Source: Facebook.

Facebook (FB -0.06%) stock is doing really well lately. Shares of the social network founded by Mark Zuckerberg are up by nearly 35% year to date. Adding more more fuel to the bullish fire, the company reported pretty solid financial results for the third quarter of 2015 on Wednesday.

Key numbers

Total revenue came in at $4.5 billion, a big 41% increase from $3.2 billion in the third quarter last year. Advertising revenue grew 45% to $4.3 billion, while payments and other fees declined 18%. Excluding the negative impact from foreign currency fluctuations, advertising revenue grew 57% and total revenue jumped by 51%.

Mobile advertising revenue represented 78% of advertising revenue during the quarter, up from 66% of advertising revenue coming from mobile in the third quarter of 2014, and proving that Facebook keeps thriving in the important mobile segment.

The company is aggressively investing for growth, so expenses outgrew revenue and pressured profit margins down during the quarter. Facebook reported a 68% increase in total expenses, reaching $3.04 billion. Operating margin declined from 44% of revenue in the third quarter of 2014 to 32% of sales last quarter.

Since the big revenue increase was for the most part diluted by declining profit margins, GAAP net income per share grew only 3% during the quarter, coming in at $0.31.

Facebook also reports adjusted financial figures, meaning accounting numbers that exclude items such as amortization of intangibles and share-based compensation expense, among others. When looking at adjusted numbers, the increase in earnings per share was a much stronger 33%, from $0.43 to $0.57 per unit.

Facebook keeps gaining more friends

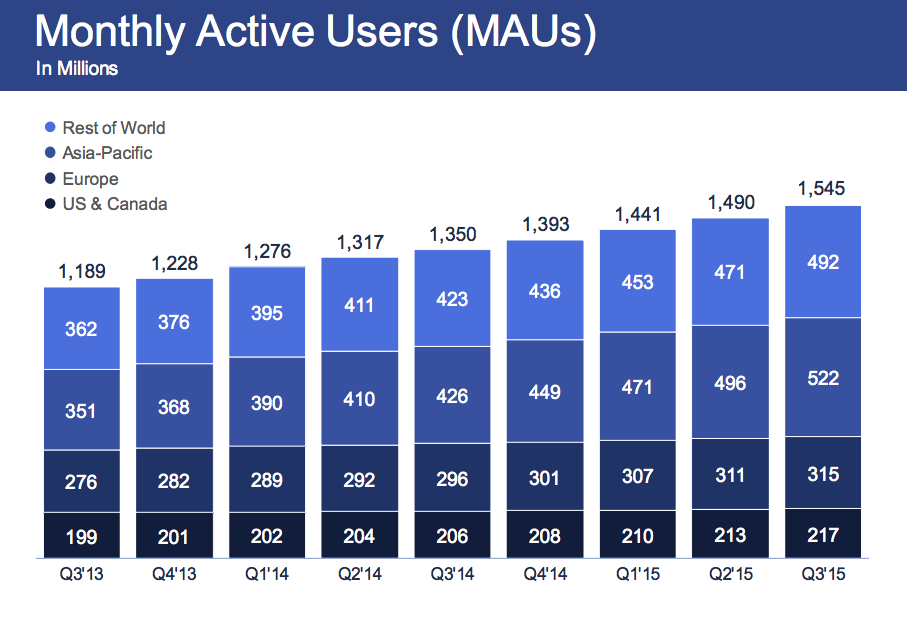

Facebook had 1.55 billion average monthly active users as of September, a healthy 14% year-over-year increase. The platform is considerably bigger than rivals such as Twitter (TWTR +0.00%) and LinkedIn (LNKD +0.00%), yet it keeps gaining more users at an amazing speed.

To put the numbers in perspective, Twitter ended the third quarter of 2015 with only 308 million average monthly users when excluding SMS Fast Followers, an 8% year-over-year increase, and it gained only 3 million users versus the second quarter of 2015. Not surprisingly, Twitter investors are feeling disappointed with this performance, and Twitter stock is down nearly 45% from its highs of the last year.

LinkedIn is a very different story. Since the company is mostly focused on business contacts and job opportunities, it theoretically has a smaller potential market than Facebook or Twitter. But the platform is still growing rapidly. LinkedIn reported 396 million cumulative members as of the end of the third quarter, a 20% annual increase.

Importantly, Facebook is growing its daily user base at a faster rate than monthly users, so engagement is moving in the right direction. Daily active users were 1.01 billion in September, a 17% year-over-year increase. Nearly 65% of Facebook users engage with the platform on a daily basis.

The company is also gaining ground on mobile devices. Facebook had 1.39 billion mobile monthly users as of September, a 23% annual increase. Mobile daily users jumped by a vigorous 27% year over year, to 894 million.

Average revenue per user is also improving. The company made $2.97 per user last quarter, versus $2.40 in the same period last year. Facebook is making $10.49 per user in the U.S and Canada, versus $3.47 in Europe, $1.39 per user in Asia-Pacific, and $0.94 in the rest of the world. This wide gap in monetization levels across different regions indicates that Facebook still has plenty of room to increase monetization on a global scale.

To sum up, Facebook is delivering solid user growth and strong engagement, and the company is also increasing its ability to make money from its user base. This approach is resulting in impressive revenue growth. Even if increasing expenses are hurting profit margins, investors in Facebook have solid reasons to give a thumbs-up to the company's latest earnings report.