Salesforce: Steady Revenue Trajectory

Salesforce (CRM -3.22%) primarily provides customer relationship management software and enterprise cloud applications that help businesses manage operations globally.

While reducing its workforce and reorganizing its leadership team to consolidate its enterprise technology divisions, it reported an approximately 17% net income margin for the quarter ended Jan. 31, 2026.

Microsoft: Scaling Enterprise Operations

Microsoft (MSFT +2.54%) develops and licenses operating systems, cloud computing platforms, and productivity software while also manufacturing personal computing devices.

It initiated a voluntary retirement program for domestic employees and unsealed a lawsuit against a malware-signing service. The company generated an approximately 38% net income margin for the quarter ended March 31, 2026.

Why Revenue Matters for Retail Investors

Tracking revenue helps investors understand the total amount of money a business brings in before expenses are deducted. This metric enables investors to gauge raw business scale and growth.

Image source: The Motley Fool.

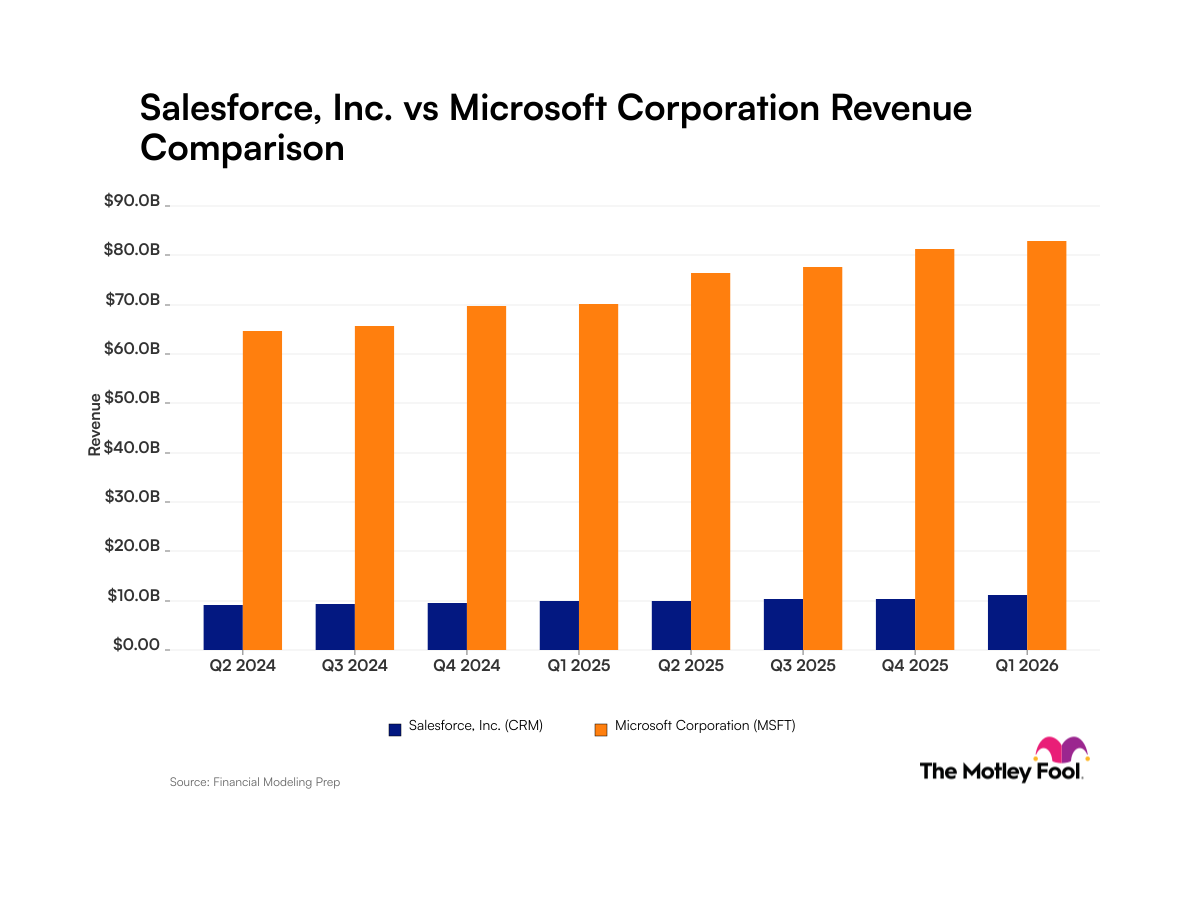

Quarterly Revenue for Salesforce and Microsoft

| Quarter (Period End) | Salesforce Revenue | Microsoft Revenue |

|---|---|---|

| Q2 2024 | $9.1 billion (period ended April 2024) | $64.7 billion (period ended June 2024) |

| Q3 2024 | $9.3 billion (period ended July 2024) | $65.6 billion (period ended Sept. 2024) |

| Q4 2024 | $9.4 billion (period ended Oct. 2024) | $69.6 billion (period ended Dec. 2024) |

| Q1 2025 | $10.0 billion (period ended Jan. 2025) | $70.1 billion (period ended March 2025) |

| Q2 2025 | $9.8 billion (period ended April 2025) | $76.4 billion (period ended June 2025) |

| Q3 2025 | $10.2 billion (period ended July 2025) | $77.7 billion (period ended Sept. 2025) |

| Q4 2025 | $10.3 billion (period ended Oct. 2025) | $81.3 billion (period ended Dec. 2025) |

| Q1 2026 | $11.2 billion (period ended Jan. 2026) | $82.9 billion (period ended March 2026) |

Data source: Company filings. Data as of May 19, 2026.

Foolish Take

While Microsoft’s revenue towers over Salesforce, both are experiencing sales growth, indicating their businesses continue to expand. This is particularly important in Salesforce’s case. The rise of artificial intelligence has led to concerns the technology could take customers away from Salesforce, but its rising revenue indicates that’s not the case.

In its 2026 fiscal year ended Jan. 31, Salesforce’s revenue jumped up 10% year over year to $41.5 billion. It anticipates ongoing growth, forecasting fiscal 2027’s sales to come in between $45.8 billion and $46.2 billion. This illustrates it’s doing well, and that AI is not hurting its business.

Even so, Wall Street dumped Salesforce shares in Q1. The stock’s forward price-to-earnings ratio of 14 is around a low point for the past year, suggesting shares are at an attractive valuation and that now is a good time to buy.

Microsoft stock was also battered in Q1 as Wall Street fretted it was spending too much on capital expenditures. That cost is a necessity to expand the company’s infrastructure to support demand for its AI offerings.

Microsoft’s sales for its fiscal third quarter, ended March 31, totaled $82.9 billion, representing an 18% increase over the prior year, and demonstrating the tech veteran continues to see strong growth. Its forward price-to-earnings ratio of 22 is not the bargain seen with Salesforce stock, but it’s still lower than a year ago, suggesting it, too, is at a compelling valuation.