Alliance Resource Partners (NASDAQ: ARLP) had long managed to buck the broader trends in the coal industry. But the limited partnership's units started to fall late last year as investors began to see that Alliance could only outrun falling coal prices for so long. Although it seems odd to say, a couple of unitholder-friendly moves might have turned out to be the worst thing that Alliance could have done for investors this year.

The coal downturn

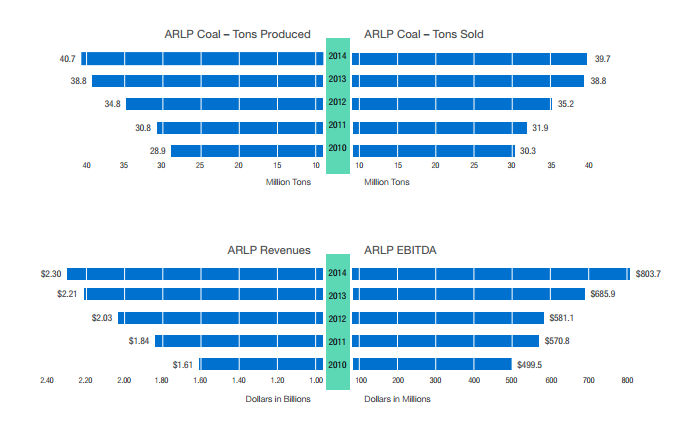

The coal industry has been in decline for several years because of coal's dirty image and cheap natural gas. The only thing is that not all coal regions have been hard hit. For example, Illinois Basin coal demand has increased in recent years because of the nature of this region's coal. That's been great for Alliance because that's where most of its mines are located. So, this coal miner has been able to increase volumes at a time when other miners have been cutting back.

As a comparison, Cloud Peak Energy (NYSE: CLD), which operates in the prolific Powder River Basin, has been selling less and less coal. Shipments were roughly 95 million tons in 2011, but have fallen each year since and may be as little as 75 million tons in 2015.

Cloud Peak coal shipment figures. Image source: Cloud Peak Energy

Alliance, meanwhile, produced a bit over 30 million tons in 2011 and is expecting to produce more than 40 million tons in 2015. It's on pace to sell almost all of what it mines.

Too much of a good thing

So while competitors like Peabody Energy have resorted to cutting dividends and others have fallen into bankruptcy, it shouldn't be surprising that Alliance has been upping its distribution every quarter through the coal downturn (until the third quarter, when it held the distribution steady).

This is really just the recognition of reality. The problem here is that the two increases made earlier in 2015, at a time when the market was already sending the units sharply lower, were likely seen as a statement of strength that hasn't proven out. Sure, it makes sense that the board wanted to keep a trend that's been going since mid-2008 intact. But with the shares heading lower, it might have been more prudent to hit the pause button at the start of the year.

Basically the miner could have said that there's a big problem in the coal industry, it sees it, and use the "extra" cash to pay down debt—a shareholder and partnership friendly move. Further, it could have explained that the distribution would be looked at quarterly, but annual hikes would likely become the norm until the coal market stabilized.

Alliance Resource Partners production and sales figures. Image source: Alliance Resource Partners.

Setting the mood

Essentially, by keeping the quarterly distribution increases going, Alliance was setting expectations higher than was appropriate in a still-struggling industry. With so many other companies cutting distributions or going under, few would have blinked at one of the best run miners taking a well-articulated wait-and-see approach. And it would have set investors up for what has turned out to be a turning point for Alliance, with CEO Joseph Craft basically explaining during the third-quarter conference call that the partnership is now looking at cutting production.

Producing less coal means lower revenue and likely less money available for distributions. Which helps explain why it chose to not increase the disbursement in the third quarter. To be fair, distribution coverage was a robust 1.66 times in the quarter, leaving plenty of room to protect the current payout. But the two earlier distribution hikes in 2015 set a tone that the current decision to hold the line has, basically, blown up. For anyone following the distributions, the distribution decision and the potential for production cuts is a double whammy that paints a very negative picture.

Distributions send signals and companies need to be careful about the story their actions tell. Alliance was trying to do the right thing by unitholders, but, in the end, may have set them up for a more severe disappointment than needed. Imagine the different impact that holding off on a small distribution hike until the final quarter of the year might have had ... basically, it would have sent a completely different message.