Photo credit: Johathan C. Wheeler via Flickr.

The oil market can be quite baffling. Take for example, its response to the recent OPEC meeting where its members agreed to press on with its policy to maintain its share of the oil market instead of maintaining a certain price for oil. It was a largely expected decision, with leading voice Saudi Arabia saying that the group would only cut output if non-members joined in. It was an effort that large oil producing non-member nations such as Russia, Mexico, and Norway were loathe to do, making it a non-starter. And yet, despite the well telegraphed outcome that OPEC wasn't budging on its policy, oil prices went into another freefall after the news broke, recently touching seven-year lows.

The market's reaction begs the question of how it did not foresee this outcome when it was plain as day beforehand. OPEC was clear it wasn't budging, as were its unwilling partners. So, one would assume this would be priced in, but apparently it was not. Unfortunately, this isn't the only time the oil market failed to assume the very likelihood of not just the expected happening, but the unexpected as well.

What goes up keeps going up, right?

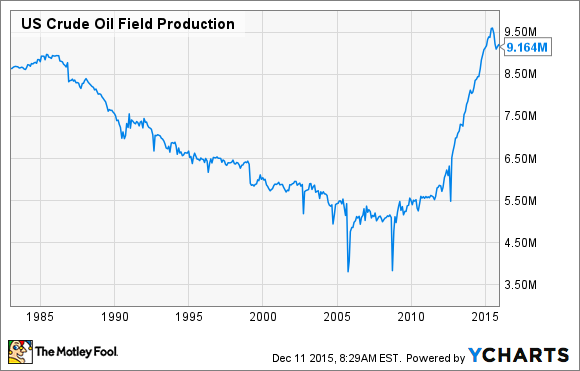

After a steady slump for decades, American oil production finally started to turn a corner right around the time of the financial crisis. Actually, turning the corner is putting it lightly, it was more like a sharp turn followed by a rocket blast:

US Crude Oil Field Production data by YCharts

This turn was fueled by three things: Triple digit oil prices, a new drilling technique, and a whole lot of debt. The net result was that in a matter of just five short years U.S. oil production effectively doubled, turning America into the world's largest oil producer. It was a turn that did not go unnoticed. OPEC saw it as a treat and because it controlled one of the fuels to this growing rival it acted to shut off one of its key fuels: $100 oil.

It was a move that no one saw coming. Every analyst believed that OPEC would fight to defend the price of oil because the budgets of member nations were built upon that oil price. Oil companies, likewise, believed that OPEC would simply cut its production to maintain price, which could enable U.S. producers to keep pumping.

A model based on a flawed assumption

Therein lies the real underlying issue. The oil market built its assumptions based on a foundation that was as firm as the desert sand. Worse yet, this assumption blinded the market to the remote possibility that things could change.

One of the clearest examples of the blindness that oil companies had to the possibility that a change was just over the horizon was found in a statement made by struggling Canadian oil producer Penn West Petroleum (NYSE: PWE). In July 2014 Penn West Petroleum wrote in an update to investors:

As of July 1, 2014, we are now participating fully in the currently strong crude oil price environment with the last of our WTI hedge positions expiring on June 30, 2014. This allows us to immediately realize 100% of current market pricing which currently exceeds our 2014 budget assumption by approximately $10 per barrel.

In other words, because oil prices were so lucrative at that moment Penn West had chosen to throw caution in the wind and allow its oil hedges to wind down enabling it to capture the higher market price for oil. However, in leaving itself open to the upside, it was now totally exposed to the downside in oil prices. Needless to say, it never saw this coming:

WTI Crude Oil Spot Price data by YCharts

Crude started its slide almost to the very day that Penn West allowed its oil hedges to roll off. Within six months the company had to dramatically shift gears, leading to a dividend reduction because, as CEO Dave Roberts put it,"Penn West's business model assumes a conservative long run-term commodity price, however, the recent downturn falls outside our lowest probabilistic expectations." In other words, we didn't see this coming, not even in our worst nightmares.

Penn West, of course, wasn't alone in not seeing the downturn coming. Permian Basin driller Pioneer Natural Resources (PXD +0.00%) was building a 10-year plan to develop its gigantic resources base. It was building its plan based on two scenarios:

Source: Pioneer Natural Resources Investor Presentation.

The conservative scenario would see oil decline from $100 to $81 by 2019 while the aggressive scenario was based on a $95 oil price holding steady for a decade. Either way, its production was heading higher because it had the fuel -- in this case high oil prices and a huge resources base -- to continue growing. Suffice it to say, today's sub-$40 oil price falls below Pioneer Natural Resources "lowest probabilistic expectations." It has forced the company to shift gears, planning for much less robust growth for the time being.

Investor takeaway

The oil market is really just based on assumptions, which get put into models that spit out probabilities. Unfortunately, analysts, investors, and oil company executives buy too heavily into these outcomes, thinking that the future is predictable. It's not. Because of this there is a very good likelihood that these models will be wrong because of something no one saw coming, even if it is clear as day before hand.

The lesson for investors is to not take these models too seriously. The best way to do this is to diversify risk and to not over-allocate a lot of one's portfolio to any one company, even one where the future looks predictable. Because more often than not something no one saw coming will throw a wrench into the key assumption driving that supposed predictability, leading to a very bad outcome.