Alcoa (AA +0.00%) is a company in transition. And 2015, despite many positives, shows why the company's legacy "Upstream Business" was its worst performing business segment. Which may also help explain why the company has chosen to break itself in two.

A new dawn

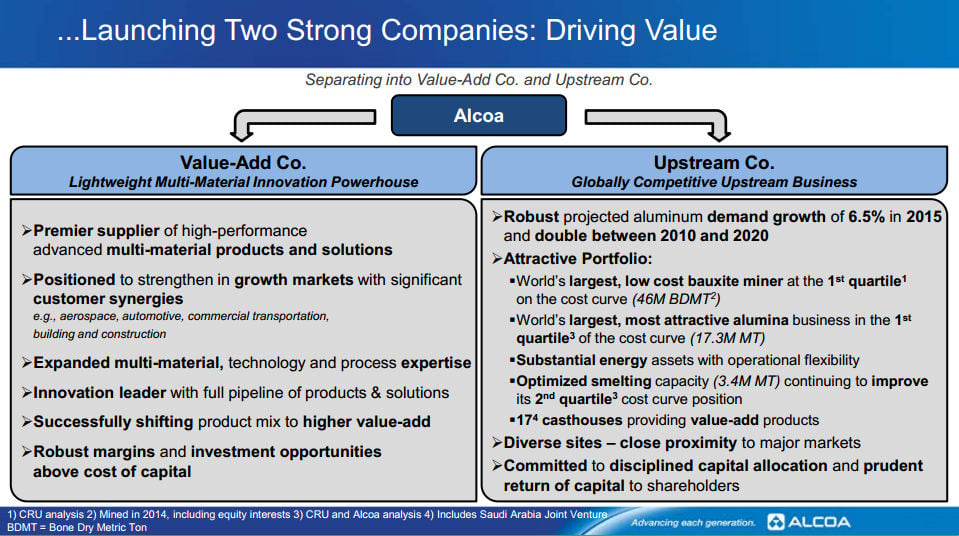

For many years Alcoa has been focusing on building up what it's calling its "Value Add" business. This segment of the company makes things out of aluminum, such as soda cans and airplane parts. These products often command high premiums and are seeing robust demand. The rest of the business, known as the Upstream Business, operates in the commodity aluminum market and has been shrinking.

Alcoa's break up plan. Source: Alcoa.

While some might like the idea of vertical integration, with the Value Add segment using what Upstream makes, Alcoa has decided that these two businesses can operate more efficiently on their own. It the second half of 2015, it announced that it was going to break itself in two.

But that just highlights the dichotomy between the two businesses. While Value Add has been growing, Upstream has been shrinking. Essentially, the giant aluminum company has been refocusing around making things out of aluminum and shifting away from the commodity-driven aluminum market.

The right move

To be fair, trimming down the Upstream business is the right move. And that continued in 2015, with the company closing two smelters, trimming U.S. production, and shuttering a power plant. But that's just continuing the long-term trend for this division, which has seen its capacity decline by about a third since 2007.

Of course, all of this has a purpose. Alcoa has been able to reduce its costs materially, thus improving the industry positioning of the Upstream Business. And the company is quick to point out that the aluminum industry is still quite strong, at least relative to other commodity markets, with demand for aluminum expected to increase in the years ahead as it displaces older, heavier materials and its use expands with organic growth in existing core markets, like aerospace. But it's hard to deny the trend at Alcoa today, Upstream is getting smaller.

Which is why this business segment was the worst performer in 2015. Indeed, industry headwinds continued to warrant right sizing the Upstream Business in 2015. Which helps explain why Alcoa is looking to break off Upstream as a separate entity, so investors can value the Value Add business as a stand-alone entity without the weight of the legacy aluminum business holding it down.

Getting smaller isn't unique to Alcoa, though. For example, United States Steel (X +0.00%) has been shrinking its business in an effort to better compete with companies utilizing newer technology and, at the same time, dealing with a global pricing slump. The same is true in the mining business, where companies like BHP Billiton (BHP -0.81%) have been trimming costs. And like Alcoa is planning, BHP split up its business to jettison operations that it felt didn't fit with its long-term future. So what Alcoa is doing with Upstream really isn't unique at all in a business environment that's been tough on all commodity players.

China is importing less aluminum. Source: Alcoa

A work in progress

All of that said, it would be a mistake to count the Upstream Business out. It is a large and important industry player. And while the aluminum market has been affected by many of the same trends as other commodities, notably decreasing demand from China, aluminum does appear to have a bright future.

For example, the aerospace sector has long been a stronghold since weight is a big issue in flying. As that sector expands with global prosperity, so, too, will demand. But weight is also an increasingly important factor for automakers, so expect auto sector demand increase, as well. True, both of these trends will likely benefit the Value Add division more, but Value Add and similar companies need to get their aluminum from somewhere. And Alcoa's Upstream Business is doing what it needs to do to ensure it will be there to supply it profitably.

Perhaps its best to consider the Upstream shakeup a little bit of tough love, as Alcoa prepares for the future of aluminum. While that marks it as Alcoa's worst performing business in 2015 in my book, it's not a fact I would hold against Upstream as it prepares to fly solo.