Source: CorEnergy Infrastructure Trust.

The recent oil crash has decimated nearly all energy related stocks. With no end in sight to cheap crude, determining which high-yield energy stocks represent long-term deep value opportunities and which are value traps can be a challenge.

Let's take a look at what could be a uniquely undervalued long-term income opportunity in the world of real estate investment trusts or REITs: CorEnergy Infrastructure Trust (NYSE: CORR), to see if its high double digit yield deserves a spot in your diversified dividend portfolio and know about both the risks and potential rewards it could offer you in 2016 and beyond.

An intriguing business model

CorEnergy's REIT structure requires it to payout 90% of its taxable income as dividends which, combined with the market's hatred of all things oil and gas related, explains the sky-high yield of 17.9%.

Despite a yield that would normally serve as a red flag for investors that a dividend cut was imminent,though, the REIT's business is actually doing very well.

Source: CorEnergy Infrastructure Trust.

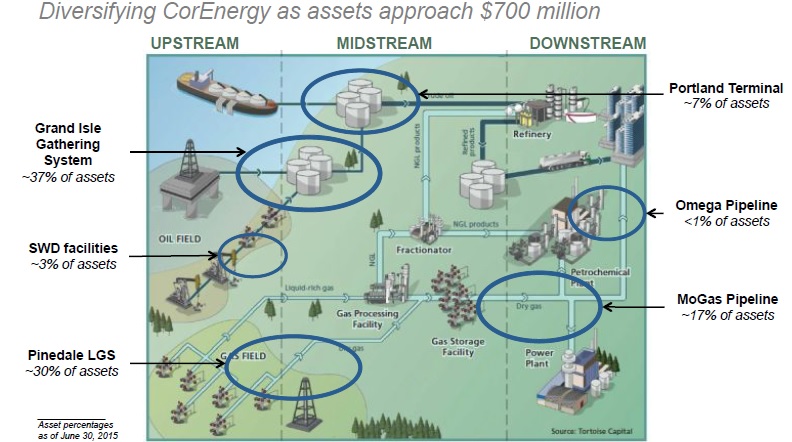

That's because CorEnergy's business model is essentially that of a midstream MLP, but better. They buy midstream infrastructure from oil and gas companies, such as its two biggest customers Ultra Petroleum (NYSE: UPL), and Energy XXI (NASDAQ: EXXI), that are essential to extracting gas and oil and bringing it to market.

CorEnergy then leases back the use of these assets under a triple net lease -- meaning the lessee pays taxes, insurance and maintenance costs -- and receives a highly predictable stream of cash in the form of monthly rent with which to pay and grow the dividend.

Better yet, because its leases are treated as operating expenses, the customers paymenr to CorEnergy comes before repayment to both shareholders and even bondholders of its customers in the event that they become distressed by low energy prices.

That's important, because both Ultra Petroleum and Energy XXI are suffering mightily because of high debt loads and oil and gas prices at multi-year lows. However, in my opinion, this offers brave, long-term investors -- with a high risk tolerance -- an incredible opportunity.

Even in the event that Ultra Petroleum and Energy XXI go bankrupt, whomever ends up owning their acreages will need to rent CorEnergy's midstream assets to continue producing and generating cash flows from the oil and gas sales.

Payout profile shows CorEnergy is undervalued

| Yield | TTM Adjusted Funds From Operations/Share Payout Ratio | Long-Term Management Payout Forecast | |

|---|---|---|---|

| CorEnergy Infrastructure Trust | 17.9% | 86% | 3%-5% |

Sources: Yahoo! Finance, earnings presentations, 10-Qs, 10-Ks, management guidance.

With a yield this high CorEnergy is trading as if a dividend cut were certain. Yet when you examine the dividend profile, it suggests that the current dividend sustainable. But before you go running out to load up on shares of CorEnergy, be aware that this is a risky investment, and the dividend is far from guaranteed.

Risks to be aware of

There are two main reasons Wall Street is willing to offer shares of CorEnergy for so little.

First, CorEnergy's growth strategy requires it to borrow cheap debt and sell equity to buy new midstream assets. While its $219 million in total debt means it's not particularly over-leveraged -- its debt-to-equity ratio of 0.52 is far lower than the REIT average of 1.84 -- because of its ties to the oil and gas sector the REIT may not be able to continue borrowing at its current low average interest rates.Until oil prices rebound, lack of cheap debt and equity growth capital will limit its ability to grow its asset base.

CorEnergy is a very small REIT, and that means its cash flows are concentrated with just a few assets leased to a small number of energy companies. Specifically, 91% of its assets are leased to its five largest customers.This situation exposes its adjusted fund from operations (AFFO) to large potential declines should one or more of those customers, especially Ultra Petroleum or Energy XXI, stop paying rent.

Management is confident that because of the low overall percentage of these companies' operating costs these rents represent, combined with the fact that without its assets they can't produce any oil and gas, that even in the event of bankruptcy its existing contracts will be honored.Should management's opinion prove overly optimistic in the event of a customer's bankruptcy, then its dividend may indeed have to be cut.

However, given that CorEnergy is offering a yield over 20%, even in the event of a worst case scenario where a couple of its customers can't pay and the dividend is cut, I believe CorEnergy would still make a good long-term investment.

Bottom line:

CorEnergy's dividend is by no means guaranteed to survive the oil crash. I fully admit that given the current energy market, this energy REIT is high-risk. However, given its strong portfolio of long-term leases and valuable assets that continue generating sufficient cash flow to cover the dividend and then some, I believe that Wall Street is mispricing the risk of a payout cut.

In that mispricing of risk lies the potential for excellent long-term income once oil prices finally recover and the yield normalizes to more rational levels.