In 2012 ConocoPhillips (COP +0.94%) initiated a bold plan to transform itself from a second-tier integrated oil company to a top-tier exploration and production company. The first stage of that shift involved spinning off its refining, logistics, and chemical segments to facilitate becoming a pure-play exploration and production company. The final stage of that big shift would be driven by plans to grow its production and margins by 3% to 5% per year for the next five years. It was a sound plan, but one predicated on relatively high oil prices for the near-to-medium term. Now that oil prices are no longer in the triple digits, the company is shifting gears yet again.

A few subtle changes

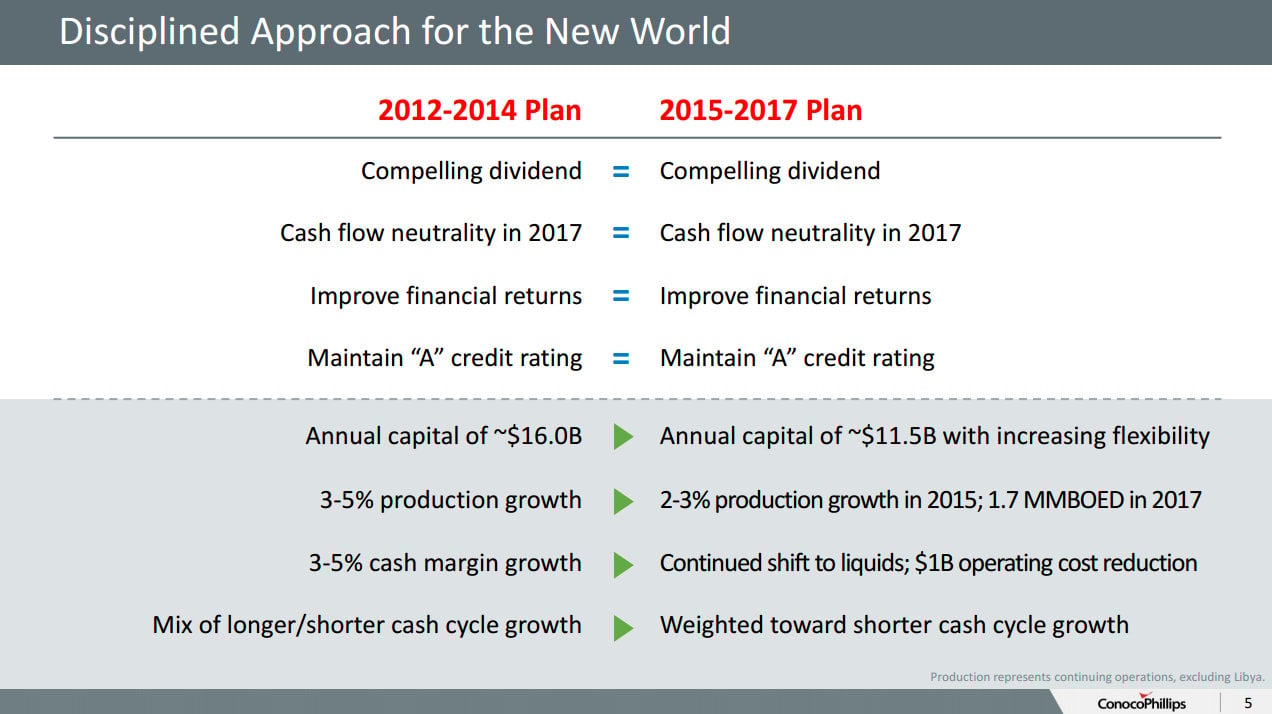

Much of ConocoPhillips' initial plan is staying the same. The company is still planning to pay a compelling dividend, which management has affirmed remains a top priority. Furthermore, the company still plans to be cash flow neutral by 2017 while improving its financial returns and maintaining an A-rated balance sheet. The shift comes in the operational side of the plan, as the reduced price of oil is forcing the company to cut spending and growth so it can still deliver on the core of its plan. This shift is detailed on the slide below.

Source: ConocoPhillips Investor Presentation.

