Duke Energy Corporation's (NYSE: DUK) stock is down some 10% since January 2015. Yet it's one of the country's largest utilities and, over the past few years, it's been shifting its business mix to focus on regulated markets. That means that Duke is getting less and less exciting, but also less and less risky even though Wall Street seems to be taking a pass on the shares. But, really, how risky is Duke Energy Corporation's stock?

Not what it was

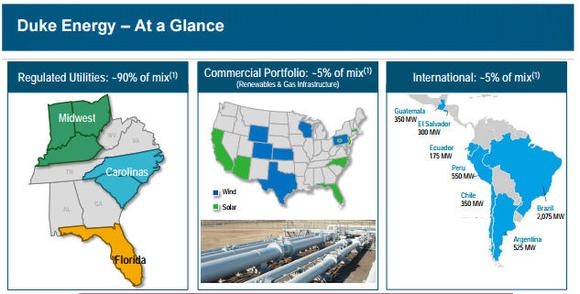

Before Duke bought Progress Energy in mid-2012, it generated around two-thirds of its revenues from regulated markets. That's an important figure to keep in mind, because it shows just how much Duke has changed in a very short period of time; today, its regulated utility business makes up around 90% of revenues.

Duke as it stands today. Source: Duke Energy.

Why is this important? Because regulated markets are essentially monopolies in which the government tells the incumbent utility how much it can make. On one hand, that limits upside potential, but on the other it leads to a pretty predictable business. So increasing this side of the the operations makes Duke more and more ... boring. Which, for a conservative investor, might be just what the doctor ordered.

That said, a good part of this growth has been achieved via acquisition. Buying Progress Energy was a big move, but Duke is currently in the middle of acquiring Piedmont Natural Gas (PNY +0.00%) for roughly $5 billion. Around 90% of Piedmont's business is regulated, so that's a plus. And it expands Duke's natural gas business, which should help on the growth side, too. But with any acquisition there's a risk that it could fall through.

So Duke's business is getting less risky, but it's taking on transaction risk to do it. That's probably a worthwhile trade-off, but it's something you'll want to keep in mind with this and any future moves. And when it comes to utilities, deals require the approval of regulators in every state or region affected.

That's been a real thorn in the side of Exelon (EXC 0.33%), which is trying to acquire Pepco (NYSE: POM). Regulators in D.C. and Maryland have balked at the deal, claiming it will stymie competition and stall renewable-power investment. Exelon has made concessions, but it hasn't helped, with D.C. regulators voting down the deal in recent days (though it provided steps that could lead to an approval). The same thing could happen to Duke and any other utility that goes the acquisition route.

Image source: Getty Images.

Other ways to get boring ...

Which brings up the other 10% of Duke's business. It's split pretty evenly between international power and the company's merchant power business, which sells power to other utilities. These are relatively small businesses now, but they are both far more volatile than the regulated operations. However, even here Duke is trying to make changes.

For example, on the international front, the utility recently announced that it intends to find a buyer for part or all of its international business. That would pull the company out of markets such as Brazil, Argentina, and Chile. A strong dollar and country-specific troubles in some of these key markets have made the international side of things a tough sled of late. So getting out is a good idea and will further reduce Duke's risk profile. However, until a deal is inked (and it gets through the entire approval process), you'll want to keep an eye on international.

The other 5% or so of the company is focused on the merchant power market. That's been a rough market, too, with low natural gas prices keeping a lid on how much companies can charge for the power they produce. But Duke isn't sitting still. For example, it sold 11 power plants that used carbon-based fuel to Dynegy (NYSE: DYN) for $2.8 billion in 2015. That reduced its exposure to the space, but also helped to alter its merchant power profile.

In fact, it's still investing in the division -- it's just refocusing. Indeed, Duke is building clean energy plants like solar as it moves away from carbon spewing plants that use coal, oil, and natural gas. As government regulations increasingly push the utility industry toward renewable power, Duke's investments here should be well positioned to benefit from solid demand, long-term contracts, and decent pricing. Of course, construction of any kind comes with risks, and you'll want to watch this space on that front, but overall Duke has even managed to find a way to make its merchant business look less risky.

This "clean" shift on the deregulated side, however, highlights a long-term issue that Duke shareholders will also want to watch on the regulated side of things. Today, coal and natural gas powered plants make up around 75% of Duke's owned capacity. Nuclear (about 18%), hydro (7%), and other clean energy options make up the rest. This isn't a bad thing today, but if present social and regulatory trends hold, Duke will increasingly be called upon to decrease its carbon footprint. To be sure, Duke's regulated business has plenty of time to shift gears and the spending it does to "clean up" should lead to top- and bottom-line growth. But you'll want to keep an eye on this big-picture theme even if it evolves over time periods that could be measured in decades.

Spend money to make money

So overall Duke looks like it's moving down the risk scale by increasing its regulated business, trying to jettison its international assets, and shifting toward renewables in its merchant operations. For a risk-averse utility investor, this is all good news. That said, don't lose sight of the fact that any purchase or sale requires regulatory approvals that could scuttle even the best deal, but that's not something specific to Duke.

And while you're at it, you'll also want to remember that regulated utilities generally spend money on new power plants and upgrading infrastructure in order to grow revenues, assuming rate hikes get approved by regulators. With the long-term trend toward clean energy and Duke's current power profile, it could wind up spending a lot over the comes decades. So there are risks here, but they're still similar to what any other utility would face. The real story about risk at Duke, despite what appears to be Wall Street concern, is the shift to get more regulated and ... boring. So boring, in fact, that investors might just be able to sleep well at night.