Midstream MLPs such as Enterprise Products Partners (EPD -1.09%), Magellan Midstream Partners (MMP +0.00%), Williams Partners (NYSE: WPZ), and the former Kinder Morgan family of MLPs have long been favorites among investors seeking stable, high, and growing yields. Over the past year, this industry has seen a spate of enormous mergers that will have important repercussions for these pipeline operators' future payout growth prospects.

Let's look at the two most important kinds of midstream MLP mergers: MLPs buying out their general partners, and general partners buying out their MLPs, to see why and how they can help your portfolio.

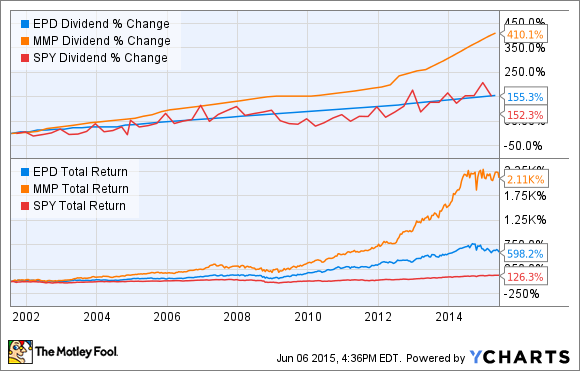

MLP buyout of GP: The original way of cutting costs and boosting payout growth

The midstream MLP industry is very capital intensive, so lowering costs of capital can be a major competitive advantage. Enterprise Products Partners and Magellan Midstream chose to buyout their general partners in 2010 and 2009, respectively; taking advantage of the financial crash to eliminate Incentive Distribution Rights, or IDRs as cheaply as possible.

These fees are designed to incentivize fast distribution growth early in an MLP's life by granting the general partner an increasing percentage of distributable cash flow, or DCF, as the distribution rises, typically up to 50% at the top IDR tier. Of course, once an MLP reaches that tier, the diverting of so much cash flow to the general partner means not only slower distribution growth going forward, but also higher capital costs, which can serve as a hindrance to both profitability and growth.

The elimination of IDR fees have helped Enterprise and Magellan generate impressive long-term payouts and market-beating total returns.

EPD Dividend data by YCharts.

However, there are more benefits to buying out one's general partner than faster payout growth -- it can also mean improved distribution safety and financial flexibility.

For example, because Enterprise doesn't have to send 50% of its DCF back to a general partner, over the last five years, it's been able to retain about $7 billion in DCF, which has allowed it to maintain an extremely safe distribution coverage ratio, or DCR, of greater than 1.4.

Magellan has also benefited from this ability to retain DCF, posting a DCR of 1.45 over the past 12 months. Beyond more sustainable distributions, high levels of retained DCF allow for more consistent payout growth -- Enterprise and Magellan have raised distributions for 43 and 21 consecutive quarters, respectively -- as well as help to lower capital costs even more. That's because retained DCF can be used to fund acquisitions or growth projects without tapping the debt or equity markets.

Kinder Morgan's "de-MLPification" merger

Kinder Morgan Inc's (KMI -1.00%) $77 billion buyout of its three MLPs transformed one of the largest MLP families into a regular c-corporation, but it came with significant benefits that made the deal a major winner for most dividend investors. It also seems to have potentially set a precedent for general partners buying out their MLPs, such as Williams Companies' (WMB +0.74%) recent $13.8 billion buyout of Williams Partners.

There are three main benefits to this kind of "de-MLPification" merger, two of them identical to the previously discussed examples: lower costs of capital and faster dividend growth due to elimination of IDR fees. However, there is a major difference, and it has to do with tax treatments.

The tax benefits of this Kinder Morgan-style merger are twofold. First, because c-corps aren't pass-through entities like MLPS, it means they can retain the high depreciation tax deferments for themselves instead of passing them onto investors. In addition, the acquiring company can reset the value of its newly acquired assets to the value it paid in the merger, which, under accelerated depreciation, can mean billions in tax deferments.

For example, Kinder Morgan and Williams Companies expect to be able to defer an additional $20 billion and $2.1 billion in taxes over the next 14 and 15 years, respectively, as a result of their mergers. This cash, while it will eventually have to be paid to the IRS, can be used to fund growth opportunities in the short term, such as Kinder's $3 billion purchase of Hiland Partners.

All told, the combination of tax deferments and lower capital costs means a boon to dividend growth, with Kinder and Williams projecting 10% and 10%-15% dividend growth through 2020, respectively. More importantly, both companies expect to generate substantial amounts of excess DCF to insulate their dividends during times of industry stress, such as the current oil crash.

Takeaway: MLP mergers can be huge wins for investors

Mergers such as those highlighted here can lead to lower capital costs, greater retained cash flow, and improved future payout growth. Just like with any other merger or acquisition, though. the price a company pays can drastically dictate the value to shareholders. When done well, like the ones made by Kinder Morgan, Williams Companies, Enterprise Products Partners, and Magellan Midstream Partners; they can make a company a very compelling investment.