As that slide notes, the biggest shift is coming in capital spending, as ConocoPhillips is cutting spending from $16 billion per year to just $11.5 billion with flexibility to cut it further if necessary. This spending cut will result in slower growth, as its production growth rate will slip from a projected 3%-5% annually to 2%-3%. That said, it's a shift that's really being made possible by its ability to invest in the shorter cash cycle growth found in shale plays.

Why shale is making this shift possible

Shale plays in the U.S. have quickly gone from high-cost sources of oil and gas to low-cost supplies due to the rapid decline in the costs of drilling shale wells along with an improvement in well performance. As a result, shale is not only among the lowest-cost sources of energy for ConocoPhillips, but -- as the slide below shows -- it's an abundant and flexible source of high-return growth.

Source: ConocoPhillips Investor Presentation.

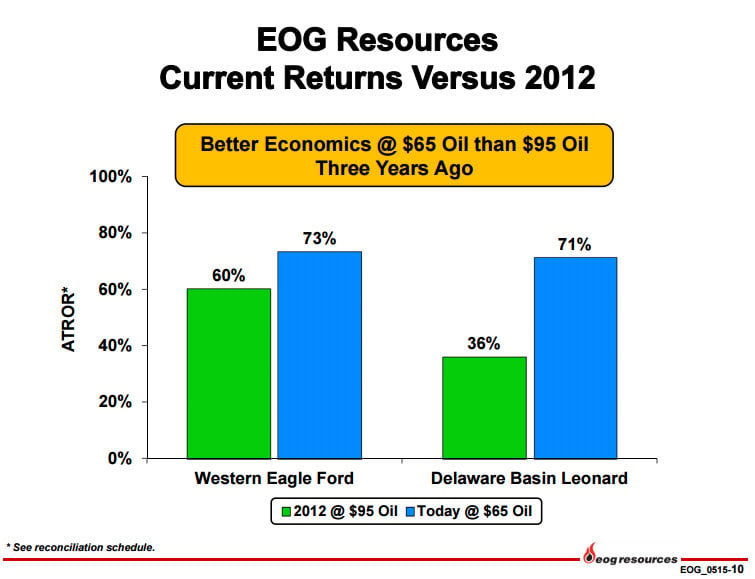

The shift in the cost structure of shale has been truly remarkable over the past year. While overall shale production in the U.S. is certainly affected by the steep decline in oil prices, the profitability of shale oil has improved. In fact, well economics in several key shale plays, including the Eagle Ford and Permian Basin, are actually better now at $65 oil than they were when oil was $95 a barrel. This is evident from the following slide from an EOG Resources (EOG +0.42%) investor presentation.

Source: EOG Resources Investor Presentation.

As that slide points out, EOG Resources is seeing returns in the Western Eagle Ford shale of 73% at $65 oil, which is an improvement from the 60% returns it was earning when oil was $95. However, even more compelling are the returns it's seeing in the Permian Basin's Delaware Basin Leonard, as returns zoomed from 36% at $95 oil to 71% at $65 oil.

In fact, the improvement in well returns in the Permian Basin even at lower oil prices is expected to bode well for ConocoPhillips' future. It has a huge position in the region, with an estimated 1 billion barrels of oil equivalent, or BOE, resource potential. That's a massive resource, though at the moment it is a smaller position than EOG Resources' at an estimated 1.4 billion BOE resource potential.

However, ConocoPhillips has been much slower than peers like EOG Resources in developing the play as the initial returns weren't on par with those of the Bakken or the Eagle Ford. That said, with costs coming down and returns improving, this is now a play that's expected to drive growth for the company going forward. In fact, the company's new plan will see it double its rig count from two rigs this year to four by 2017, which will push production up from its current rate of less than 10,000 barrels of oil equivalent per day, or BOE/d, to nearly 25,000 BOE/d by 2017, with upside should returns continue to improve.

Investor takeaway

ConocoPhillips is shifting toward shale in a big way. It's a move made possible by the rapid decline in well costs, which is significantly improving well returns. That combination is now opening up a new growth driver for the company, as the Permian Basin is expected to go from a subpar play to a real growth driver for the company, much as it has been for rival EOG Resources.