Apollo Investment Corporation (AINV +0.52%) can't seem to catch a break. The company reported yet another quarter of losses from its energy-heavy investment book, despite its efforts to use fee waivers to stay friendly with its shareholders.

Apollo Investments' quarter by the numbers

The investment company reported falling operating income against the year-ago period and a slightly smaller net loss than the year-ago period.

|

Metric Per Share |

Calendar 4Q 2015 |

Calendar 4Q 2014 |

|---|---|---|

|

Net Investment Income (Operating Income) |

$0.21 |

$0.24 |

|

Net Increase in Net Assets Resulting From Operations (Net Income) |

-$0.11 |

-$0.09 |

|

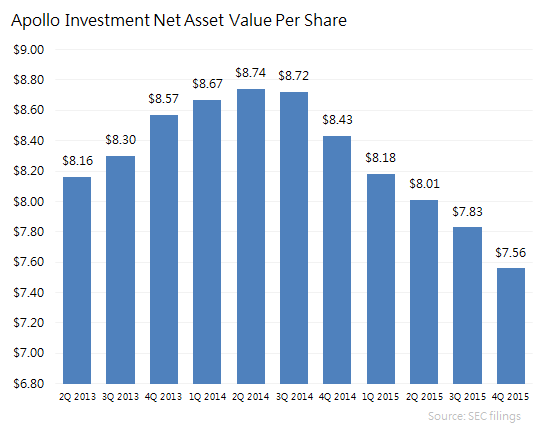

Net Asset Value (Book Value) |

$7.56 |

$8.43 |

Data source: SEC filings.

While operating earnings of $0.21 per share covered its $0.20 quarterly dividend, the company's bottom line, which includes the impact of capital gains and losses, failed to do so.

In the short run, operating income is a suitable measure for dividend sustainability from quarter to quarter, but in the long run, a company's all-encompassing net income figure is what drives performance and the ability to make outsized distributions to shareholders.

As its investments are affected by falling loan prices and weakening credit conditions in its energy portfolio, Apollo Investment's book value has now dropped six quarters in a row.

What happened this quarter?

Relatively "boring" by nature, financial companies tend not to change much from quarter to quarter. There were, however, a few notable events:

- The portfolio shrank by about $57 million on a net basis (new investments minus sales and repayments), or about 1.8% from the prior period.

- Fee waivers are helping the company hold the line on operating income. Notably, Apollo Investment's external manager waived about $5 million in fees this quarter, which added about $0.02 to net investment income per share. Without these fee waivers, Apollo Investment would have failed to earn its dividend from operating income.

- Oil and gas investments now make up about 12.9% of the company's investment portfolio at fair value, down from 15% last quarter, due largely to declines in their carrying values.

- Buybacks at prices below book value have helped stem the decline in book value on a per-share basis. Apollo Investment notes that repurchases of 10.6 million shares, or 4.5% of its initial shares outstanding, added about $0.07 to net asset value per share from August to the end of the fourth quarter.

- Non-accruals (investments on which Apollo Investment is not accruing income) currently make up 6% of the portfolio at cost, and 2.5% of the portfolio at fair value.

What management had to say

CEO James Zelter commented that "NAV per share declined during the quarter due to the dislocation in the credit markets which resulted in spread widening, as well as from low and falling oil prices."

On the call, one executive also provided some helpful hints about the company's capital allocation plans, noting that the company places "leverage a little bit higher than our stock," suggesting that the pace of buybacks could slow as the company manages its balance sheet.

Notably, Apollo Investment's balance sheet leverage stood at 0.8 times debt to equity, which is relatively high given a legal requirement to keep leverage at less than 1 debt to equity, and the ratings agencies' view that 0.85 times is a soft limit for maintaining an investment-grade credit rating.

Looking ahead

This year will be one of portfolio management. Of its four non-accrual investments, consider that only one (Gryphon Colleges) is not an energy- or commodity-related company. Working through the company's troubled commodity-exposed investments will remain a top priority as Apollo Investment enters calendar year 2016.