Image source: Getty Images.

Part of why investing is so intriguing to many people is that the next product to help turn a company's stock into a multibagger or market-beating machine could be right in front of you. Maybe that new burrito shop is the next Chipotle. Maybe that music-streaming platform you're listening to is the next big thing. As long as you keep your eyes peeled and keep asking questions, you could stumble upon your greatest investment. In this case, the products associated with these two stocks are likely part of your everyday life.

Right under your feet

It's been quite the turnaround for U.S. Concrete (USCR +0.00%) after its highly leveraged balance sheet during the aftermath of the Great Recession caused it to file for Chapter 11 bankruptcy in 2010. This forced the company to shed some of its low-margin pre-cast business, and as a result it has emerged much healthier, with a narrowed focus on key markets: Texas, Northern California, and the New York metro area, to name some major spots.

U.S. Concrete stands to benefit from increased infrastructure work. Image source: Getty Images.

Over the trailing-12-month period ended June 30, U.S. Concrete generated 80% of its revenue from ready-mixed concrete for construction industries, and the remaining 20% from aggregates and aggregates-related materials (materials mined to use in the making of concrete). Of the ready-mixed volume, 59% was used in commercial and industrial markets while 26% went to residential construction.

The upside, in my opinion, could be with its third segment: street, highway, and other public works. That segment generated only about 15% of the company's ready-mixed volume, but U.S. Concrete is well positioned to benefit from the much-needed infrastructure improvement in America.

Beyond growth in construction segments, the company is pressing for growth from acquisitions, too. It's completed 21 ready-mixed concrete and aggregates acquisitions since 2014, and it's proven it can consolidate markets and vertically integrate operations to improve margins and returns.

Lastly, one of the intriguing factors for investors looking at U.S. Concrete is that its construction projects aren't typically one-hit wonders. The average length of the company's top 15 customer relationships is approximately 20 years. That means that the company does good work, bringing customers back, and that its relationships with huge companies offer a list of potential projects.

If the U.S. finally begins to pour additional capital into improving infrastructure, construction in residential and commercial markets continues to increase, and the company creates synergies with its acquisitions, better days are ahead for the company and its investors.

Tell me again about your leverage

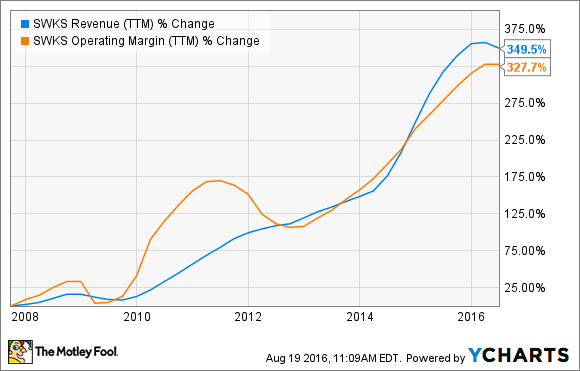

More often than not, when it comes to manufacturers and suppliers, the former has more negotiation leverage. That's generally because the larger manufacturers represents a huge order and large chunk of business for the supplier – thus, as the supplier badly wants this business, it concedes a bit of its pricing power. But in my opinion, Skyworks Solutions (SWKS +0.92%), a major supplier for Apple, has been able to buck the trend and has consistently increased its profitability with its top line.

SWKS Revenue (TTM) data by YCharts.

However, Skyworks' management understands that lessening its dependence on Apple for success will be important moving forward. Fortunately, in addition to supplying RF (radio frequency) chips for Apple's iPhone and Samsung's Galaxy devices, it also sells plenty of analog semiconductors in other industries that include wireless infrastructure, broadband applications, automotive industry, medical, and even military markets, to name a few. In fact, between 2011 and 2015, Skyworks' integrated mobile systems business segment grew from generating 20% of the company's total revenue to 52%.

Basically, consider Skyworks a play on the future of the Internet of Things -- the ability for products to connect to one another through the internet. Unfortunately, that's the long-term thesis, and Wall Street has sold off shares of Skyworks because it does indeed rely on Apple for a lot of its business, and the latter's iPhone sales have finally slowed -- and even declined -- over the past two quarters.

However, there might be some near-term upside, as Skyworks, in my opinion, is one of few companies positioned to take advantage of a rapidly expanding global 4G LTE network. According to Morningstar, citing data from Ericsson, LTE networks covered roughly 27% of the globe in 2014, but the coverage is expected to climb to 65% by 2019.

If Skyworks can get its fair share of RF chips into those devices accessing a rapidly expanding 4G LTE network, lessen its dependence on Apple for top- and bottom-line success, and expand into more IoT categories, this stock should be a big winner over the next decade.