money quickly, and lost other investors -- at least on paper -- a great deal of money even more rapidly.

Those who bought at least three years ago are still sitting on hefty gains of about 76% or more, as of March 24, while those who bought about a year ago have watched their investment's value been cut in half.

Data by YCharts.

Let's look at what there is to love and hate about 3D Systems' actual business:

3 things to love -- or at least like -- about 3D Systems:

1. It's one of the co-first movers in the industry

Along with fellow industry leader Stratasys, 3D Systems is a first mover in the 3D printing industry. Oftentimes, but far from always, first movers enjoy a sustainable long-term competitive advantage.

2. Its direct metal printing segment is growing rapidly

Demand for 3D printers that have metal capabilities should grow at a faster rate than the overall 3D printing industry as the technology makes increasing inroads into manufacturing applications. So, it's a positive that 3D Systems entered the direct metal 3D printing market when it acquired Phenix Systems in July 2013.

In 2014, the company's direct metal printer revenue grew 175% on a year-over-year pro forma basis to $39 million. ("Pro forma" means that Phenix Systems' entire 2013 revenue is included for the comparison.) This segment is still tiny -- it accounted for 6% of total revenue in 2014 -- but should be a significant part of 3D Systems' business in the next year or two.

The company has sold out of direct metal printers in every quarter since it acquired Phenix. In the second and third quarters of 2014, 3D Systems was significantly capacity-constrained, resulting in lost revenue. However, it got a second manufacturing line up and running in the fourth quarter, resulting in direct metal printer revenue increasing 178% over the previous year's period.

3. It seems to be building a formidable healthcare segment

3D Systems continues to focus on beefing up its healthcare segment. In 2014, this segment's revenue expanded 80% to $129.3 million, accounting for 19.8% of the company's total revenue. This includes strong organic revenue growth (revenue growth in businesses owned for at least one year) of 46%.

It seems a positive that 3D Systems is building its healthcare 3D printing chops, as personalized medicine is an expanding market. That said, we don't have bottom-line figures such as operating profit for this segment -- and ultimately earnings are what drives a company's stock price.

4 things to hate -- or at least dislike -- about 3D Systems:

1. Its decreasing profitability

Along with Stratasys, 3D Systems ratcheted up its growth game beginning in 2014. It's sacrificing short-term profits for increased spending aimed at capturing market share and fueling long-term growth.

This one is a mixed love/hate bag. We appreciate companies that are investing with an eye toward long-term growth but don't like what that does to current profits.

Data by YCharts.

2. Its extreme diversification achieved through acquisitions

3D Systems has seven distinct 3D printing technologies, whereas Stratasys has three. 3D Systems is also very diversified in terms of materials capabilities and target markets. It's achieved this diversification largely by gobbling up more than 50 mainly smaller businesses in the past approximately four years, with an eye toward becoming the one-stop shop for everything 3D printing-related.

It's a positive that the company doesn't have all its eggs in one tech basket, as relying on a single technology in a rapidly evolving space would result in major trouble if that tech fell out of favor. However, 3D Systems seems to have taken diversification too far.

There are several downsides to attempting to be the industry's jack-of-all-trades. Notably, a business with many moving parts is difficult to manage. The company's growth-by-acquisition strategy further complicates managing the business. It's nearly impossible for any company's top management to focus on nurturing its existing businesses if it's in a constant state of acquiring and incorporating new companies into its fold.

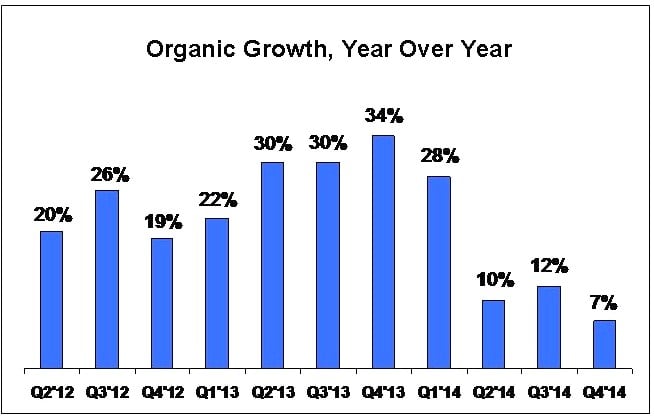

3. Its organic revenue growth faltered in 2014

In 2014, 3D Systems' organic revenue growth (revenue growth in businesses owned for at least one year) slowed considerably. It seems probable that at least some of this slackening was the result of the previously mentioned downside of a supercharged growth-by-acquisition strategy.

Data source: 3D Systems' earnings reports.

3D Systems' fourth-quarter results indicate that it appears to have successfully addressed the two issues that it blamed on its weak organic growth in the second and third quarters: manufacturing constraints for direct metal printers and the delayed availability of its newest Cube desktop 3D printer. However, a new trouble spot bubbled up in the fourth quarter: The North American region's results were tepid, which the company attributed to sluggish 9% year-over-year unit volume growth of its jetting 3D printers.

In the context of a fast-growing industry, 3D Systems' recent organic growth rates are worrisome. Granted, we should expect some growing pains from a company that's scaling up its business, but things need to start to turn around soon if 3D Systems is to remain an industry leader. After all, Stratasys has managed to scale up its business and maintain strong organic growth rates.

Its gross profit margin dropped significantly in 2014

Here's how the gross margin by segment broke out in 2014:

Source: 3D Systems' Q4 earnings presentation.

The company attributed its decreasing gross margin to the introduction of new products, manufacturing expansion, and an unfavorable product sales mix. However, it noted in its Q4 earnings presentation that it expects gross margin to resume expansion this year. We'll have to wait and see if this statement comes to fruition.

Wrap-up

There are a good number of things to both like and dislike about 3D Systems. We should expect some of the growing pains the company has been experiencing. That said, while I'm hopeful for investors, I remain somewhat skeptical about the company's strategy. Attempting to be everything to everyone in any fast-evolving and growing space -- and to accomplish that largely via acquisitions -- is a strategy that's difficult to execute well.