When results of TrueCar, Inc.'s (TRUE +0.00%) second quarter hit the wires, investors responded favorably, sending the stock to a new 52-week high. That high is nice and all, but the stock still trades far below levels witnessed a couple of years ago before the company hit multiple speed bumps starting early last summer. A picture is worth a thousand words, so they say, so let's try to put TrueCar's better-than-expected second quarter into three important and telling graphs.

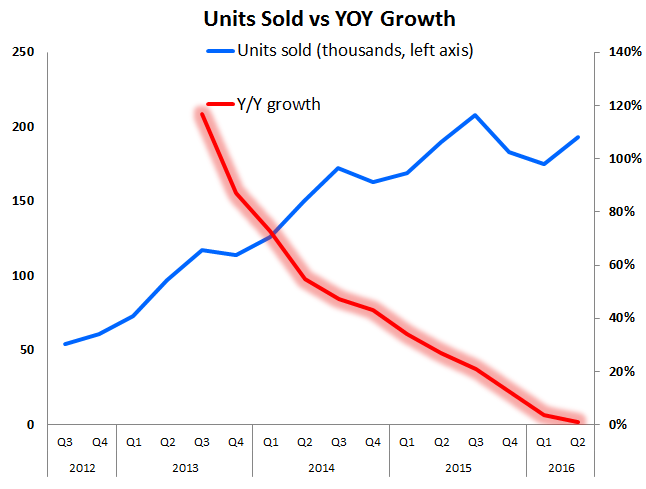

Great quarter, but has growth stalled?

It's a simple fact that eventually even the greatest of companies with the most popular products will have slowing sales in the face of saturation. The problem is when a slowdown happens before that saturation, due to competition or other factors, and that is a hurdle TrueCar is currently facing.

Image source: TrueCar, Inc. Chart by author.

For such a young company, it's problematic to see that year-over-year units sold -- which are new-vehicle transactions consumers complete at dealerships causing the latter to pay TrueCar for the sales lead -- screech to a halt near 0%.

The question isn't whether the growth is slowing, because that's clear, but whether management can revive its top-line growth. Investors hoping the company can do just that were optimistic when hearing about a new affinity partnership that should be completed and announced in the back half of 2016.

For those who aren't aware, an affinity partnership is an agreement between TrueCar and a large organization such as USAA or Sam's Club, both of which are already working with TrueCar. Consider that TrueCar's affinity partnerships generate only 30% of the website's unique visitors but contribute a higher 60% of unit sales. Depending on what organization TrueCar is close to inking a partnership with, it could definitely help revive sales.

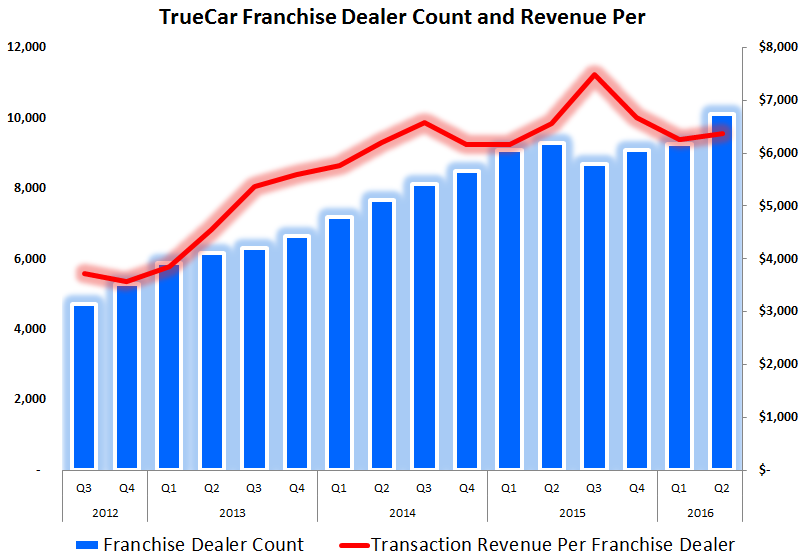

TrueCar seems to be optimizing its network

Another way to generate incremental revenue from its network of more than 10,000 dealerships is to simply make each dealership better at closing their sales leads. That's been a focus for TrueCar as it helped improve its dealerships' appearance on its website and has expanded its sales staff to help improve the sales process on both ends. The good news is that, if the second quarter is any indication, it's working.

Data source: TrueCar, Inc. Chart by author.

What you'll want to note here is that during the third quarter of 2015 when the revenue per dealership spikes, it's due to roughly the same amount of revenue being spread across a smaller dealership count. That was basically a neutral result. Now, looking at the first two quarters of 2016 and you can see that as the dealership count spikes to an all-time high, revenue per dealership actually moved higher. In my opinion, it wouldn't have been surprising to see revenue per dealership decline with such a spike in dealership numbers, and the fact that it didn't means TrueCar is helping each of its dealerships generate incremental revenue.

Also, as TrueCar and AutoNation continue to repair their rocky relationship, there was some great news coming from the latter. According to Automotive News, citing AutoNation's chief marketing officer, Marc Cannon, the close rate, quality of traffic, and value/pricing equation all vastly improved from when the partnership previously dissolved.

The only graph that matters

At the end of the day, the graph that matters the most is what appears on the company's bottom line.

Data source: TrueCar, Inc. Chart by author.

TrueCar was hitting its stride in 2014 before falling off a cliff early last summer. It's been a rough road since then, but the company has posted three consecutive quarters of improving adjusted EBITDA and management noted that the best is yet to come this year -- TrueCar's fourth quarter is likely to be its best quarterly result of the year.

As always, investors cheered when management moved its full-year guidance higher during the second-quarter conference call. TrueCar is maintaining its top-line forecast for full-year units to reach 780,000 and revenue to reach $270 million, but its adjusted EBITDA moves from breakeven to between $5 million and $6 million.

Ultimately, this was a strong quarter even as units sold slowed. It's very promising that the company's sales force is seemingly improving the effectiveness of its dealership network, as well as working behind the scenes to attract new affinity partners that could generate substantially more revenue and bottom-line earnings. Stay tuned. The second half of 2016 will be very telling for whether the rebound has legs.