Eaton Corp. (NYSE: ETN) posted generally disappointing earnings in the third quarter, though they were in line with a last-minute revision to guidance. The thing is, the news doesn't get much better. Here are five key takeaways from the quarterly earnings call.

It wasn't pretty

According to CEO Sandy Cutler, "Our sales were down 9%, with 6 points of those 9 points due to forex; the other 3, organic revenue decline." That was worse than the company expected at the midpoint of the year. It's bad that the company's top line is falling, but it's really bad that results are falling short of management's expectations.

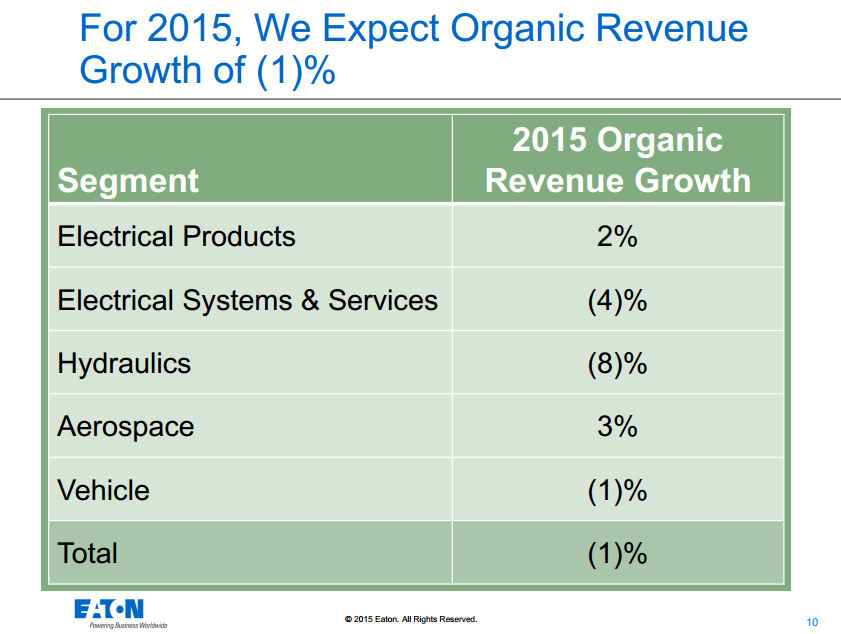

Eaton's new sales outlook. Source: Eaton Corp.

And the change has been dramatic. Eaton started the year off expecting organic sales growth of between 3% and 4%. It has steadily dropped that number and now expects organic revenues to fall 1% for the full year. So the quarter's top line is symptomatic of a worsening market. Further, Cutler explained that "our weaker bookings have really caused us to drop our second-half guidance."

Eaton, however, isn't alone. For example, competitor ABB (NYSE: ABB) saw its top line decline 13% year over year. (Revenues were down 2% if you take out the impact of currency changes.) In fact, the lead bullet point in the company's earnings release was this: "Order pattern reflects adverse market conditions." So Eaton is hardly a standout in its struggles, with ABB highlighting oil and gas and China as two notable ongoing concerns.

We're doing what we can

With a weak top line, it's hard to expect much from the bottom line, and indeed, Eaton's earnings missed analyst expectations and were about 25% below the year-ago period. But it could have been worse. According to the CEO.

We're particularly pleased with the great cost control and all the restructuring work that's going on across the company. And that allowed us to offset the lower volumes that we had outlined in our earnings revision just a week and a half ago, as well as more negative FX.

In other words, the actions the company has been taking to right-size its business in the face of difficult end markets has been working. It's good to know things are going well operationally, but it's equally nice to see that the company is being proactive.

But wait: There's more.

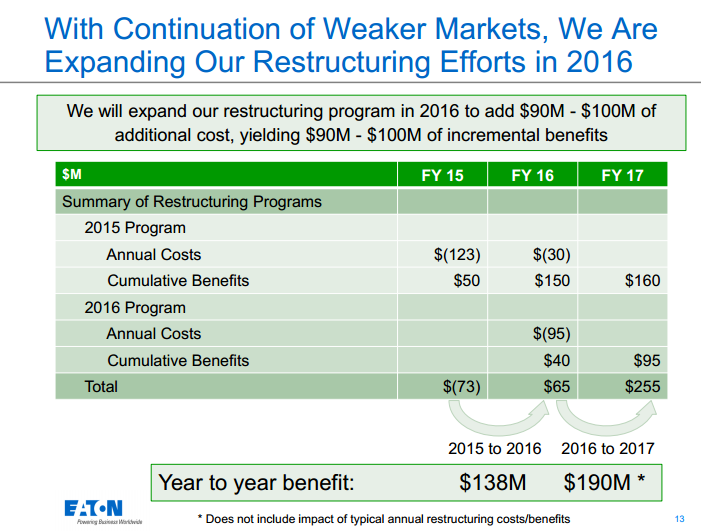

In fact, Eaton's not done yet. The CEO's update on the restructuring program that was announced earlier in the year was that it "is indeed going to produce even more savings than we had shared with you." But the company has upped the ante as we enter the last stanza of the year, announcing a second phase that will start in 2016 to trim an additional $90 million to $100 million in ongoing costs.

Eaton's next restructuring effort. Source: Eaton Corp.

When asked about the delay to 2016 on the second program, Cutler explained:

Part of this is the issue of just how much capacity there is to do how much all at one time. ... [The] company has been really busy during the third and fourth quarter getting this first group done. And we'll kick off with the second group, as I said, most likely right in the first quarter.

This is really about Eaton's doing what's best for the company instead of what's best for next quarter's earnings, which should make long-term shareholders happy.

The weak spots are still weak

Although the company saw sales weaken across the board, there were two standouts that have remained trouble spots. The first was the hydraulics business, where the CEO noted, "I don't think [there's] much new news here from what we've been chatting with you all about here, as these markets continue to be weak, commodity markets across the board around the world are weak." China is a big story here, particularly the construction side of things, just like at ABB.

The second notable ongoing issue was the oil and gas business, which lives within Eaton's electrical systems and services segment. According to Cutler, "Recall when we gave our guidance for this year and indicated that about 6% of Eaton's revenues are in oil and gas, and that we expected that [market] would be off about 25%, we'd also said that we thought the primary impact of that would be in the second half of 2015, and that is indeed what we're experiencing." This is in line with ABB's experience, too.

So while a generally softening business environment is bad, these two areas are particularly troublesome and are worth watching. Yes, Eaton is working on turning things around, but it can only do so much. Hydraulics and oil and gas are likely to remain trouble spots into next year.

But we've got cash!

All these negatives aside, Cutler was pleased to announce "a quarterly record operating cash flow," which he explained was "a reflection of the work we're doing in terms of not only improving profitability but also really pulling dollars out of our working capital." So despite the weakening market, Eaton is still generating plenty of cash.

The second piece here, though, is what Eaton is doing with that cash. It made one small acquisition in the quarter, buying an LED lighting company that specializes on the stadium and large-venue markets. But the cash also "allowed us during the quarter to buy back about $284 million of shares," the CEO said, adding: "That brings our year-to-date repurchases to $454 million. That's about 1.5% of our outstanding shares." Since the company thinks its shares are underpriced, look for more buybacks next year.

It was a tough quarter. But Eaton, which has been in business for over 100 years, has seen economic slowdowns before. It's doing what needs to be done. Moreover, it's acting like an investor and buying Eaton shares at what it believes is a cheap level. Despite the negative news, it might be a good idea to consider following that lead.