It's no secret that the industrial sector is facing a difficult 2016, and historically investors have favored stocks such as Danaher Corporation (DHR +1.48%) for their "safe haven" qualities. The company's exposure to healthcare, environmental, and dental technologies gives it defensive qualities. Moreover, 60% of its revenue comes from recurring (often high-margin consumables) sales. That said, its recent fourth-quarter results saw core revenue come in flat, when management had expected 2% growth. Which of course begs the question: Is Danaher still a safe haven?

What went wrong?

Despite core revenue growth that fell short, Danaher met analyst estimates for $1.27 in adjusted diluted EPS, and first-quarter guidance of $1.00 to $1.04 straddles analyst estimates of $1.03.

However, Danaher's full-year 2016 guidance of core revenue growth of 2% to 3% deserves closer inspection. The core revenue shortfall in the fourth quarter of 2015 and CEO Thomas Joyce's admission of a weakening macro environment "particularly in our industrially oriented markets" raises question marks about Danaher's full-year target.

Indeed, Barclays analyst Scott Davis asked a related question on it. Joyce responded by highlighting the growth opportunities in its less cyclical businesses and outlined his assumption that "some of the slowing in December is essentially the environment that we're going to see in the near term here."

That said, it's a useful idea to look at segmental performance to see just where trends are likely to take Danaher in 2016.

Segmental trends

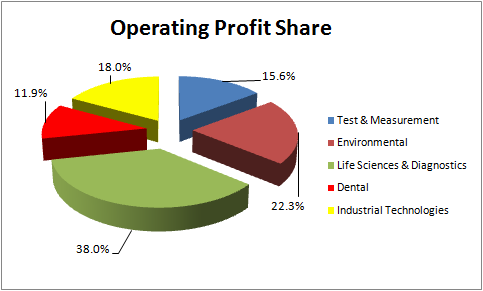

You can think of the test and measurement and industrial technologies segments as being the most cyclical, while life sciences and diagnostics, environmental, and dental are relatively less so. A breakout of Danaher's fourth-quarter operating profit share reveals that only a third of its earnings come from the former -- within which around 20%-30% of revenue is from consumables.

SOURCE: DANAHER CORPORATION PRESENTATIONS.

It's useful to separate core from reported results because Danaher is an acquisitive company. In other words, the reported numbers are somewhat distorting. Indeed, the acquisition of Pall Corp. clearly flatters life sciences and diagnostics reported growth, while dental benefited from the acquisition of Nobel Biocare.

| Segment |

Reported Revenue Growth |

Core Revenue Growth |

Reported Margin Growth (bp) |

Core Margin Growth (bp) |

Operating Profit Growth |

|---|---|---|---|---|---|

|

Test and Measurement |

(9%) |

(5%) |

340 |

110 |

6.8% |

|

Environmental |

1% |

4% |

260 |

60 |

14.9% |

|

Life Sciences and Diagnostics |

34.5% |

2% |

(270) |

75 |

12.5% |

|

Dental |

17% |

0.5% |

630 |

515 |

94.3% |

|

Industrial Technologies |

(8.5%) |

(4.5%) |

120 |

80 |

(3.4%) |

|

Total |

12.5% |

Flat |

Flat |

120 |

12.9% |

SOURCE: DANAHER CORPORATION PRESENTATIONS.

A few positive takeaways from the table:

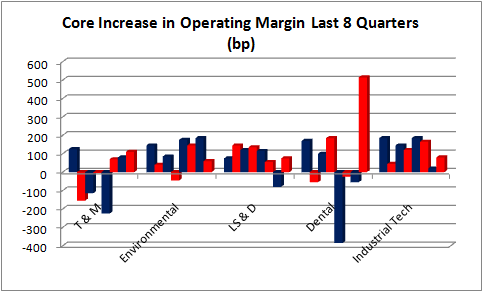

- Each segment increased core margin.

- Despite falling revenue growth (core and reported), test and measurement and industrial technologies both increased margin growth.

- Life sciences and diagnostics returned to core margin growth after a decline in the previous quarter.

- The Nobel Biocare acquisition seems to be turning around lackluster performance in Danaher's dental segment.

And now the negative:

- There was weakness in industrial technologies and test and measurement revenues.

- Core revenue growth at dental remains disappointing.

- Life sciences and diagnostics core revenue growth slowed to just 2% in the quarter.

Commentary

It's no surprise to see industrial technologies and test and measurement give weak results, and it's fair to apportion a large part of the performance to the economy -- not a lot Danaher can do about that. Moreover, the improvements in core operating margin across the board are a testament to management's ability.

DATA SOURCE: DANAHER CORPORATION PRESENTATIONS.

However, dental's sluggish core growth is a concern, though Joyce signaled that its dental technology products -- hit by customer destocking all through 2015 -- had turned a corner: "In dental technology, we saw our first quarter of positive growth since the fourth quarter of 2014. Top line results continued to be affected by destocking within our U.S. distribution channels but to a much lesser degree than in previous quarters."

Turning to life science and diagnostics, core revenue growth of just 2% -- a worrying sign, as it indicates that Danaher's revenues may not be as immune as many think.

Sanford Bernstein analyst Steve Winoker asked about growth rates, and CFO Daniel Comas responded by pointing out that diagnostics was the larger side (mainly consumables) and growth had been negatively affected by fewer selling days in the quarter.

"So, actually on a days-adjusted basis, diagnostics tracked pretty close to that 3% to 4% rate all year, including the fourth quarter," he concluded.

Looking ahead

All told, it was a good quarter of execution, and Danaher appears to be getting its dental segment back on track for growth, while life sciences and diagnostics and environmental remain strong.

Clearly, the concern lies with revenue from its industrially exposed segments. Moreover, Danaher maintained its expectations for 2% to 3% core revenue growth in 2016, despite flat core revenue growth in the fourth quarter--putting pressure on the company to deliver. On balance, Danaher still deserves the benefit of the doubt and its safe-haven status, but after these results it's bit more dependent on management's ability to execute.