Another quarter, another three months of margin expansion for Illinois Tool Works (ITW +2.21%). After a difficult end to 2015 prompting reduced earnings guidance, management has turned momentum around and for the second quarter in a row has raised its guidance for full-year earnings per share. In truth, the guidance hike is more about internal execution and margin optimism than an improvement in the revenue outlook. That said, it's only really the welding segment that's disappointing right now; elsewhere there are signs of a growth recovery in the engineering-equipment manufacturer's end markets. Let's take a closer look at a nuanced quarter that needs some careful explaining.

WELDING AND METAL CUTTING REMAINS A PROBLEM AREA FOR ILLINOIS TOOL WORKS. IMAGE SOURCE: GETTY IMAGES.

The tale of Illinois Tool Works's second-quarter earnings

A quick look at the key points from the update guidance helps explain matters.

- Full-year organic revenue growth is now expected to be in the range of 1% to 2% compared to prior guidance for 1% to 3%.

- Full-year GAAP EPS was upgraded from from prior guidance for $5.40 to $5.60 and is now expected to be between $5.50 and $5.70. Management started the year guiding toward $5.35 to $5.55.

- Operating margin guidance stays the same, with management still expecting more than 22.5% for the full year.

- Operating margin guidance includes "50 basis point dilution" due to an acquisition, so de facto Illinois Tool Works increased margin guidance.

Regular readers will already have seen that industrial supply company MSC Industrial Direct (MSM -0.03%) reported ongoing weakness in its heavy-machinery and metal-cutting end markets -- the kinds of industries that buy Illinois Tool Works' welding equipment. Deteriorating conditions in those end markets was borne out in Illinois Tool Works' organic revenue figures.

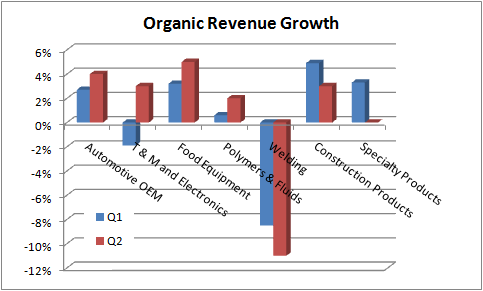

As you can see below, welding continued to disappoint for the company, but interestingly, four of the seven segments saw increased growth in the second quarter compared to the first. Indeed, the full-year organic revenue target was reduced only due to the "lingering difficult market conditions being experienced by the Welding segment."

DATA SOURCE: ILLINOIS TOOL WORKS.

A return to growth in test and measurement and electronics -- a highly cyclical sector -- is a notable and welcome event, suggesting that the company is over the worst of the slowdown in the industrial economy. Moreover, construction and automotive -- also seen as cyclical sectors -- remain strong.

Continued margin expansion

Outside welding, conditions appear to be improving, but management isn't simply waiting for some assistance from the economy. In fact, the company is in the fourth year of a five-year enterprise strategy aimed at expanding operating margin. A large part of the plan involves disposing of underperforming businesses and focusing on adjusting product lines in order to generate future growth.

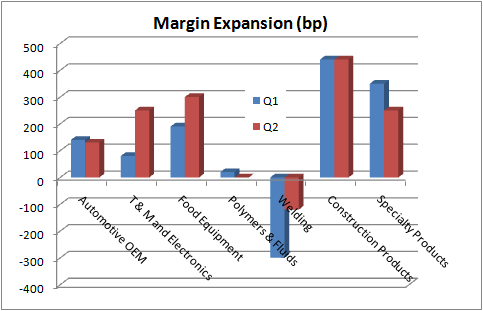

In other words, the company has self-help initiatives in place, and management continues to execute well. The chart below shows ongoing margin expansion in six of Illinois Tool Works' seven segments, and as a consequence management felt able to increase full-year EPS guidance.

BP REPRESENTS BASIS POINTS WHERE 100 BP EQUALS 1%. DATA SOURCE: ILLINOIS TOOL WORKS.

Looking ahead

Let's turn to third-quarter guidance. These are the results management expects:

- Organic revenue growth between 1% and 3%.

- GAAP EPS, including an acquisition, between $1.42 and $1.52.

- Operating margin at 23%.

Moreover, there is reason to believe there could be some upside to the third-quarter and full-year guidance. For example, during the earnings call CFO Michael Larsen outlined: "We are assuming current levels of demand going into Q3 and the slight bump in overall year-over-year organic growth rate is due to the comps. So we're assuming no acceleration in Q3 or Q4 at current demand levels."

However, outside welding, end-market conditions appear to be improving, and management's guidance could prove to be conservative. Regardless, it was a good second-quarter report, as the company continues to wring every bit of margin and growth it can from a moderately growing industrial economy.